In Iowa, certain uses of energy, such as electricity and gas, are exempt from state sales tax if they are for residential purposes. However, when energy is used in ways that do not qualify for this exemption—primarily, for non-residential purposes—the state mandates the use of the Iowa 31 116A form. This document serves as a critical communication tool between purchasers of energy and their suppliers. It clarifies that the energy purchased will be used in a manner subject to taxation, aiding in the proper assessment and collection of taxes. The form, which needs to be completed by the energy purchaser and provided to the seller, includes detailed sections for specifying the use of energy that disqualifies it from the residential energy exemption, the percentage of energy used in such taxable ways, and other pertinent information such as meter and utility account numbers. Sellers are required to keep the completed form on file and update it at least every three years based on the latest available information that substantiates the taxable use of energy. This process ensures both parties maintain accurate records for tax purposes, supporting the Iowa Department of Revenue’s efforts to fairly enforce tax laws while allowing businesses and other non-residential energy users to clearly document their tax liabilities related to energy use.

| Question | Answer |

|---|---|

| Form Name | Iowa Form 31 116A |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | itrl, affirm, purchaser, 31-116b |

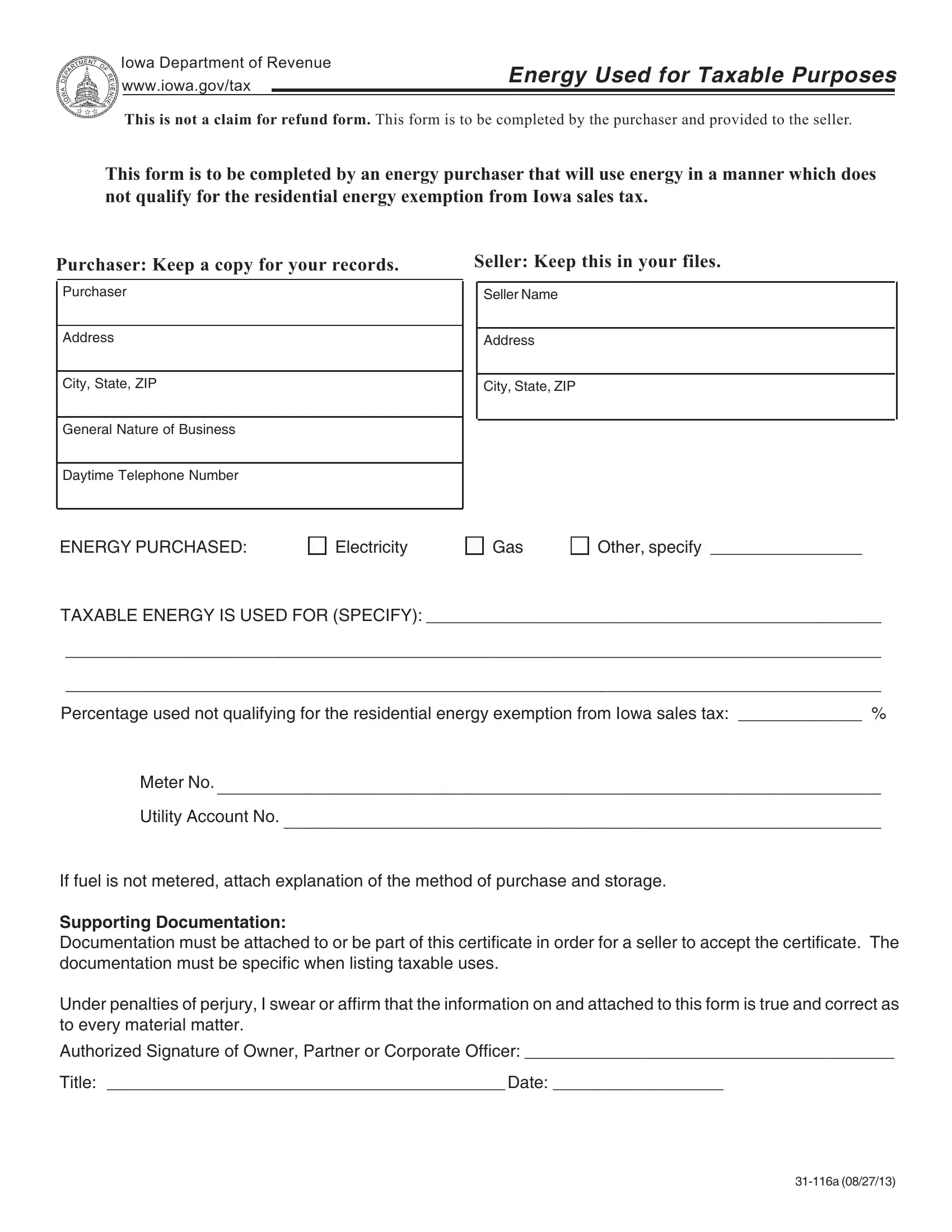

Iowa Department of Revenue

www.iowa.gov/tax

Energy Used for Taxable Purposes

This is not a claim for refund form. This form is to be completed by the purchaser and provided to the seller.

This form is to be completed by an energy purchaser that will use energy in a manner which does not qualify for the residential energy exemption from Iowa sales tax.

Purchaser: Keep a copy for your records.

Purchaser

Seller: Keep this in your files.

Seller Name

Address

Address

City, State, ZIP

City, State, ZIP

General Nature of Business

Daytime Telephone Number

ENERGY PURCHASED:

Electricity

Gas

Other, specify ________________

TAXABLE ENERGY IS USED FOR (SPECIFY): ________________________________________________

______________________________________________________________________________________

______________________________________________________________________________________

Percentage used not qualifying for the residential energy exemption from Iowa sales tax: _____________ %

Meter No. ______________________________________________________________________

Utility Account No. _______________________________________________________________

If fuel is not metered, attach explanation of the method of purchase and storage.

Supporting Documentation:

Documentation must be attached to or be part of this certificate in order for a seller to accept the certificate. The documentation must be specific when listing taxable uses.

Under penalties of perjury, I swear or affirm that the information on and attached to this form is true and correct as to every material matter.

Authorized Signature of Owner, Partner or Corporate Officer: _______________________________________

Title: __________________________________________ Date: __________________

Energy Used for Taxable Purposes

Residential energy is exempt from Iowa state sales tax. It remains subject to any applicable local option sales tax.

Residential energy includes metered electricity, metered natural gas, propane, heating fuel, and kerosene.

Energy billed to a residence is taxable when used for

If it is impractical to separately meter and bill the energy, complete the Energy Used for Taxable Purposes form

Seller: Keep this certificate in your files.

Purchaser: Keep a copy of this certificate for your records.

Do not send to the Iowa Department of Revenue.