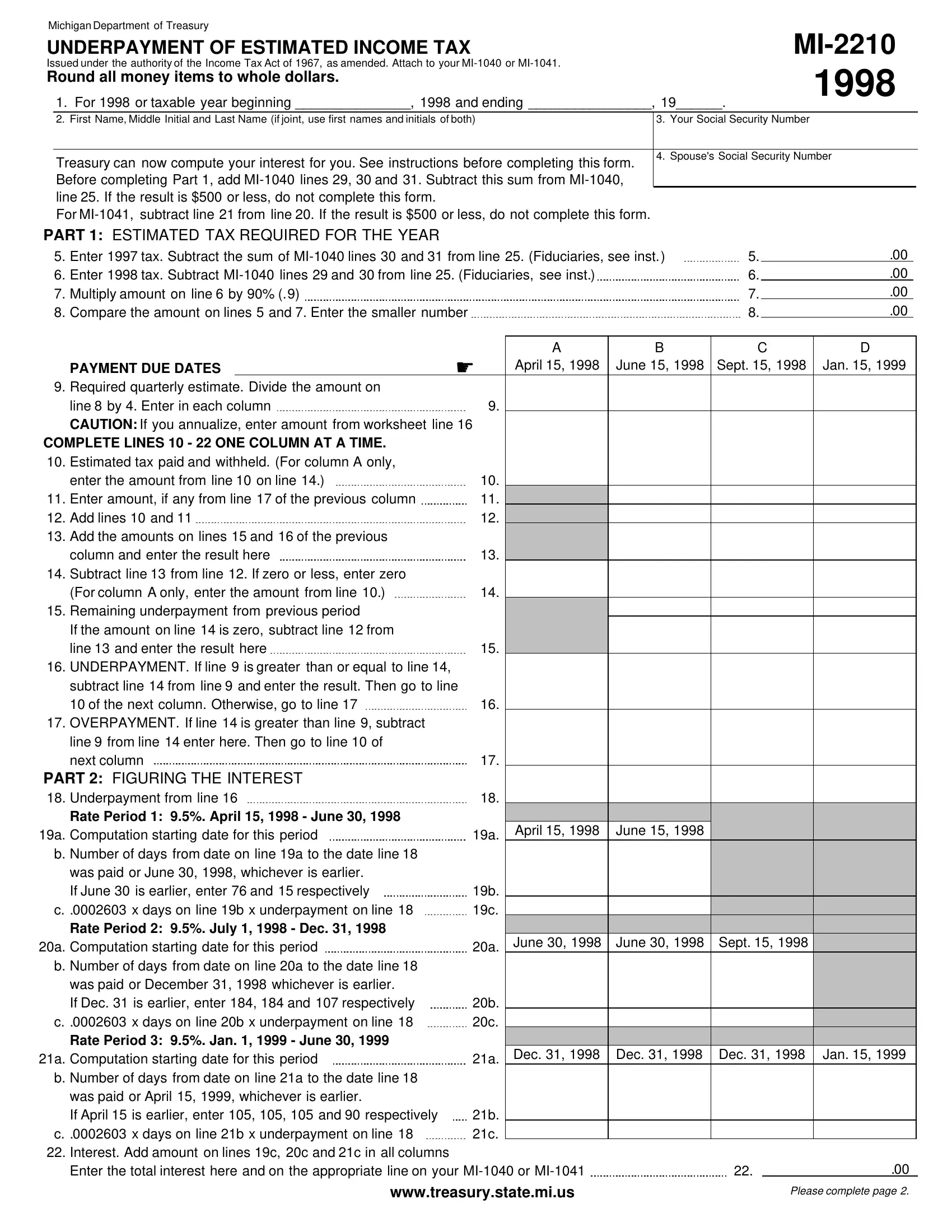

Navigating the intricacies of taxation, the Michigan Department of Treasury provides individuals and fiduciaries with the MI-2210 form, a document critical for calculating penalties and interest due on underpaid estimated income tax. The MI-2210 form serves as a tool for those who either did not make estimated tax payments or who made payments that were either insufficient or not timely across any of the payment periods. This element of the taxation process is particularly pertinent for individuals who have an uneven income distribution throughout the year, offering the opportunity to annualize income and potentially mitigate penalties. Additionally, special considerations are afforded to farmers, fishermen, and seafarers, acknowledging the unique nature of their income flow. The form breaks down the calculation process into digestible sections, starting with figuring the underpayment, moving on to calculating the interest owed based on specific time frames and rates, and concluding with penultimate calculation triggered by payment discrepancies. At its core, the MI-2210 emphasizes the importance of meticulous financial planning and adherence to tax payment schedules, underscored by the potential financial ramifications of disregarding the same.

| Question | Answer |

|---|---|

| Form Name | Michigan Mi 2210 Form |

| Form Length | 4 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 1 min |

| Other names | mi 2210 annualized income worksheet, annualize, mi 2210, michigan form mi 2210 instructions |