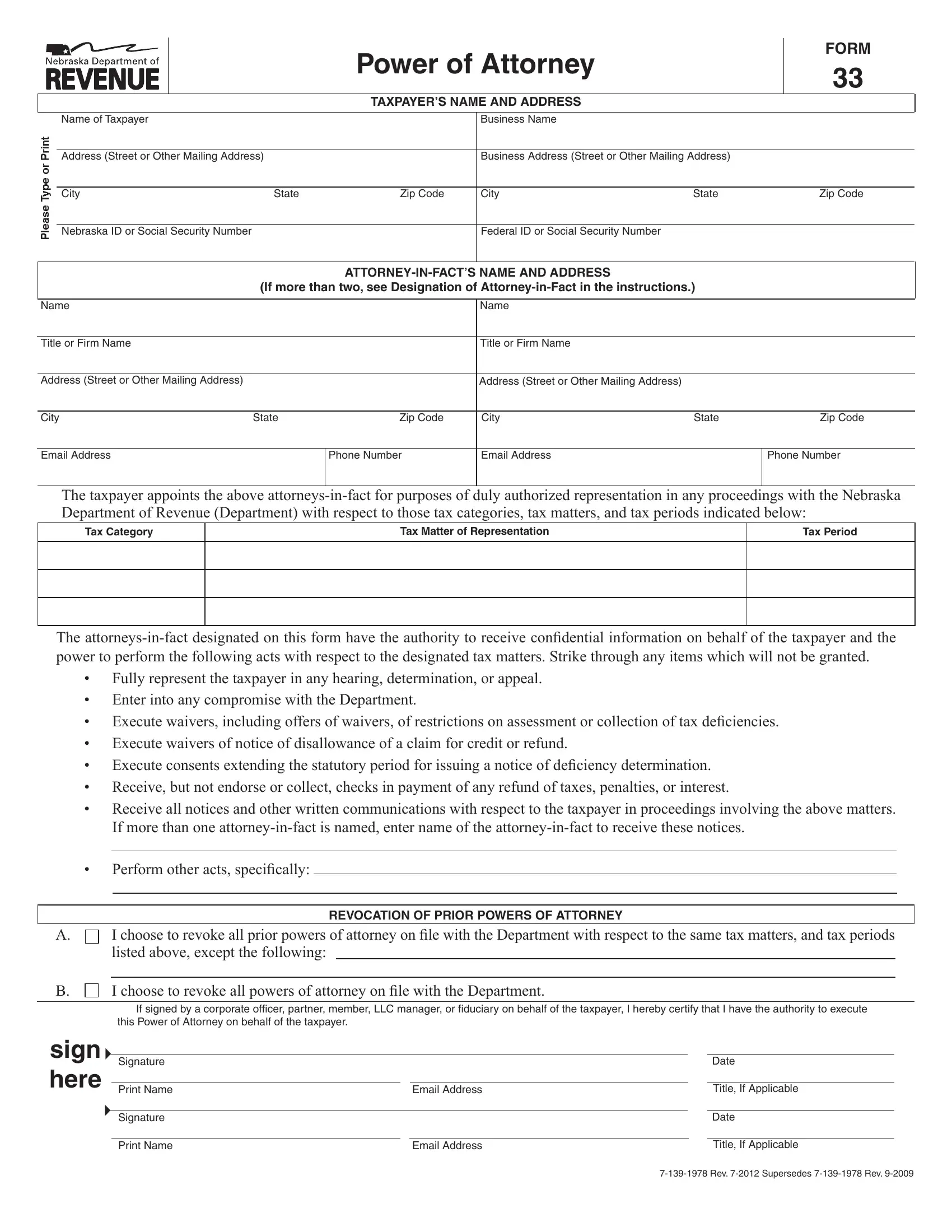

Navigating tax affairs can be complex, and for individuals and businesses in Nebraska looking to authorize another party to manage these matters on their behalf, Form 33 serves as a crucial instrument. This Power of Attorney (POA) form, provided by the Nebraska Department of Revenue, allows taxpayers to designate attorneys-in-fact, granting them the authority to represent the taxpayer in dealings with the Department. These dealings encompass a wide range of tax matters, from hearings and appeals to requests for tax refunds. Details required on the form include taxpayer and attorney-in-fact names and addresses, along with the specific tax matters and periods for which representation is authorized. Importantly, the form also outlines the extent of authority granted to the attorney-in-fact, including receiving confidential tax information and executing agreements. Taxpayers have the option to revoke previous POAs, ensuring that representation is current and reflects their present needs. Additionally, Form 33 must be filed with the appropriate details and signatures before any representation occurs, ensuring that all legal bases are covered. By completing and submitting Form 33, taxpayers in Nebraska can effectively manage their tax affairs through trusted representatives, simplifying what can often be a complicated process.

| Question | Answer |

|---|---|

| Form Name | Nebraska Form 33 |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | nebraska power of attorney form 33, nebraska form 33, E-Mail, Iowa |