Planning for retirement involves understanding various forms and requirements, including the Iowa W-4P form, which is essential for residents receiving pension or annuity payments. This form, made available by the Iowa Department of Revenue, is designed to manage how income tax is withheld from these payments. Pensioners and annuitants have the option to claim exemptions based on their filing status and other eligibility criteria, allowing for a more tailored approach to tax withholding. For example, qualifying Iowa residents over the age of 55, those who are disabled, or surviving spouses may exempt up to $6,000 or $12,000 of their annual taxable pension, depending on their marital status and if the taxable portion of their annual distribution exceeds certain thresholds. Moreover, there are provisions for those choosing not to have taxes withheld and for individuals who fall under specific income brackets, providing a complete framework for managing tax obligations. This form not only includes fields for personal identification but also clear instructions on the eligibility requirements, withholding options, and where to send the completed document. Whether opting for automatic exemptions, choosing not to have taxes withheld, or specifying an additional amount for withholding, the Iowa W-4P plays a pivotal role in financial planning for retirees in Iowa, ensuring they comply with state tax laws while potentially optimizing their retirement income.

| Question | Answer |

|---|---|

| Form Name | Iowa W 4P Form |

| Form Length | 1 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 15 sec |

| Other names | site:iowa.gov, filers, iowa w4p 2019, annuitants |

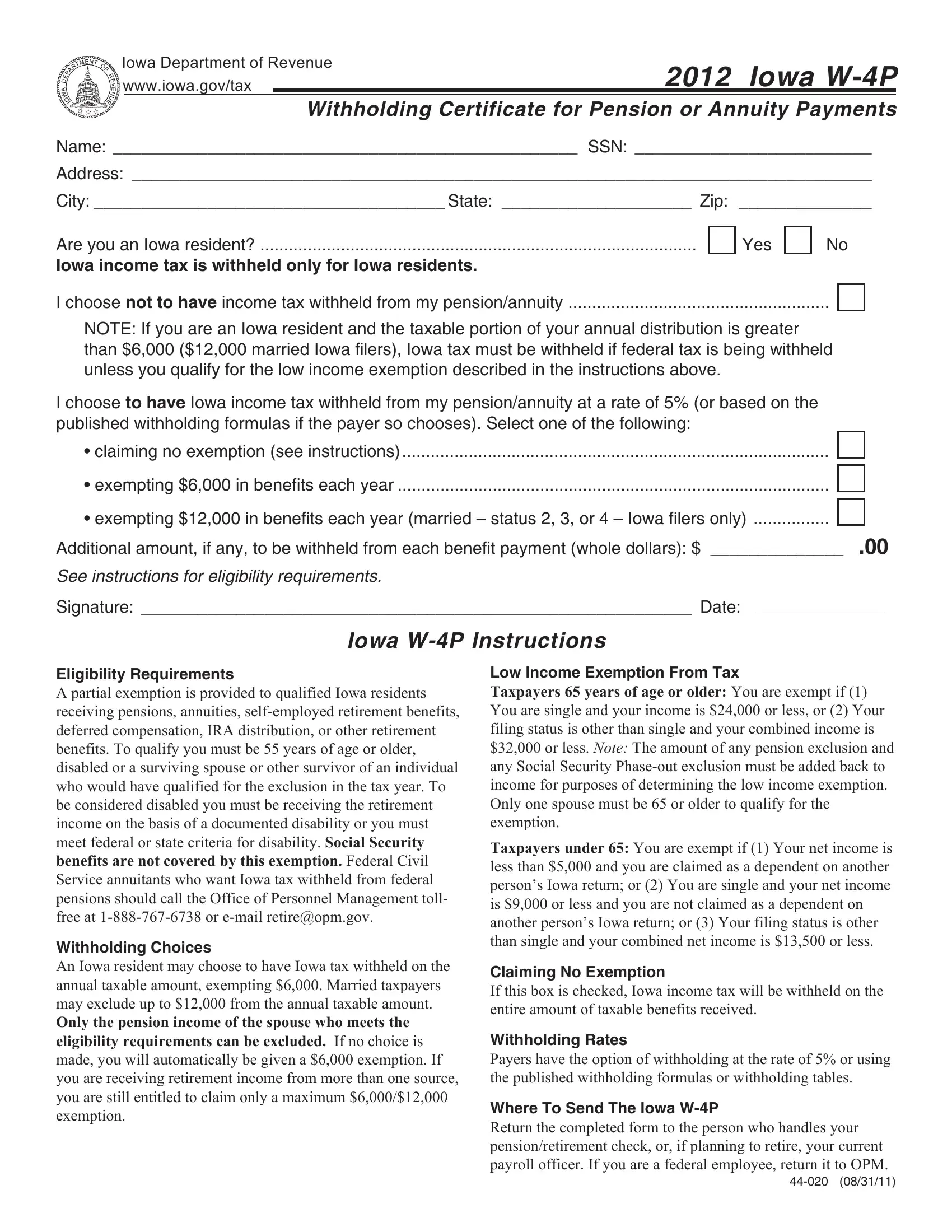

Iowa Department of Revenue

www.iowa.gov/tax

2012 Iowa

Withholding Certificate for Pension or Annuity Payments

Name: _________________________________________________ SSN: _________________________

Address: ______________________________________________________________________________

City: _____________________________________ State: ____________________ Zip: ______________

Are you an Iowa resident? ............................................................................................

Iowa income tax is withheld only for Iowa residents.

Yes

No

I choose not to have income tax withheld from my pension/annuity .......................................................

NOTE: If you are an Iowa resident and the taxable portion of your annual distribution is greater than $6,000 ($12,000 married Iowa filers), Iowa tax must be withheld if federal tax is being withheld unless you qualify for the low income exemption described in the instructions above.

I choose to have Iowa income tax withheld from my pension/annuity at a rate of 5% (or based on the published withholding formulas if the payer so chooses). Select one of the following:

• claiming no exemption (see instructions) ..........................................................................................

• exempting $6,000 in benefits each year ...........................................................................................

• exempting $12,000 in benefits each year (married – status 2, 3, or 4 – Iowa filers only) ................

Additional amount, if any, to be withheld from each benefit payment (whole dollars): $ ______________ .00

See instructions for eligibility requirements.

Signature: __________________________________________________________ Date:

Iowa

Eligibility Requirements

A partial exemption is provided to qualified Iowa residents receiving pensions, annuities,

Withholding Choices

An Iowa resident may choose to have Iowa tax withheld on the annual taxable amount, exempting $6,000. Married taxpayers may exclude up to $12,000 from the annual taxable amount.

Only the pension income of the spouse who meets the eligibility requirements can be excluded. If no choice is made, you will automatically be given a $6,000 exemption. If you are receiving retirement income from more than one source, you are still entitled to claim only a maximum $6,000/$12,000 exemption.

Low Income Exemption From Tax

Taxpayers 65 years of age or older: You are exempt if (1) You are single and your income is $24,000 or less, or (2) Your filing status is other than single and your combined income is $32,000 or less. NOTE: The amount of any pension exclusion and any Social Security

Taxpayers under 65: You are exempt if (1) Your net income is less than $5,000 and you are claimed as a dependent on another person’s Iowa return; or (2) You are single and your net income is $9,000 or less and you are not claimed as a dependent on another person’s Iowa return; or (3) Your filing status is other than single and your combined net income is $13,500 or less.

Claiming No Exemption

If this box is checked, Iowa income tax will be withheld on the entire amount of taxable benefits received.

Withholding Rates

Payers have the option of withholding at the rate of 5% or using the published withholding formulas or withholding tables.

Where To Send The Iowa

Return the completed form to the person who handles your pension/retirement check, or, if planning to retire, your current payroll officer. If you are a federal employee, return it to OPM.