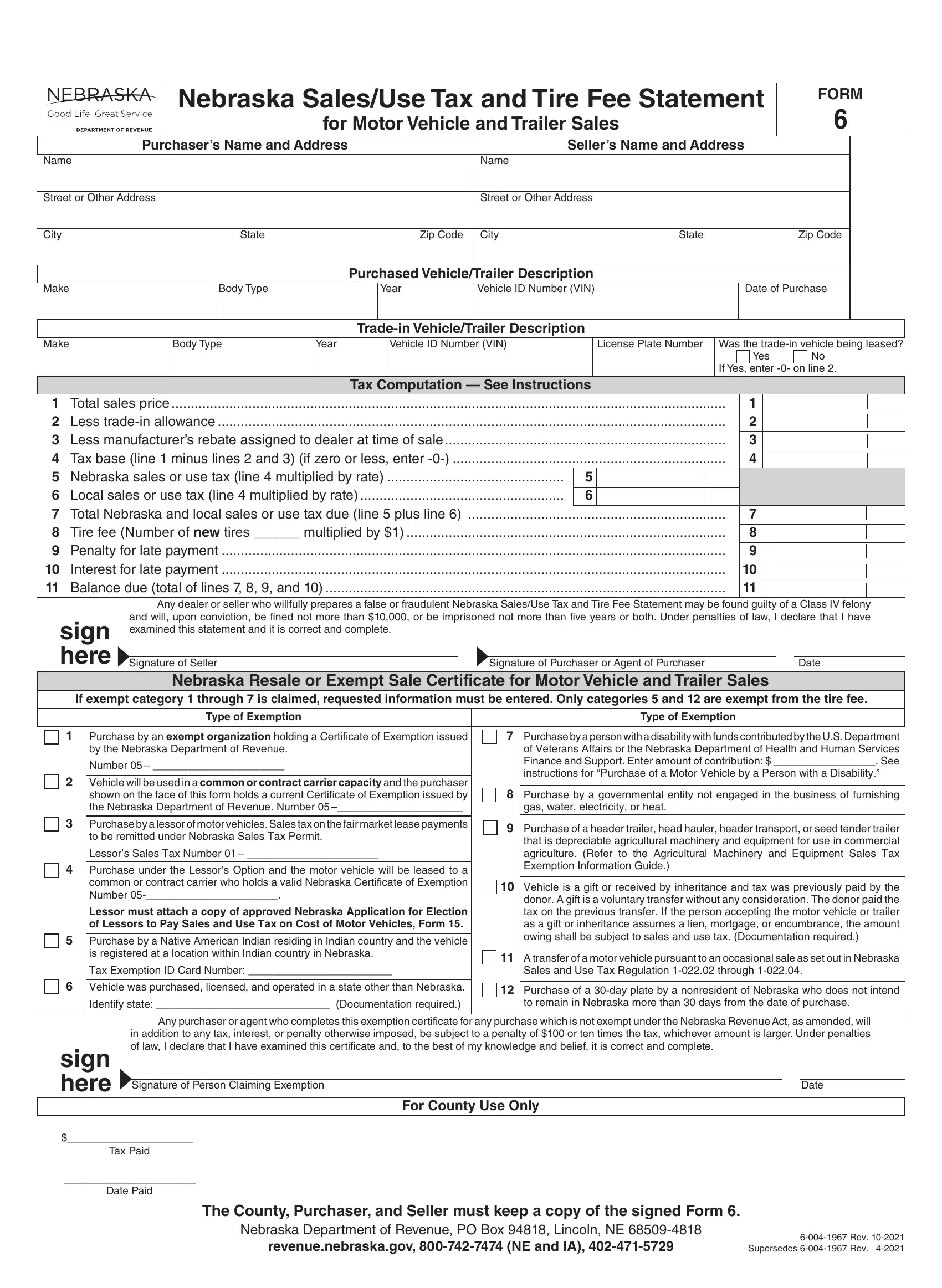

The Nebraska 6 form serves a crucial role in the documentation and taxation process for the sale and purchase of motor vehicles and trailers in the state of Nebraska. Officially known as the Nebraska Sales/Use Tax and Tire Fee Statement for Motor Vehicle and Trailer Sales, this form requires comprehensive details from both the purchaser and seller, including names, addresses, and specific vehicle or trailer information such as make, body type, year, and the Vehicle Identification Number (VIN). Additionally, it outlines the method for computing the applicable sales or use taxes alongside the tire fee, taking into account factors like trade-in allowance and manufacturer’s rebates. It's designed to ensure that the correct amount of taxes and fees are collected at the time of sale, with penalties in place for late payment, detailed instructions for the computation of taxes, and clear stipulations for claiming exemptions under specific circumstances. The form also includes stern warnings against fraudulent reporting, highlighting the serious legal repercussions for wrongdoing. Integral to the legal documentation for vehicle sales in Nebraska, the form must be accurately completed and submitted to the relevant county or state authorities, ensuring compliance with Nebraska's tax laws and regulations. Beyond just a simple tax document, the Nebraska 6 form also plays a part in regulating fair trade practices and ensuring the state's fiscal policies are upheld in the context of vehicle sales and purchases.

| Question | Answer |

|---|---|

| Form Name | Nebraska Form 6 |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | revenue.nebraska.govsales-and-use-tax-formsSales and Use Tax FormsNebraska Department of Revenue |