COMMONWEALTH OF KENTUCKY

DEPARTMENT OF REVENUE

FRANKFORT, KENTUCKY 40620

10A100(P) (06-21)

Kentucky Tax Registration Application

and Instructions

www.revenue.ky.gov

Employer’s Withholding Tax Account

Sales and Use Tax Account/Permit

Transient Room Tax Account

Motor Vehicle Tire Fee Account

Commercial Mobile Radio Service (CMRS) Prepaid Service Charge Account

Utility Gross Receipts License Tax Account

Telecommunications Tax Account

Consumer’s Use Tax Account

Corporation Income Tax Account

Limited Liability Entity Tax Account

Kentucky Nonresident Income Tax Withholding on Distributive Share Income Tax Account

Coal Severance and Processing Tax Account

Coal Seller/Purchaser Certificate ID Number

10A100(P)(06-21)

Commonwealth of Kentucky

DEPARTMENT OF REVENUE

KENTUCKY TAX REGISTRATION APPLICATION

For faster service, apply online at

http://onestop.ky.gov

•Incomplete or illegible applications will delay processing and will be returned.

•See instructions for questions regarding completion of the application.

• Need Help? Call (502) 564-3306 or

Email DOR.Registration@ky.gov

FOR OFFICE USE ONLY

WH SU |

TEL CU |

CT |

CP NRWH |

TR |

UTL |

CID |

LL |

TF

CMRS

CBI #

FEIN

CRIS #

RCS Flag |

NAICS |

|

|

Coded/Date Coded |

Data Entry/Data Entered |

|

|

|

|

SECTION A |

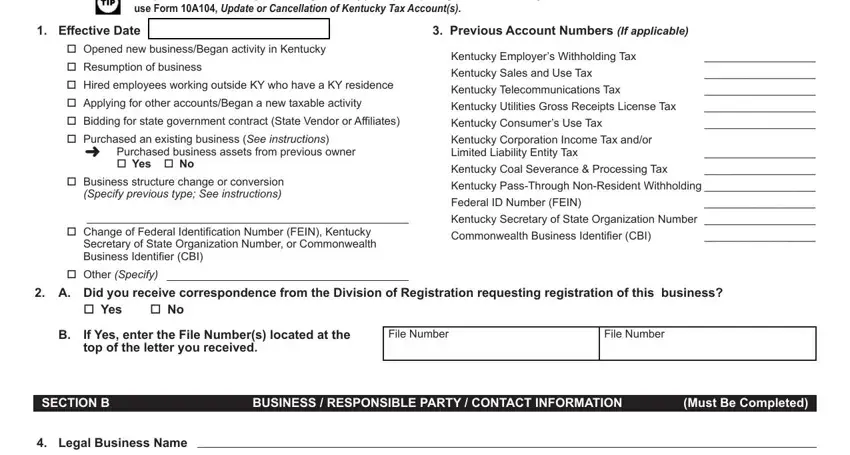

REASON FOR COMPLETING THIS APPLICATION |

(Must Be Completed) |

To update information for your existing account(s) or report opening a new location of your current business,

use Form 10A104, Update or Cancellation of Kentucky Tax Account(s).

Opened new business/Began activity in Kentucky

Resumption of business

Hired employees working outside KY who have a KY residence

Applying for other accounts/Began a new taxable activity

Bidding for state government contract (State Vendor or Affiliates)

Purchased an existing business (See instructions)

Purchased business assets from previous owner

Yes No

Business structure change or conversion (Specify previous type; See instructions)

Change of Federal Identification Number (FEIN), Kentucky Secretary of State Organization Number, or Commonwealth Business Identifier (CBI)

Other (Specify)

3. Previous Account Numbers (If applicable)

Kentucky Employer’s Withholding Tax |

__________________ |

Kentucky Sales and Use Tax |

__________________ |

Kentucky Telecommunications Tax |

__________________ |

Kentucky Utilities Gross Receipts License Tax |

__________________ |

Kentucky Consumer’s Use Tax |

__________________ |

Kentucky Corporation Income Tax and/or |

|

Limited Liability Entity Tax |

__________________ |

Kentucky Coal Severance & Processing Tax |

__________________ |

Kentucky Pass-Through Non-Resident Withholding __________________

Federal ID Number (FEIN) |

__________________ |

Kentucky Secretary of State Organization Number |

__________________ |

Commonwealth Business Identifier (CBI) |

__________________ |

2.A. Did you receive correspondence from the Division of Registration and Data Integrity requesting registration of this business?

Yes No

B.If Yes, enter the File Number(s) located at the top of the letter you received.

SECTION B |

BUSINESS / RESPONSIBLE PARTY / CONTACT INFORMATION |

(Must Be Completed) |

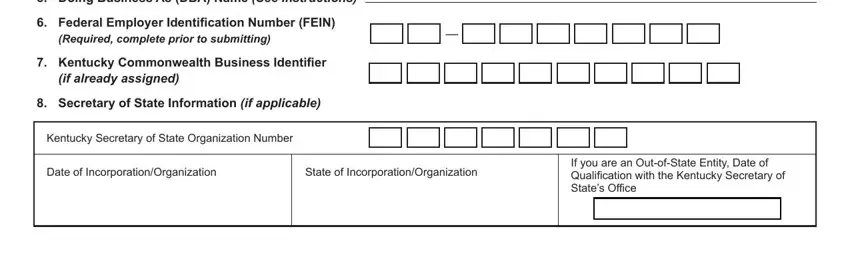

4.Legal Business Name

5.Doing Business As (DBA) Name (See instructions)

6.Federal Employer Identification Number (FEIN)

(Required, complete prior to submitting)

7.Kentucky Commonwealth Business Identifier

(if already assigned)

8.Secretary of State Information (if applicable)

Kentucky Secretary of State Organization Number

|

Date of Incorporation/Organization |

State of Incorporation/Organization |

If you are an Out-of-State Entity, Date of |

|

Qualification with the Kentucky Secretary of |

|

|

|

|

|

|

|

|

|

|

|

|

State’s Office |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

/ |

/ |

|

|

|

/ |

/ |

|

|

|

|

|

|

|

|

|

|

|

10A100(P)(06-21) |

|

|

|

|

|

|

Page 2 |

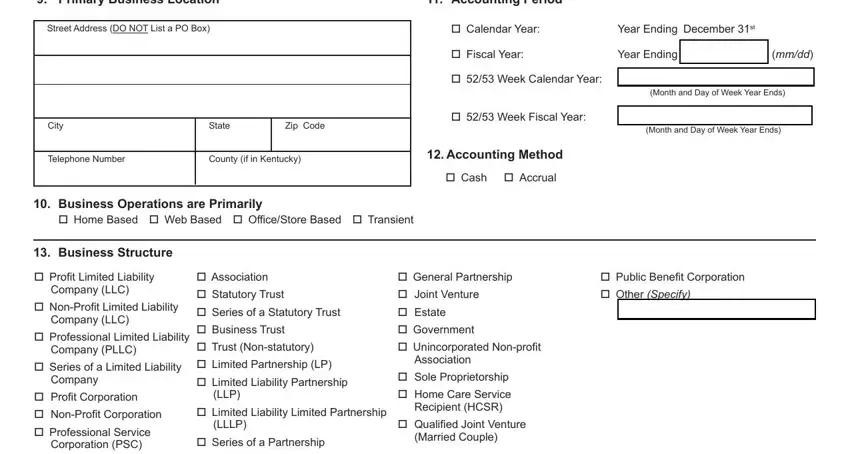

9. |

Primary Business Location |

|

|

11. Accounting Period |

|

|

|

|

|

|

|

|

|

|

Calendar Year: |

Year Ending December 31st |

|

Street Address (DO NOT List a PO Box) |

|

|

|

|

|

|

|

|

|

|

Fiscal Year: |

Year Ending |

___ ___ /___ ___ |

(mm/dd) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

52/53 Week Calendar Year: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

_______________________________ |

|

|

|

|

|

|

|

|

|

|

(Month and Day of Week Year Ends) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

52/53 Week Fiscal Year: |

_______________________________ |

|

|

|

City |

|

|

State |

Zip |

Code |

|

|

|

|

|

(Month and Day of Week Year Ends) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12. Accounting Method |

|

|

|

|

|

|

Telephone Number |

County (if in Kentucky) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

( |

) |

– |

|

|

|

|

Cash Accrual |

|

|

|

|

10.Business Operations are Primarily

Home Based Web Based Office/Store Based Transient

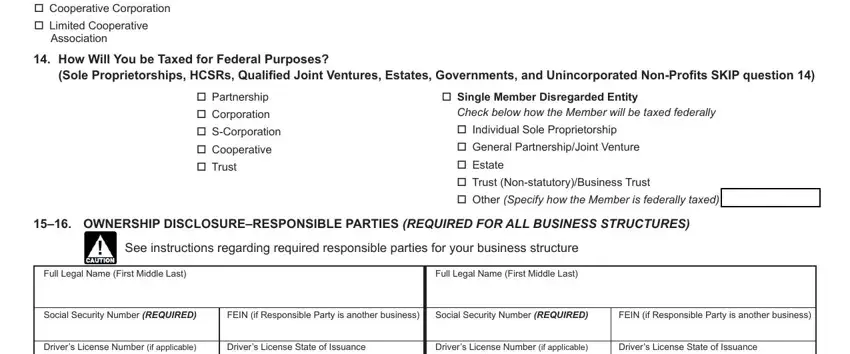

13. Business Structure

Profit Limited Liability |

Association |

General Partnership |

Public Benefit Corporation |

Company (LLC) |

Statutory Trust |

Joint Venture |

|

Other (Specify) |

|

Non-Profit Limited Liability |

Series of a Statutory Trust |

Estate |

|

|

Company (LLC) |

Business Trust |

Government |

|

|

|

|

Professional Limited Liability |

|

|

Company (PLLC) |

Trust (Non-statutory) |

Unincorporated Non-profit |

|

|

Series of a Limited Liability |

Limited Partnership (LP) |

Association |

|

|

Sole Proprietorship |

|

|

Company |

Limited Liability Partnership |

|

|

|

|

|

Profit Corporation |

(LLP) |

Home Care Service |

|

|

Non-Profit Corporation |

Limited Liability Limited Partnership |

Recipient (HCSR) |

|

|

Qualified Joint Venture |

|

|

Professional Service |

(LLLP) |

|

|

Series of a Partnership |

(Married Couple) |

|

|

Corporation (PSC) |

|

|

|

|

|

Cooperative Corporation |

|

|

|

|

Limited Cooperative |

|

|

|

|

Association |

|

|

|

|

14.How Will You be Taxed for Federal Purposes?

(Sole Proprietorships, HCSRs, Qualified Joint Ventures, Estates, Governments, and Unincorporated Non-Profits SKIP question 14)

Partnership

Corporation

S-Corporation

Cooperative

Trust

Single Member Disregarded Entity

Check below how the Member will be taxed federally

Individual Sole Proprietorship

General Partnership/Joint Venture

Estate

Trust (Non-statutory)/Business Trust

Other (Specify how the Member is federally taxed)

15–16. OWNERSHIP DISCLOSURE–RESPONSIBLE PARTIES (REQUIRED FOR ALL BUSINESS STRUCTURES)

See instructions regarding required responsible parties for your business structure

Full Legal Name (First Middle Last) |

|

|

|

Full Legal Name (First Middle Last) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Social Security Number (REQUIRED) |

FEIN (if Responsible Party is another business) |

|

Social Security Number (REQUIRED) |

|

FEIN (if Responsible Party is another business) |

|

|

|

|

|

|

|

|

|

|

Driver’s License Number (if applicable) |

Driver’s License State of Issuance |

|

Driver’s License Number (if applicable) |

|

Driver’s License State of Issuance |

|

|

|

|

|

|

|

|

|

|

|

|

Business Title |

|

|

Effective Date of Title |

|

Business Title |

|

|

|

Effective Date of Title |

|

|

|

|

/ |

/ |

|

|

|

|

|

|

/ |

/ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Residence Address |

|

|

|

|

|

Residence Address |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City |

|

|

|

State |

Zip Code |

|

City |

|

|

|

|

State |

Zip Code |

|

|

|

|

|

|

|

|

|

|

|

|

|

Telephone Number |

|

|

County (if in Kentucky) |

|

Telephone Number |

|

|

|

County (if in Kentucky) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

( |

) |

– |

|

|

|

|

( |

) |

– |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

17. Person to contact about this application:

E-mail: (By supplying your e-mail address you grant the Department of Revenue permission to contact you via e-mail.)

SECTION CTELL US ABOUT YOUR BUSINESS OR ORGANIZATION(Must Be Completed)

18a. Describe the nature of your business activity in Kentucky, including any services provided.

_________________________________________________________________________________________________________________________

18b. List products sold in Kentucky.

_________________________________________________________________________________________________________________________

|

The following questions will determine your need for an Employer’s Withholding Tax Account. |

|

|

|

|

Yes |

No |

19. |

Do you have or will you hire employees to work in Kentucky within the next six (6) months? |

|

|

|

An employee is anyone to whom you pay wages, including part-time help and family members. Kentucky corporate |

|

|

|

officers receiving compensation other than dividends are also considered employees. |

|

|

20. |

Do you wish to voluntarily withhold on Kentucky residents who work outside Kentucky? |

|

|

21. |

Do you wish to voluntarily withhold on pension and retirement payments? |

|

|

22.Will your business be registered to make charitable or other lawful gaming payouts in Kentucky and be required to withhold

federal tax from those payouts? |

|

|

If you answered Yes to any of questions 19 through 22, you must complete SECTION D.

The following questions will determine your need for a Sales and Use Tax Account,

the schedules you may need to file,

and/or your need for a

Transient Room Tax Account,

Motor Vehicle Tire Fee Account,

Commercial Mobile Radio Service (CMRS) Prepaid Service Charge Account,

Utility Gross Receipts License Tax Account, and/or

Telecommunications Tax Account.

Sales and Use Tax Account |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Yes |

No |

23. |

Will you make retail and/or wholesale sales of tangible or digital property in Kentucky? |

|

|

|

Examples: prepared food, internet sales, downloaded music and books. (SEE INSTRUCTIONS FOR MORE.) |

|

|

24. |

Will you install replacement parts for the repair or recondition of tangible property? |

|

|

|

Examples: automotive repairs, computer or electronics repair, furniture repair. (SEE INSTRUCTIONS FOR MORE.) |

|

|

25. |

Will you produce, fabricate, process, print or imprint tangible property? |

................................................................................................ |

|

|

|

Examples: sign making, window tinting, embroidery, screen printing, engraving. (SEE INSTRUCTIONS FOR MORE.) |

|

|

26. |

Will you charge for labor or services rendered in installing or applying tangible personal property, digital property, or service sold? |

|

|

27. Will you provide any of the following services? (SEE INSTRUCTIONS FOR MORE.) |

|

|

|

|

Yes |

No |

|

Yes |

No |

|

|

|

|

|

|

|

A. Landscaping services |

|

|

G. |

Linen supply services |

|

|

|

|

|

B. Janitorial services |

|

|

H. |

Indoor skin tanning services |

|

|

|

|

|

C. Small animal veterinary services |

|

|

I. |

Non-medical diet and weight reducing services |

|

|

|

|

|

D. Pet care services |

|

|

J. |

Limousine services, with a driver provided |

|

|

E. Industrial laundry services

F. Non-coin operated laundry and dry cleaning services

10A100(P)(06-21) |

|

Page 4 |

|

|

|

|

|

|

Yes |

No |

28. |

Will you sell extended warranties? |

|

|

29. |

Will you rent or lease tangible or digital property to others, including related companies? |

|

|

30.Will you charge admissions, including initiation fees, monthly fees or membership fees for the use of a facility or participating in an event or activity? (Non-profit organizations selling admissions other than golf admissions, check NO. (SEE INSTRUCTIONS

FOR ADDITIONAL INFORMATION.) |

|

|

31.Are you a remote retailer selling tangible personal property or digital property delivered or transferred electronically to a

|

purchaser in Kentucky? (SEE INSTRUCTIONS FOR ADDITIONAL INFORMATION.) |

|

|

32. |

Are you a manufacturer’s agent soliciting orders for a nonresident seller not registered in Kentucky? |

|

|

33a. |

Are you a marketplace provider or retailer? (SEE INSTRUCTIONS FOR ADDITIONAL INFORMATION.) |

|

|

33b. Do you facilitate sales by third party retailers? (See KRS 139.450. A marketplace provider may register for two Kentucky sales |

|

|

|

tax account numbers. SEE INSTRUCTIONS FOR ADDITIONAL INFORMATION.) |

|

|

33c. |

Are you applying for separate accounts for your own sales and for your facilitated sales? (SEE INSTRUCTIONS FOR ADDITIONAL |

|

|

|

INFORMATION.) |

|

|

34. |

Are you a manufacturing fee processor or a contract miner operating in Kentucky? |

|

|

35. |

Are you bidding on a contract with Kentucky state government? |

|

|

36. |

Are you an affiliate of a company who has been awarded a Kentucky state government contract? |

|

|

37. |

Will you rent campsites at campgrounds or recreational vehicle parks? |

|

|

Sales and Use Tax Account Schedules |

|

|

38. |

Will you receive receipts from the breeding of a stallion to a mare in Kentucky? |

|

|

39. |

Will you make sales of aviation jet fuel? |

|

|

40.Will you make sales of motor vehicles to residents of Arizona, California, Florida, Indiana, Massachusetts, Michigan, South

Carolina, or Washington? |

|

|

Transient Room Tax Account |

|

|

41. Will you rent temporary lodging to others? |

|

|

Examples: hotel, motel, or inn (SEE INSTRUCTIONS FOR MORE.) |

|

|

Motor Vehicle Tire Fee Account |

|

|

42. Will you sell new tires for motor vehicles or semi-trailers? |

|

|

Commercial Mobile Radio Service (CMRS) Prepaid Service Charge Account |

|

|

43.Will you sell cellular phones with preloaded minutes, prepaid cellular phone cards, or recharge cellular phones and cards

with minutes? .................................................................................................................................................................................................

Utility Gross Receipts License Tax Account and/or Telecommunications Tax Account

44. Were you approved for an Energy Direct Pay Authorization with a Utility Gross Receipts License Tax Exemption? |

|

|

Attach a copy of your official UGRLT Exemption Authorization. |

|

|

|

|

|

45. Will you sell any of the following? |

|

|

|

|

|

|

Yes |

No |

|

Yes |

No |

|

|

|

|

|

|

A. Sewer services |

|

|

E. |

Communications services |

|

|

|

|

B. Water utilities |

|

|

F. |

Multichannel video programming services *(see instructions) |

|

|

|

C. Natural, artifical, or mixed gas utilities |

|

|

G. |

Video streaming services *(see instructions) |

|

|

|

|

D. Electricity |

|

|

H. |

Direct broadcast satellite services *(see instructions) |

|

|

|

|

|

|

|

|

|

Yes |

No |

46a. Will your company purchase any of the utility types listed above in question 45 B through G from |

|

|

a provider outside of Kentucky? |

|

|

|

|

|

46b. If yes, please list the provider’s name and utility type: ___________________________________________________________________________

If you answered Yes to any of questions 23 through 45 E, you must complete SECTION E.

If you answered Yes to any of questions 44 or 45 B through 45 G, you must complete SECTION F.

If you answered Yes to any of questions 45 E through 45 H, you must complete SECTION G.

The following question will determine your need for a Consumer’s Use Tax Account.

Skip question 47 if you must complete Section E.

|

Yes |

No |

47. Will you make purchases from out-of-state vendors and not pay Kentucky Sales or Use Tax to the seller on those purchases? |

|

|

If you are a PROFESSIONAL SERVICE business or if your business will make a one-time purchase only, please see |

|

|

instructions for important additional details. |

|

|

If you answered Yes to question 47, you must complete SECTION H.

The following questions will determine your need for a

Corporation Income Tax Account and/or a Limited Liability Entity Tax Account.

|

If your answer to questions 13 and 14 was NOT |

|

|

|

Sole Proprietorship, HCSR, Qualified Joint Venture, Estate, Government, |

|

|

|

General Partnership taxed as a Partnership, or Joint Venture taxed as a Partnership, |

|

|

|

you must complete questions 48 through 54. |

|

|

|

|

Yes |

No |

48. |

Are you organized under the laws of Kentucky with the Kentucky Secretary of State’s Office? |

|

|

49. |

Will your business have its commercial domicile in Kentucky? |

|

|

50. |

Will your business own or lease any real or tangible property in Kentucky? |

|

|

51. Will your business have one or more individuals performing services in Kentucky? |

|

|

52. |

Will your business maintain an interest in a pass-through entity or derive income from Kentucky sources? |

|

|

53. |

Will you direct activities toward Kentucky customers for the purpose of selling them goods and/or services? |

|

|

54.Will your business own/lease any intangible property or receive payments from a related member as defined in KRS 141.205(1)(g) or an unrelated party for the use of intangible property in Kentucky such as royalties, franchise agreements, patents, trademarks,

If you answered Yes to any of questions 48 through 54, you must complete SECTION I.

The following questions will determine your need for a

Kentucky Nonresident Income Tax Withholding on Distributive Share Income Tax Account.

|

|

Yes |

No |

55. |

Is this business considered a pass-through entity as defined in KRS 141.010(21)? |

|

|

|

If you answered Yes to question 55, you must answer questions 56 A and 56 B. |

|

|

56. |

Does your pass-through entity have nonresident: |

|

|

|

|

Yes |

No |

A.Individual partner(s), shareholder(s), or member(s) receiving Kentucky distributive share income from your

pass-through entity? |

|

|

“Individual" includes estates and trusts. |

|

|

B. Corporate partner(s) or member(s) receiving Kentucky distributive share income from your pass-through entity? |

|

|

If you answered Yes to question 56 A and/or 56 B, you must complete SECTION J.

10A100(P)(06-21) |

|

Page 6 |

|

|

|

|

|

The following questions will determine your need for a |

|

|

|

Coal Severance/Processing Tax Account and/or a Coal Seller Purchaser Certificate ID#. |

|

|

|

|

Yes |

No |

57. |

Will you mine coal to which you own or possess the mineral rights? |

|

|

58. |

Will you purchase coal for the purpose of processing and resale, or do you process refuse coal? |

|

|

Processing means cleaning, breaking, sizing, dust allaying, treating to prevent freezing, or loading or unloading for any purpose.

59. Will you purchase and sell coal as a coal broker? |

|

|

If you answered Yes to any of questions 57 through 59, you must complete SECTION K and SECTION E.

SECTION D |

EMPLOYER’S WITHHOLDING TAX ACCOUNT |

|

Must be completed if you answered Yes to any of questions 19 through 22. |

|

|

60. |

A. Has a Kentucky Employer’s Withholding Tax Account already been assigned to this business? |

|

|

|

|

|

|

|

Yes |

|

No |

|

B. |

If Yes, list the Employer’s Withholding Tax Account Number |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

61. |

Number of Kentucky employees ______________________________ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

65. |

Employer’s Withholding Tax mailing address: |

|

|

|

|

|

|

|

|

62. |

Date wages/pensions first paid or will be paid (REQUIRED) |

|

|

Use the same address as your location address |

|

|

|

|

|

|

|

|

|

|

|

Use the same address as ______________________ Tax Account |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

/ |

/ |

|

|

|

c/o or Attn. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

63 |

Estimated total annual tax withheld in Kentucky: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

$0.00–$399.99 |

$2,000.00–$49,999.99 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City |

|

|

|

|

|

State |

|

Zip Code |

|

|

|

|

$400.00–$1,999.99 |

$50,000.00 or more |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Mailing Telephone Number |

|

County (if in Kentucky) |

|

|

|

|

|

|

|

|

|

|

( |

) |

– |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

64. |

A. |

Is the withholding for your employees reported by a Common Paymaster or a Common Pay Agent? |

|

|

|

|

|

|

|

Yes |

|

No |

Most payroll processors do NOT operate as Common Paymasters/Pay Agents. If using a payroll processor, check with them to determine if you should answer yes to the question above.

B.If Yes, attach a separate sheet listing which you use, Common Paymaster or Common Pay Agent, and provide their Business Name, FEIN, and Kentucky Employer’s Withholding Tax Account Number.

10A100(P)(06-21) |

Page 7 |

SECTION E |

SALES AND USE TAX ACCOUNT |

|

TRANSIENT ROOM TAX ACCOUNT |

|

MOTOR VEHICLE TIRE FEE ACCOUNT |

|

COMMERCIAL MOBILE RADIO SERVICE (CMRS) PREPAID SERVICE CHARGE ACCOUNT |

Must be completed if you answered Yes to any of questions 23 through 45 E or any of questions 57 through 59.

66. A. Has a Kentucky Sales and Use Tax Account already been assigned to this business? |

Yes |

No |

B. If Yes, list the Sales and Use Tax Account Number

67.Date sales began or will begin (REQUIRED)

//

68.Estimated gross monthly sales tax collected in Kentucky:

$0.00–$1,199.99 |

$1,200.00 or more |

69.A. Does this business have additional locations in Kentucky other

than the Primary Business Location? Yes |

No |

B.If Yes, attach a listing of all additional Kentucky locations. For each location, the attachment should include: doing business as (DBA) name, physical location address, phone number, date location was opened, and a description of the location’s business activity.

70.Sales and Use Tax mailing address:

Use the same address as your location address

Use the same address as _______________________ Tax Account

c/o or Attn.

Address

|

City |

|

|

|

State |

Zip Code |

|

|

|

|

|

|

Mailing Telephone Number |

County (if in Kentucky) |

|

( |

) |

– |

|

|

|

|

|

|

|

|

|

|

SECTION F |

UTILITY GROSS RECEIPTS LICENSE TAX ACCOUNT |

|

Must be completed if you answered Yes to any of questions 44 or 45 B through 45 G. |

|

|

71. A. Has a Kentucky Utility Gross Receipts License Tax Account already been assigned to this business? |

Yes |

No |

B. If Yes, list the Utility Gross Receipts License Tax Account Number

72.Date sales of utilities began or will begin (REQUIRED)

//

73.Telephone Number

(__________) __________ – ____________________

74.Utility Gross Receipts License Tax mailing address:

Use the same address as your location address

Use the same address as _______________________ Tax Account

c/o or Attn.

Address

|

City |

|

|

|

State |

Zip Code |

|

|

|

|

|

|

Mailing Telephone Number |

County (if in Kentucky) |

|

( |

) |

– |

|

|

|

|

|

|

|

|

|

|

Once the account for Utility Gross Receipts License Tax is assigned, use the website below to set up account for e-file.

http://revenue.ky.gov/Business/Utility-Gross-Receipts-License-Tax/Pages/default.aspx

10A100(P)(06-21) |

Page 8 |

SECTION G |

TELECOMMUNICATIONS TAX ACCOUNT |

Must be completed if you answered Yes to any of questions 45 E through 45 H.

75. |

A. |

Has a Kentucky Telecommunications Tax Account already been assigned to this business? |

|

|

|

|

|

|

Yes |

|

No |

|

B. |

If Yes, list the Telecommunications Tax Account Number |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

76. |

Does your organization have tangible personal property located within the Commonwealth of Kentucky? |

|

|

|

|

|

|

Yes |

|

No |

77.Select company type:

Municipal Entity |

Other Provider |

Consumer |

78.Date sales of services began or will begin in Kentucky (REQUIRED)

//

79.Telephone Number

(__________) __________ – ____________________

Once the account for Telecommunications Tax is assigned, use the website below to set up account for e-file.

80.Telecommunications Tax mailing address:

Use the same address as your location address

Use the same address as _______________________ Tax Account

c/o or Attn.

Address

|

City |

|

|

|

State |

Zip Code |

|

|

|

|

|

|

Mailing Telephone Number |

County (if in Kentucky) |

|

( |

) |

– |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

http://revenue.ky.gov/Business/Telecommunications-Tax/Pages/default.aspx

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

SECTION H |

CONSUMER’S USE TAX ACCOUNT |

|

|

|

|

|

|

|

|

|

|

|

Must be completed if you answered Yes to question 47. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

81. |

A. |

Has a Consumer’s Use Tax Account already been assigned to this business? |

|

|

|

Yes No |

|

|

B. |

If Yes, list the Consumer’s Use Tax Account Number |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

82. |

Date purchases began or will begin (REQUIRED) |

83. Consumer’s Use Tax mailing address: |

|

|

|

|

|

|

|

|

|

|

|

|

|

Use the same address as your location address |

/ |

/ |

|

|

Use the same address as _______________________ Tax Account |

|

|

|

|

|

|

|

|

|

|

|

|

c/o or Attn. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City |

|

|

State |

Zip Code |

|

|

|

|

|

|

|

|

|

|

Mailing Telephone Number |

County (if in Kentucky) |

|

|

|

( |

) |

– |

|

|

|

|

|

|

|

|

|

|

|

|

10A100(P)(06-21) |

Page 9 |

|

|

SECTION I |

CORPORATION INCOME AND/OR LIMITED LIABILITY ENTITY TAX ACCOUNT |

|

Must be completed if you answered Yes to any of questions 48 through 54. |

|

|

84. A. Has a Corporation Income and/or Limited Liability Entity Tax Account already been assigned to this business? |

Yes |

No |

B. If Yes, list the Corporation Income or Limited Liability Entity Tax Account Number

85.A. Is this entity treated federally as a division of a parent company

and not separately taxed as its own entity? Yes |

No |

B.If Yes, select the division type below:

Qualified Subchapter S-corporation Subsidiary (QSUB)

Qualified Real Estate Investment Trust Subsidiary (QRS)

86.If an out-of-state entity, is your Kentucky activity limited to the mere solicitation of the sale of tangible personal property and exempt from

Corporation Income tax due to Public Law 86-272? Yes |

No |

87.If an out-of-state entity, date activity or receipt of pass through income began or will begin in Kentucky

//

89.Corporation Income and/or Limited Liability Entity Tax mailing address:

Use the same address as your location address

Use the same address as _______________________ Tax Account

c/o or Attn.

Address

|

City |

|

|

|

State |

Zip Code |

|

|

|

|

|

|

Mailing Telephone Number |

County (if in Kentucky) |

|

( |

) |

– |

|

|

|

|

|

|

|

|

|

|

88. A. Is your entity exempt from Corporation Income Tax and/or Limited Liability Entity Tax under Kentucky law? |

Yes |

No |

B.If Yes, see Exemption Table 1 in the instructions to provide the code for your Exemption Type. __________________________________________

C. If Political Organization selected above, are you required to file federal Form 1120-POL? |

Yes |

No |

SECTION J |

KENTUCKY NONRESIDENT INCOME TAX WITHHOLDING ON DISTRIBUTIVE SHARE |

|

INCOME TAX ACCOUNT |

|

Must be completed if you answered Yes to question 56 A and/or B. |

|

|

90.A. Has a Kentucky Nonresident Income Tax Withholding on Distributive Share Income Tax Account already been assigned to this business?

Yes No

B. If Yes, list the Kentucky Nonresident Income Tax Withholding on Distributive Share Income Tax Account Number

91.Date first nonresident corporation or individual became a partner, member, or shareholder (REQUIRED)

//

92.A. Is your entity exempt from Kentucky Nonresident Income Tax

Withholding on Distributive Share Income Tax under Kentucky law? Yes No

B.If Yes, see Exemption Table 2 in the instructions to provide the code for your Exemption Type.

__________________________________________________

93.Nonresident Distributive Share Withholding Tax mailing address:

Use the same address as your location address

Use the same address as _______________________ Tax Account

c/o or Attn.

Address

|

City |

|

|

|

State |

Zip Code |

|

|

|

|

|

|

Mailing Telephone Number |

County (if in Kentucky) |

|

( |

) |

– |

|

|

|

|

|

|

|

|

|

|

SECTION K COAL SEVERANCE/PROCESSING TAX ACCOUNT and/or COAL SELLER/PURCHASER CERTIFICATE ID #

Must be completed if you answered Yes to any of questions 56 through 58.

94. A. Has a Coal Severance Tax Account and/or a Coal Seller/Purchaser Certificate ID # already been assigned to this business? |

Yes |

No |

B.If Yes, list the Coal Severance Tax Account Number

C.If Yes, list the Coal Seller/Purchaser Certificate ID Number

95.Date mining/processing or coal brokering operations began or will begin (REQUIRED)

//

96.Coal Severance & Processing Tax mailing address:

Use the same address as your location address

Use the same address as _______________________ Tax Account

c/o or Attn.

Address

|

City |

|

|

|

State |

Zip Code |

|

|

|

|

|

|

Mailing Telephone Number |

County (if in Kentucky) |

|

( |

) |

– |

|

|

|

|

|

|

|

|

|

|

IMPORTANT: THIS APPLICATION MUST BE SIGNED BELOW:

The statements contained in this application and any accompanying schedules are hereby certified to be correct to the best knowledge and belief of the undersigned who is duly authorized to sign this application.

Signature: __________________________________________________ |

Printed Name:_______________________________________________ |

|

|

|

|

(mm/dd/yyyy) |

Phone Number: ______________________________________________ |

Title: ______________________ |

Date: |

____/____/______ |

For assistance in completing the application, please call the Division of Registration at (502) 564–3306, Monday through Friday between the hours of 8:00 a.m. and 5:00 p.m., Eastern Time, or you may use the Telecommunications Device for the Deaf at (502) 564-3058.

SEND completed application to: |

KENTUCKY DEPARTMENT OF REVENUE |

|

DIVISION OF REGISTRATION |

|

501 HIGH STREET, STATION 20 |

|

FRANKFORT, KENTUCKY 40602-0299 |

|

FAX: |

502–227–0772 |

|

E-MAIL: |

DOR.Registration@ky.gov |

If you would like to register for Electronic Funds Transfer (EFT), visit the Kentucky Department of Revenue website at http://revenue.ky.gov .

This form does not include registration with the Secretary of State, Unemployment Insurance, or Workers’ Compensation Insurance. For assistance, please contact those offices at the telephone numbers below.

Secretary of State |

(502) 564–3490 |

Unemployment Insurance (502) 564–2272 |

Workers’ Compensation (502) 564–5550 |

IRS—FEIN |

(800) 829–4933 |

|

|

For assistance with other questions about starting a business in Kentucky, including special licensing and permitting requirements, business structure registration, employer responsibilities, and business development resources, call the Business Information Clearinghouse at 1–800–626–2250 or visit the Kentucky Business One Stop website at http://onestop.ky.gov .

The Kentucky Department of Revenue does not discriminate on the basis of race, color, national origin, sex, age, religion, disability, sexual orientation, gender identity, veteran status, genetic information or ancestry in employment or the provision of services.

10A100(P)(06-21) |

INSTRUCTIONS |

Commonwealth of Kentucky

DEPARTMENT OF REVENUE

KENTUCKY TAX REGISTRATION APPLICATION

WHAT IS THE PURPOSE OF THE KENTUCKY TAX REGISTRATION APPLICATION?

This application is used to apply for any of the following: Employer’s Withholding Tax Account, Sales and Use Tax Account/Permit,Transient Room Tax Account, Motor Vehicle Tire Fee Account, Commercial Mobile Radio Service (CMRS) Prepaid Service Charge Account, Telecommunications Tax Account, Utility Gross Receipts License Tax Account, Consumer’s Use Tax Account, Corporation Income Tax Account, Limited Liability Entity Tax Account, Kentucky Nonresident Income Tax Withholding on Distributive Share Income Tax Account, Coal Severance and Processing Tax Account, and/or Coal Seller/Purchaser Certificate ID Number.

DO I HAVE ANY OTHER DEPARTMENT OF REVENUE TAX REGISTRATION REQUIREMENTS?

Depending on the product or service your business provides, there may be other state taxes that apply to your business. Most of these require that you file a special application/registration. To register for Tobacco Tax, Minerals or Natural Gas Severance Tax, Motor Fuels Tax, or any other miscellaneous taxes or fees administered by the Department of Revenue, visit the Department’s website at www.revenue.ky.gov .

I ALREADY HAVE TAX ACCOUNTS, HOW DO I UPDATE MY ACCOUNT INFORMATION?

Complete FORM 10A104, UPDATE OR CANCELLATION OF KENTUCKY TAX ACCOUNT(S), to update information; such as business name, location or mailing addresses, phone numbers, accounting period, responsible party information, and to report a taxing election change with the Internal Revenue Service (IRS) or to request cancellation of your accounts. Visit www.revenue.ky.gov to obtain the form.

You may also update certain business and tax account information for the Department of Revenue and the Kentucky Secretary of State’s Office online. If you do not already have online access to your business, follow the steps below.

1.Go to onestop.ky.gov .

2.Click on the link for One Stop Business Services.

Note: The One Stop Business Services login page provides information on creating a user account, as well as portal security. You will also find overview information for the services the portal currently provides. This information is updated regularly to reflect new services and notify you when additional agencies join the portal.

3.Welcome to the Kentucky Online Gateway. Select that you are a citizen or business partner and click Create Account.

4.Complete your Kentucky Online Gateway user account. Once a user account has been created, an e-mail will be sent to you with further instructions to activate the account and login. You must use the activation link in the e-mail prior to logging in to your account.

5.Once logged in, launch the Kentucky Business One Stop App.

6.Go to the Link My Business option. Click on the link provided within that webpage to obtain the Commonwealth Business Identifier (CBI) and the Security Token for the business.

Note: You will be able to provide information to gain immediate access to the business or request a letter be mailed, which contains your CBI and Security Token. To gain secure access to the portal, each business has been assigned a unique Security Token, which is an enhanced security feature of the portal.

7.Once you have the CBI and Security Token for the business, the Link My Business option will require you to name at least one “One-Stop Portal Business Administrator.” (This should be the business owner or a representative from the business.)

Note: The administrator can then delegate access to other individuals—for example, an attorney, accountant or manager. The administrator also determines the appropriate authority level for delegates to make changes—this could include changes such as filing annual reports with the Secretary of State’s Office, changing the business address, or filing and paying taxes. Only the One Stop business administrator(s) can grant, approve, withdraw or revoke access to the business.

For more information about registering and using the portal, visit onestop.ky.gov . For questions, please call the Kentucky Business One Stop Help Line at (502) 564-5053.

WHO CAN I CALL WITH QUESTIONS ABOUT REGISTRATION?

For help completing the application, please call the Division of Registration at (502) 564-3306, Monday through Friday between the hours of 8:00 a.m. and 5:00 p.m., Eastern Time.

You may also use the Telecommunications Device for the Deaf, (502) 564-3058.

The Department of Revenue has an Ombudsman who serves as your advocate and is available to make sure your rights are protected. You may contact the Ombudsman at (502) 564-7822.

WHEN SHOULD I FILE MY APPLICATION?

You are required to complete the application and file it with the Kentucky Department of Revenue at least 30 days before engaging in an activity that requires the establishment of the following:

n Employer’s Withholding Tax Account (KRS 141.310) |

n Consumer’s Use Tax Account (KRS 139.310) |

n Sales and Use Tax Account (KRS 139.200, 139.240) |

n Utility Gross Receipts License Tax Account (KRS 160.613) |

n |

Transient Room Tax Account (KRS 142.400) |

n |

Telecommunications Tax Account (KRS 136.614 and 136.616) |

n |

Motor Vehicle Tire Fee Account (KRS 224.50-868) |

n |

Coal Seller/Purchaser Certificate ID Number (KRS 143.037) |

nCommercial Mobile Radio Service Prepaid Service Charge Account (KRS 65.7634)

Pass-Through Entities must complete the application to establish a Kentucky Nonresident Income Tax Withholding on Distributive Share Income Tax Account (KRS 141.206) within 30 days of obtaining a Kentucky non-resident individual or corporate partner, member, or shareholder.

Corporations and Limited Liability Entities must complete the application to establish a Corporation Income Tax Account and/or a Limited Liability Entity Tax Account (KRS 141.040, 141.0401):

If you are... |

Then your application should be filed... |

|

|

Kentucky formed |

Within 30 days of formation with the Kentucky Secretary of State’s Office |

|

|

Formed out-of-state and you have obtained a Certificate of Authority to |

Within 30 days of obtaining a certificate of authority, provided that you |

transact business in Kentucky from the Kentucky Secretary of State |

are treated as doing business in Kentucky under KRS Chapter 141 |

|

|

Formed out-of-state and you have NOT obtained a Certificate of Authority |

Within 30 days of first engaging in activities that result in you being |

to transact business in Kentucky from the Kentucky Secretary of State |

treated as doing business in Kentucky under KRS Chapter 141 |

|

|

IS MY APPLICATION COMPLETE? |

|

Your application will not be considered complete unless it includes all required information specified on the form. This includes, but is not limited to, a Federal Employer Identification Number and accurate Social Security Number(s), as appropriate. You are required to provide your Social Security Number on tax forms per Section 405, Title 42, of the United States Code. This information will be used to establish your identity for tax purposes.

WHAT PENALTIES APPLY?

Failure to complete and file the required application in the specified time frames listed above shall subject you to applicable penalties as provided in KRS 131.180.

HOW LONG WILL IT TAKE FOR MY ACCOUNT NUMBERS TO BE ASSIGNED?

Fully completed paper applications will be processed, barring seasonal workload increases, within 5 to 10 business days. Applications with missing or unclear information requiring additional research may take longer. Those with extensive amounts of missing information will be returned by mail for further completion.

For faster service, apply online at onestop.ky.gov .

Note: If your business structure is not available as a selection online, you must submit a completed Kentucky Tax Registration Application by mail, fax, or e-mail.

LINE BY LINE APPLICATION INSTRUCTIONS

SECTION A—REASON FOR COMPLETING THIS APPLICATION

1.Effective Date—Enter the effective date of the reason you are completing this application. Check the box which corresponds to why the application is being completed.

•Opened New Business, Began Activity in Kentucky, Resumption of Business, Hired Employees Working Outside Kentucky Who Have a Kentucky Residence—Complete Sections A, B, and C to determine the accounts for which you are required to apply. For Resumption of Business, list your previous account numbers in Section A, question 3.

•Applying for Other Accounts, Began a New Taxable Activity—If you require an account type that is not currently assigned to your business, complete Sections A, B, and C to determine the additional accounts for which you are required to apply. If the questions in Section C lead you to complete a Section for an account type you already have, write your current account number in the field provided within the Section you are completing.

•Bidding for State Government Contract (State Vendor or Affiliates)—Any vendor who contracts to sell, install, or provide services to the Commonwealth of Kentucky or one of its agencies, or any affiliate of a company who contracts to sell, install, or provide services to the Commonwealth, is required to register for Kentucky Sales and Use Tax per KRS Chapter 45A, and collect and remit the Sales and Use Tax imposed by KRS Chapter 139. Complete Sections A, B, and C to determine the accounts for which you are required to apply.

•Purchased an Existing Business—(This will include a business previously owned by a family member.)

|

10A100(P)(06-21) |

Page 3 |

|

|

|

|

|

If the business you purchased was a... |

Then... |

|

|

|

|

|

n Sole Proprietorship |

|

|

n Joint Venture |

|

|

n Qualified Joint Venture |

|

|

n General Partnership |

|

|

n Series of a Statutory Trust |

You will need to apply for new accounts. List the previous owner’s |

|

n Limited Partnership (LP) |

accounts in Section A, question 3, and complete Sections B and C to |

|

n Limited Liability Partnership (LLP) |

determine the account(s) for which you are required to re-apply. |

|

n Limited Liability Limited Partnership (LLLP) |

|

|

n Series of a Partnership |

|

|

n Series of a Limited Liability Company (LLC) |

|

|

n Protected Cell Company (PCC) |

|

|

|

|

|

|

n Profit Corporation |

If: |

|

n Profit Limited Liability Company (LLC) |

–you are converting the purchased business to a new business structure, |

|

n Professional Service Corporation (PSC) |

or |

|

n Professional Limited Liability Company (PLLC) |

–the Federal Identification Number (FEIN) has changed, or |

|

n Public Benefit Corporation |

–the Secretary of State Organization Number has changed, or |

|

n Association |

–the Commonwealth Business Identifier (CBI) has changed, |

|

n Cooperative Corporation |

you will need to apply for new accounts. List the previous owner’s |

|

n Limited Cooperative Association |

|

n Statutory Trust |

accounts in Section A, question 3, and complete Sections B and C to |

|

n Business Trust |

determine the account(s) for which you are required to re-apply. |

|

n Trust (non-statutory) |

|

|

|

|

|

|

n Non-Profit Corporation |

If the business structure, Federal Identification Number (FEIN), Secretary |

|

n Non-Profit Limited Liability Company (LLC) |

|

of State Organization Number, and Commonwealth Business Identifier |

|

n Unincorporated Non-Profit Association |

|

(CBI) will all stay the same, DO NOT use the Kentucky Tax Registration |

|

|

|

|

|

|

Application. Use Form 10A104, Update or Cancellation of Kentucky |

|

|

|

Tax Account(s), to provide the updated business and responsible party |

|

|

|

information or update your information online. |

|

|

|

|

Note to persons buying a business: Any person buying a business may incur a sales tax liability on the purchase of the business assets or become personally liable for the prior sales tax liability of the seller. It may be necessary for the purchaser to withhold a part of the sales price until verification has been furnished by the seller that tax liabilities have been paid or do not exist. Therefore, it is important that anyone purchasing a business obtain a copy of Kentucky Revised Statutes 139.670 and 139.680 to determine the tax consequences and potential liability in such transactions. Copies are available at www.revenue.ky.gov, by writing the Office of Sales and Excise Taxes, Department of Revenue, P. O. Box 1274, Frankfort, Kentucky 40602-1274, or by calling (502) 564-5170.

•Business Structure Change or Conversion, Change in Federal Identification Number (FEIN), Change in Kentucky Secretary of State Organization Number, or Change in Commonwealth Business Identifier (CBI)—A business may change its taxing election with the Internal Revenue Service (IRS) and retain the same Kentucky tax account numbers. However, any change to an entity’s business structure, Federal Identification Number (FEIN), Kentucky Secretary of State Organization Number, or Commonwealth Business Identifier (CBI) requires that new accounts be applied for with the Department of Revenue.

To change a taxing election, use Form 10A104, Update or Cancellation of Kentucky Tax Account(s), to provide the updated business and responsible party information.

For all other business structure changes or conversions, for receiving a new Federal Identification Number (FEIN), for receiving a new Kentucky Secretary of State Organization Number, or for receiving a new Commonwealth Business Identifier (CBI), you must apply for new Kentucky tax account numbers. List your old account numbers in Section A, question 3, and complete Sections A, B and C to determine the account(s) for which you are required to re-apply.

Examples of conversions requiring a business apply for new accounts are:

n A Sole Proprietorship converting to a General Partnership and vice versa,

n A Corporation converting to a Limited Liability Company (LLC) and vice versa,

n A Limited Liability Company (LLC) converting to a Statutory Trust and vice versa, or n Any ownership type converting to a Limited Liability Company (LLC) and vice versa.

2.Did you receive correspondence from the Division of Registration and Data Integrity—If you received a letter(s) requesting registration, check Yes and list the File Number(s) from the letter in B. If No, leave B blank.

3.Previous Kentucky Account Numbers—If you have purchased an existing business, list the previous owner’s accounts, if available. If your current business has changed business structures, received a new Federal Identification Number (FEIN), received a new Kentucky Secretary of State Organization Number, or a new Commonwealth Business Identifier (CBI) and your company must apply for new accounts or you have resumed an old business, list your old accounts in Section A, question 3. A request in writing from the previous owner is required to cancel previous accounts.

SECTION B—BUSINESS / RESPONSIBLE PARTY / CONTACT INFORMATION

4.Legal Business Name—Enter the complete legal business name for your business or organization.

Note: If the business is a Sole Proprietorship, do not include your personal name unless it is a part of the business name or you do not have a business

name. For example: John Smith’s Plumbing.

If the business is a Home Care Service Recipient (HCSR), the name of the business should be the first, middle and last name of the disabled or elderly individual with the acronym “HCSR” added to the end of the name. For example: “John Q Public HCSR”.

5.Doing Business As (DBA)—If your business or organization has a “doing business as” name, enter the name.

6.Federal Employer Identification Number (FEIN)—Enter the FEIN assigned to your business or organization by the Internal Revenue Service. If you are a disregarded entity that is operating under your parent’s FEIN, DO NOT list your parent’s/member’s FEIN.

Apply for a FEIN online at www.irs.gov or contact the IRS at (800) 829-4933. Sole Proprietorships and Disregarded Entities that do not have employees or file certain federal excise tax returns may not be required to hold a FEIN for federal purposes. However, all businesses applying for Kentucky tax accounts are encouraged to obtain a FEIN. A FEIN helps distinguish a business from others with similar names, and for certain documents, may be an alternative to using a personal Social Security Number.

7.Kentucky Commonwealth Business Identifier (CBI)—If your business has already been assigned a CBI, enter that 10-digit number. This number is used to uniquely identify your business for the Kentucky One Stop Portal across all state agencies that utilize the portal.

8.Secretary of State Information—Sole Proprietorships, Estates, HCSRs, Governments, Unincorporated Non-Profit Associations, Unincorporated Associations, Qualified Joint Ventures, and Non-statutory Trusts are not required to register with the Kentucky Secretary of State. General Partnerships or Joint Ventures who do not operate using a DBA or Assumed Name are not required to register with the Kentucky Secretary of State.

For all remaining entities, enter the Organization Number assigned to your entity by the Kentucky Secretary of State’s Office. Enter your date of incorporation/ organization and list the state in which you incorporated/organized. If an out-of-state entity, list the date you qualified with the Kentucky Secretary of State’s Office to do business in Kentucky.

9.Primary Business Location—List the street address, city, state and ZIP Code for the location for which you are requesting registration. Do not list a P.O. Box for a business location address. For out-of-state businesses that do not have a Kentucky location, use the principal location address in your home state. If your location is in Kentucky, enter county name. If out-of-state, leave county blank. Enter the telephone number for the listed location; include the area code.

10.Business Operations are Primarily—Check the box where your business is primarily operated.

11.Accounting Period—Check the box that corresponds to when your business or organization’s accounting period ends. If you choose the fiscal year filing box, enter the month and day when your year ends. If you choose the 52/53 week calendar year box, enter the month and day of the week your year ends. If you choose the 52/53 week fiscal year box, enter the month and day of the week your year ends.

Note: Most businesses operate under a calendar year basis (year end December 31).

12.Accounting Method—Check the box corresponding to the accounting method your company uses.

Cash Basis—The business elects to report receipts in the accounting period that payment is actually or constructively received from the customer, even though the customer may take posession of the product before actually paying for it.

Accrual Basis—The business elects to report receipts in the accounting period that the sale actually occurs, regardless of when the customer makes payment for such purchases.

13.Business Structure—Check the box for the organizational structure type you have selected for your business. If “Other” selected, enter the structure type on the blank provided.

|

Business Structure |

Basic Definition |

|

|

|

|

Profit Limited Liability Company (LLC) |

An organization of individuals chartered by law and operating under the direction of members or managers. |

|

|

For US federal taxation purposes an LLC can be taxed as a single member disregarded entity, partnership, |

|

Non-Profit Limited Liability Company |

or a corporation. |

|

(LLC) |

|

|

|

A Non-Profit LLC is a special type of LLC formed for educational, charitable, social, religious, civic or |

|

Professional Limited Liability Company |

humanitarian purposes. |

|

(PLLC) |

|

|

|

A PLLC is a special type of LLC formed to engage in specific types of licensed professional services such |

|

Series of a Limited Liability Company |

as law, medicine, architecture, accounting, engineering, etc. |

|

|

Some states’ laws allow for the formation of Series underneath a main or master LLC, which has separate |

|

|

rights, powers, or duties, or has a separate purpose or investment objective. |

|

|

Each LLC which has a Series should register each of its separate Series which do business in Kentucky |

|

|

with the Kentucky Secretary of State’s Office as an assumed name. |

|

|

For Kentucky Department of Revenue purposes, each Series within an LLC must register for its own separate |

|

|

Corporation Income Tax and/or Limited Liability Entity Tax Account, unless it has chosen a disregarded status. |

|

|

|

|

Profit Corporation |

An organization chartered by law and recognized as having a legal existence as an entity separate from |

|

|

its owners. It operates under the direction of duly elected officers. |

|

Non-Profit Corporation |

A Non-Profit Corporation is a special type of corporation formed for educational, charitable, social, religious, |

|

|

|

Professional Service Corporation (PSC) |

civic, or humanitarian purposes. |

|

|

|

Public Benefit Corporation |

A PSC is a special type of corporation formed to engage in specific types of licensed professional services |

|

such as law, medicine, architecture, accounting, engineering, etc. |

|

|

|

|

A Public Benefit Corporation is a special type of corporation created to perform a specific function for the |

|

|

benefit of the public. |

|

|

|

10A100(P)(06-21) |

Page 5 |

|

|

Business Structure |

Basic Definition |

|

|

Cooperative Corporation |

A group of individuals known as patrons who have supplied their own capital at their own risk, who |

|

democratically direct and manage the enterprise, and who themselves receive the fruits of their |

Limited Cooperative Association |

cooperative endeavors, through the allocation of the excess among themselves. In general, Cooperatives |

|

are treated as corporations for Kentucky tax purposes. |

|

Limited Cooperative Associations must register as such with the Kentucky Secretary of State’s Office. This |

|

business structure allows for investor members in addition to patron members. For Kentucky purposes, |

|

Limited Cooperative Associations are also subject to the Limited Liability Entity Tax. |

|

|

Association |

An association is an unincorporated group joined together for a common purpose. However, associations |

|

may be treated as corporations for Kentucky tax purposes. |

|

|

Trust (Non-statutory) |

A legal entity that acts as fiduciary, agent or trustee on behalf of a person or business entity for the purpose |

|

of administration, management and the eventual transfer of assets to a beneficial party. |

Business Trust |

|

|

A Statutory Trust must register as such with the Kentucky Secretary of State’s Office. |

Statutory Trust |

|

|

A Series of a Statutory Trust is a Series established by a Statutory Trust, which has separate rights, powers, |

Series of a Statutory Trust |

or duties, or has a separate purpose or investment objective. Each Statutory Trust should register each of |

|

its separate Series with the Kentucky Secretary of State’s Office as an assumed name. (KRS 386A.4-010) |

|

For Kentucky purposes, Statutory Trusts and Series of Statutory Trusts are subject to the Limited Liability |

|

Entity Tax. |

|

For Kentucky Department of Revenue purposes, each Series within a Statutory Trust must register for its |

|

own separate Limited Liability Entity Tax Account, unless it has chosen a disregarded status. |

|

|

Limited Partnership (LP) |

A partnership formed by two or more persons having one or more general partners and one or more |

|

limited partners. The limited partner(s) have restricted liability for the business debts, while the general |

Limited Liability Partnership (LLP) |

partner(s) are fully liable. Limited liability will only be recognized for partnerships registered as a limited |

|

partnership through a state’s Secretary of State’s Office. |

Limited Liability Limited Partnership |

|

(LLLP) |

Some states’ laws allow for the formation of Series underneath the main or master Partnership, which |

|

has separate rights, powers, or duties, or has a separate purpose or investment objective. |

Series of a Partnership |

|

|

Each Partnership which has a Series should register each of its separate Series which do business in |

|

Kentucky with the Kentucky Secretary of State’s Office as an assumed name. |

|

For Kentucky Department of Revenue purposes, each Series within a Partnership must register for its |

|

own separate Limited Liability Entity Tax Account, unless it has chosen a disregarded status. |

|

|

General Partnership |

Two or more individuals owning and/or operating a business. All partners jointly share profits and losses |

|

and are individually responsible for debts incurred. |

|

|

Joint Venture |

A business entity that is generally short lived, frequently common to construction related activities, |

|

where two or more individuals or businesses come together temporarily to participate in a profit making |

|

activity. Usually, each partner specializes in a specific field of expertise or has resources not available |

|

to the other partner(s). |

|

|

Estate |

The total property, real and personal, that was owned by an individual, now deceased, before distribution |

|

through a trust or will. |

|

|

Government |

City, county, state, and federal agencies. |

|

|

|

An unincorporated informal group of members who come together to perform some social good conducted |

Unincorporated Non-Profit |

for nonprofit purposes. Per KRS 273A.005(6), “Nonprofit purposes” means any one (1) or more of |

Association |

the following purposes: charitable, benevolent eleemosynary, educational, civic, patriotic, political, |

|

governmental, religious, social, recreational, fraternal, literary, cultural, athletic, scientific, agricultural, |

|

horticultural, animal husbandry, and professional commercial, industrial, or trade association, but shall |

|

not include labor unions, cooperative organizations, and organizations subject to any of the provisions |

|

of the insurance laws or banking laws of this state which may not be organized under this chapter. |

|

|

Sole Proprietorship |

One single person owning and/or operating a business, solely responsible for all debts and liabilities |

|

incurred by the business. |

|

|

10A100(P)(06-21) |

Page 6 |

|

|

Business Structure |

Basic Definition |

|

|

Home Care Service Recipient (HCSR) |

A disabled or elderly individual participating in an in-home domestic services program administered by |

|

a state or local agency where all or part of the services received are paid for with funds supplied by the |

|

federal, state, or local government. |

|

A Federal Identification Number (FEIN) is issued in the name of the disabled or elderly individual (Service |

|

Recipient) as the employer. The Service Recipient or their family designates an agent to report, file, and |

|

pay employment taxes on the Service Recipient’s behalf. |

|

|

Qualified Joint Venture |

A business jointly owned and operated by a married couple who are electing to have the business not |

|

treated as a general partnership for federal tax purposes. Spouses electing qualified joint venture status |

|

are treated as sole proprietors for federal tax purposes. |

|

|

Other |

Any ownership not elsewhere classified. |

|

|

14.How will You be Taxed for Federal Purposes? Indicate how this business will be treated for federal purposes. If “Single Member Disregarded Entity, Other” is selected, list what type of entity the single member is and how it is taxed.

15-16. Ownership Disclosure—Responsible Parties—Enter the full legal name, Social Security Number (required if responsible party is an individual), FEIN (if responsible party is another business), driver’s license number, driver’s license state of issuance, residence address, city, state, ZIP Code, telephone number, county (if in Kentucky), business title and the date for when the title became effective for the information that corresponds to your business structure. Note: Social Security Numbers for responsible parties are required (KRS 131.180(3)). Also, you are required to provide your Social Security Number on tax forms per Section 405, Title 42, of the United States Code. This information will be used to establish your identity for tax purposes.

If your Business Structure is... |

Then the required Ownership/Responsible Party disclosure is... |

|

|

n Sole Proprietorship |

Enter owner’s individual information, including Social Security Number, in |

n Profit Limited Liability Company (LLC) for Federal Purposes Taxed as |

question 15. |

an Individual Sole Proprietorship |

Do not use name abbreviations or nicknames. |

n Professional Limited Liability Company (PLLC) for Federal Purposes |

Taxed as an Individual Sole Proprietorship |

|

n Non-Profit Limited Liability Company (LLC) for Federal Purposes |

|

Taxed as an Individual Sole Proprietorship |

|

|

|

n Qualified Joint Venture |

Enter the information for the married couple, including Social Security |

|

Numbers, in question 15 and 16. |

|

Do not use name abbreviations or nicknames. |

|

|

n Profit Limited Liability Company (LLC) for Federal Purposes Taxed as |

Enter the single member’s company information, including FEIN, in question |

a Single Member Disregarded Entity |

15. |

n Professional Limited Liability Company (PLLC) for Federal Purposes |

|

Taxed as a Single Member Disregarded Entity |

If the LLC has managers, their full individual information can be entered in |

n Non-Profit Limited Liability Company (LLC) for Federal Purposes |

question 16. Attach a separate sheet for more LLC managers. |

Taxed as a Single Member Disregarded Entity |

|

|

|

n Profit Corporation |

Enter the officers’ information, including Social Security Numbers in |

n Professional Service Corporation (PSC) |

questions 15 and 16. If more than two officers, attach a separate sheet. |

n Public Benefit Corporation |

|

n Association |

Note: Information for the President is required. The information for an Officer |

n Cooperative Corporation |

must be for an individual and not another business. |

n Limited Cooperative Association |

|

n Non-Profit Corporation |

|

n Government |

|

|

|

n Unincorporated Non-Profit Association |

Enter the members’/managers’ information in questions 15 and 16. If |

|

members/managers are individuals, provide their Social Security Numbers. |

|

If members/managers are other businesses, provide their FEINs. |

|

If more than two members/managers, attach a separate sheet. |

|

|

n Statutory Trust |

Enter the trustee information in questions 15 and 16. If trustees are |

n Series of a Statutory Trust |

individuals, provide their Social Security Numbers. If trustees are other |

n Business Trust |

businesses, provide their FEINs. If more than two trustees, attach a |

n Trust (non-statutory) |

separate sheet. |

|

For a Series of a Statutory Trust, also provide the information for the master |

|

Statutory Trust under which it was formed, including the FEIN for the master |

|

Statutory Trust. |

|

|

10A100(P)(06-21) |

Page 7 |

|

|

If your Business Structure is... |

Then the required Ownership/Responsible Party disclosure is... |

|

|

n Joint Venture |

Enter the partners’/members’ information in questions 15 and 16. If partners/ |

n General Partnership |

members are individuals, provide their Social Security Numbers. If partners/ |