In today's dynamic business environment, corporations and Canadian partnerships find themselves navigating through a labyrinth of tax regulations, striving to optimize their fiscal obligations while maintaining compliance. Among the tools at their disposal is the GST25 form, a critical document designed for closely related corporations and Canadian partnerships that wish to streamline their tax reporting and reduce administrative burdens. The form facilitates an election, or the revocation of one, allowing specified members of a qualifying group to treat certain taxable supplies exchanged among them as having been made for nil consideration. This mechanism is particularly advantageous for entities that engage in frequent transactions with each other, enabling them to forgo the usual GST/HST implications on these exchanges. The GST25 form encompasses Parts A, B, and C, each serving a distinct purpose: Part A for identification, Part B to ascertain eligibility, and Part C to either elect or revoke the election. This provision, however, comes with its set of prerequisites and exceptions, mandating a thorough understanding and careful consideration by the parties involved. It's essential for corporations and partnerships to meticulously complete the form and adhere to the stipulated terms, such as the eligibility criteria, the effective date of election or revocation, and the maintenance and retention of records. This comprehensive approach ensures that the electing parties benefit from the intended tax relief while remaining compliant with the Canada Revenue Agency's regulations.

| Question | Answer |

|---|---|

| Form Name | Gst25 Form |

| Form Length | 4 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 1 min |

| Other names | gst25 form, cra form gst 25, gst 25, closely canadian online |

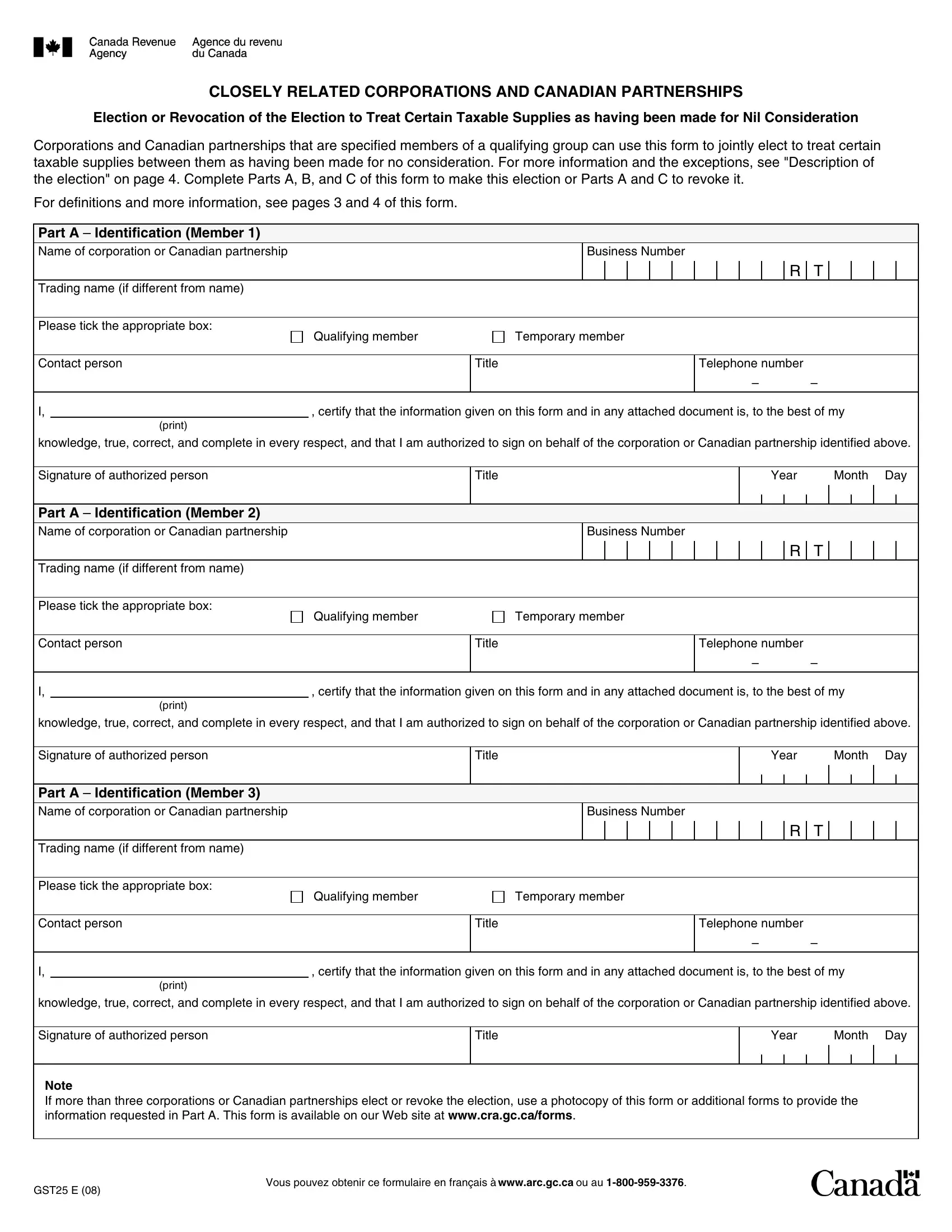

CLOSELY RELATED CORPORATIONS AND CANADIAN PARTNERSHIPS

Election or Revocation of the Election to Treat Certain Taxable Supplies as having been made for Nil Consideration

Corporations and Canadian partnerships that are specified members of a qualifying group can use this form to jointly elect to treat certain taxable supplies between them as having been made for no consideration. For more information and the exceptions, see "Description of the election" on page 4. Complete Parts A, B, and C of this form to make this election or Parts A and C to revoke it.

For definitions and more information, see pages 3 and 4 of this form.

Part A – Identification (Member 1)

Name of corporation or Canadian partnership |

Business Number |

|

|

|

|

|

|

|

|

|

|

|

|

|

R |

T |

|

|

|

|

Trading name (if different from name) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Please tick the appropriate box: |

Qualifying member |

Temporary member |

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Contact person |

|

Title |

|

|

|

|

|

Telephone number |

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

– |

– |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

I, |

, certify that the information given on this form and in any attached document is, to the best of my |

|||||||||||||||||

|

(print) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

knowledge, true, correct, and complete in every respect, and that I am authorized to sign on behalf of the corporation or Canadian partnership identified above.

Signature of authorized person |

Title |

|

Year |

Month Day |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Part A – Identification (Member 2)

Name of corporation or Canadian partnership |

Business Number |

|

|

|

|

|

|

|

|

|

|

|

|

|

R |

T |

|

|

|

|

Trading name (if different from name) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Please tick the appropriate box: |

Qualifying member |

Temporary member |

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Contact person |

|

Title |

|

|

|

|

|

Telephone number |

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

– |

– |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

I, |

, certify that the information given on this form and in any attached document is, to the best of my |

|||||||||||||||||

|

(print) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

knowledge, true, correct, and complete in every respect, and that I am authorized to sign on behalf of the corporation or Canadian partnership identified above.

Signature of authorized person |

Title |

|

Year |

Month Day |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Part A – Identification (Member 3)

Name of corporation or Canadian partnership |

Business Number |

|

|

|

|

|

|

|

|

|

|

|

|

|

R |

T |

|

|

|

|

Trading name (if different from name) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Please tick the appropriate box: |

Qualifying member |

Temporary member |

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Contact person |

|

Title |

|

|

|

|

|

Telephone number |

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

– |

– |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

I, |

, certify that the information given on this form and in any attached document is, to the best of my |

|||||||||||||||||

|

(print) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

knowledge, true, correct, and complete in every respect, and that I am authorized to sign on behalf of the corporation or Canadian partnership identified above.

Signature of authorized person |

Title |

|

Year |

Month Day |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Note

If more than three corporations or Canadian partnerships elect or revoke the election, use a photocopy of this form or additional forms to provide the information requested in Part A. This form is available on our Web site at www.cra.gc.ca/forms.

GST25 E (08)

Vous pouvez obtenir ce formulaire en français à www.arc.gc.ca ou au

Part B – Eligibility for the election

Each person must be a qualifying member or a temporary member to qualify as a specified member; only specified members in the same qualifying group are eligible to make this election. The definitions of these terms are on page 3.

Section 1 – This section must be completed.

Tick the boxes that apply:

The registrant corporations resident in Canada and registrant Canadian partnerships identified as qualifying members in Part A and on any attached forms are members of the same qualifying group.

None of the corporations identified as qualifying members in Part A and on any attached forms are party to an election to deem certain taxable supplies as supplies of financial services. (Tick this box if all the members identified as qualifying members in Part A or on any attached forms are Canadian partnerships.)

For each corporation or Canadian partnership, registrant and resident in Canada, identified as qualifying members in Part A and on any attached forms:

all or substantially all of the property of the corporation or Canadian partnership (other than financial instruments) was last manufactured, produced, acquired, or imported by the corporation or Canadian partnership for consumption, use, or supply exclusively in its commercial activities; or

if the corporation or partnership has no property (other than financial instruments), all or substantially all of the supplies it made were taxable.

If you ticked all three boxes, the corporations and Canadian partnerships identified as qualifying members in Part A and on any attached forms are eligible to jointly make the election.

Section 2 – This section has to be completed if there is at least one temporary member in the qualifying group.

Tick the boxes that apply:

The registrant corporations resident in Canada identified as temporary members in Part A and on any attached forms are members of a qualifying group but not qualifying members.

None of the corporations identified as temporary members are party to an election to deem certain taxable supplies as supplies of financial services.

The corporations identified as temporary members are to receive a supply of property in contemplation of a distribution made in the course of a reorganization from the distributing corporation that is a qualifying member in the same group.

The corporations identified as temporary members do not carry on any business or have any property (other than financial instruments) before receiving the supply and the shares of the corporations are transferred on the distribution.

If you ticked all four boxes, the corporations identified as temporary members in Part A and on any attached forms, that are to receive a supply of property in contemplation of a distribution made in the course of a reorganization, are eligible to jointly make the election with the qualifying members in the same qualifying group.

Complete Part C of this form.

Part C – Election or revocation of the election

Tick one of the boxes below and enter the effective date of the election or revocation of the election:

The corporations and Canadian partnerships identified in Part A of this form and on any attached forms jointly elect to treat taxable supplies made between them while the election is in effect as having been made for no consideration, with the following exceptions. The election does not apply to a supply of property or a service that is not acquired by the recipient of the supply for consumption, use, or supply exclusively in its commercial activities or to a sale of real property. If the recipient of the supply is a temporary member, the election also does not apply if a supply is not made in contemplation of a distribution in the course of a reorganization, as described in the Income Tax Act.

or

The corporations and Canadian partnerships identified in Part A of this form and on any attached forms jointly revoke the election to treat certain taxable supplies made between them as having been made for no consideration.

Year Month Day

Effective date of this election or revocation of the election:

Page 2

General information

Definitions

All or substantially all generally means 90% or more.

Canadian partnership means a partnership each member of which is a corporation or partnership and is resident in Canada.

Commercial activity means a business carried on by a person or an adventure or concern of the person in the nature of trade, but does not include the making of exempt supplies. It also includes the supply of real property by a person, other than an exempt supply, and anything done in the course of making the supply or in connection with the supply.

A commercial activity does not include a business carried on, or an adventure or concern in the nature of trade engaged in, by an individual, a personal trust or a partnership where all the members are individuals, without a reasonable expectation of profit.

Distribution has the meaning assigned by subsection 55(1) of the Income Tax Act. A distribution for the purposes of section 55 of the Income Tax Act means the direct or indirect transfer of property of a corporation (referred to in section 55 as a "distributing corporation") to one or more of its corporate shareholders (referred to in section 55 as a "transferee corporation") such that each transferee corporation that receives property on the distribution receives its pro rata share of each type of property owned by the distributing corporation immediately before the distribution.

Exclusive in respect of the consumption, use, or supply of a property or service by a person (other than a financial institution) means all or substantially all of the consumption, use, or supply of the property or service. For a financial institution, exclusive in respect of the consumption, use, or supply of a property or service means 100% of the consumption, use, or supply.

Qualifying group means:

a group of corporations, each member of which is closely related to each other member of the group; or

a group of Canadian partnerships, or of Canadian partnerships and corporations, each member of which is closely related to each other member of the group.

To determine if corporations or Canadian partnerships are closely related, for the purposes of this election, to other corporations or Canadian partnerships, see "Meaning of closely related corporations and closely related Canadian partnerships" later on this page.

Qualifying member of a qualifying group means a registrant corporation resident in Canada or a registrant Canadian partnership:

that is a member of the qualifying group;

that is not a party to an election to treat certain taxable supplies as supplies of financial services; and

all or substantially all of the property of which (other than financial instruments) was last manufactured, produced, acquired, or imported by the corporation or partnership for consumption, use, or supply exclusively in its commercial activities, or if the corporation or partnership has no property (other than financial instruments), all or substantially all of its supplies are taxable.

Qualifying subsidiary of a particular corporation means another corporation not less than 90% of the value and number of the issued and outstanding shares of the capital stock of which, having full voting rights under all circumstances, are owned by the particular corporation, and includes:

a corporation that is a qualifying subsidiary of a qualifying subsidiary of the particular corporation;

where the particular corporation is a credit union, every other credit union; and

where the particular corporation is a member of a mutual insurance group, every other member of that group.

Specified member of a qualifying group means:

a qualifying member of the group; or

a temporary member of the group. A temporary member of the group only qualifies as a specified member when it is to receive a supply of property in contemplation of a distribution made in the course of a reorganization described in subparagraph 55(3)(b)(i) of the Income Tax Act from the distributing corporation that is a qualifying member of the same group.

Note

Once the reorganization is complete, the temporary member must qualify as a qualifying member to be a specified member and eligible to make this election.

Temporary member of a qualifying group means a registrant corporation, resident in Canada:

that is a member of the group but not a qualifying member;

that is not a party to an election to treat certain taxable supplies as supplies of financial services;

that receives a supply of property in contemplation of a distribution made in the course of a reorganization described in subparagraph 55(3)(b)(i) of the Income Tax Act from the distributing corporation that is a qualifying member of the same group;

that does not carry on any business or have any property (other than financial instruments) before receiving the supply; and

that transfers its shares on the distribution.

Meaning of closely related corporations and closely related Canadian partnerships

Closely related corporations

In general, two corporations are considered to be closely related if at least 90% of the value and number of the issued and outstanding shares of the capital stock of one of the corporations, having full voting rights under all circumstances, are owned by:

the other corporation;

a qualifying subsidiary of the other corporation;

a corporation of which the other corporation is a qualifying subsidiary;

a qualifying subsidiary of a corporation of which the other corporation is a qualifying subsidiary; or

any combination of the corporations or subsidiaries referred to above.

Closely related Canadian partnerships

A particular Canadian partnership and another Canadian partnership are closely related if all or substantially all of the interest in the other Canadian partnership is held by:

the particular Canadian partnership;

a corporation or a Canadian partnership, that is a member of a qualifying group of which the particular partnership is a member; or

any combination of corporations or partnerships referred to above.

Two Canadian partnerships are also closely related to each other if one:

owns at least 90% of the value and number of the issued and outstanding shares, having full voting rights under all circumstances, of the capital stock of a corporation that is a member of a qualifying group of which the other partnership is a member; or

holds all or substantially all of the interest in a Canadian partnership that is a member of a qualifying group of which the other partnership is a member.

Page 3

Closely related Canadian partnerships and corporations

A Canadian partnership is considered to be closely related to a particular corporation if one of the following applies:

at least 90% of the value and number of the issued and outstanding shares, having full voting rights under all circumstances, of the capital stock of the particular corporation are owned by:

–the partnership;

–a corporation or a Canadian partnership, that is a member of a qualifying group of which the partnership is a member; or

–any combination of corporations or partnerships referred to above;

at least 90% of the issued and outstanding shares, having full voting rights under all circumstances, of the capital stock of a corporation that is a member of a qualifying group of which the particular corporation is a member are owned by the Canadian partnership.

at least 90% of the issued and outstanding shares, having full voting rights under all circumstances, of the capital stock of a corporation that is a member of a qualifying group of which the partnership is a member are owned by the particular corporation.

all or substantially all of the interest in the partnership is held by:

–the particular corporation;

–a corporation or a Canadian partnership that is a member of a qualifying group of which the particular corporation is a member; or

–any combination of corporations or partnerships that includes the particular corporation or another member of a qualifying group of which the particular corporation is a member;

all or substantially all of the interest in a Canadian partnership that is a member of a qualifying group of which the partnership is a member is held by the particular corporation; or

all or substantially all of the interest in a Canadian partnership that is a member of a qualifying group of which the particular corporation is a member is held by the partnership.

Persons closely related (as defined above) to the same person

Two corporations are considered closely related to each other for the GST/HST if they are each closely related to a third corporation.

A corporation and a Canadian partnership or two Canadian partnerships are considered closely related to each other for this election if they are each closely related to a third corporation or Canadian partnership, or would be considered to be closely related to the Canadian partnership if each member of that partnership were resident in Canada.

Interest in a partnership

For the purposes of this election, a person (corporation or partnership), or a group of persons, holds, at any time, all or substantially all of the interest in a partnership if at that time the person, or every person in the group, is a member of the partnership and the person is, or the members of the group collectively are, all the following:

entitled to receive at least 90% of the total of all amounts, each of which is the share of the partnership's income from all sources that each of its members is entitled to receive for the last fiscal period (within the meaning of the Income Tax Act) of the partnership that ended before that time (or if the partnership's first fiscal period includes that time, for that period), or if the partnership has no income, the total of all amounts each of which is the share of the income of the partnership that each member of the partnership would be entitled to receive if the income of the partnership from each source were one dollar;

entitled to receive at least 90% of the total amount that would be paid to all members of the partnership (other than amounts that would be paid as a share of partnership income) if it were wound up; and

able to direct the business and the affairs of the partnership, or would be able to do so if no secured creditor had any security interest in an interest in, or the property of, the partnership.

Description of the election

When a specified member of a qualifying group jointly elects with another specified member of the group, certain taxable supplies made between them are considered to have been made for no consideration. A corporation that has filed an election (Form GST27, Election or Revocation of an Election to Deem Certain Supplies to be Financial Services) to deem certain taxable supplies as supplies of financial services cannot make this election.

Exceptions

The following supplies are excluded from this election: a supply by way of sale of real property;

a supply of property or service that is not acquired by the recipient for consumption, use, or supply exclusively in the commercial activities of the recipient; and

a supply of property that is not made in contemplation of a distribution made in the course of a reorganization described in subparagraph 55(3)(b)(i) of the Income Tax Act, if the recipient of the supply is a temporary member.

Eligibility

Complete Part B on Page 2 of this form to determine if you are eligible to make this election.

Parties to this election

Every combination of eligible corporations and eligible Canadian partnerships whose names appear on this form and on any attached forms is considered to have made this election. For example, for a group with three electing members, if we number them 1, 2, and 3, the combinations would be:

a)1 and 2;

b)1 and 3; and

c)2 and 3.

Duration of the election

The election made jointly by two specified members of the qualifying group ceases to have effect on the earliest of:

the day one of those members ceases to be a specified member of the qualifying group; or

the day those members jointly revoke the election.

Books and records

You do not have to file this form with the Canada Revenue Agency. However, you must complete it and keep it with the books and records of the specified members making the election while an election is in effect, and for six years from the end of the year to which an election relates.

Do you need more information?

For more information, visit our Web site at www.cra.gc.ca/gsthst, or call us at

Page 4