Having the right emergency forms on hand can make all the difference when it comes to quickly and accurately responding to an emergency situation. The RSA 1 Emerg Form is an important document that helps ensure your organization responds correctly in a range of different situations. What makes this form unique is that it covers everything from medical emergencies to security issues, giving you peace of mind knowing everyone will be prepared for any scenario. In this blog post, we'll take a closer look at what this form entails and how it can help keep you, your staff, and anyone else involved safe during emergencies. Read on to learn more about why having an RSA 1 Emerg Form should be part of every team's emergency protocol!

| Question | Answer |

|---|---|

| Form Name | Rsa 1 Emerg Form |

| Form Length | 3 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 45 sec |

| Other names | deferrals, EMERG, rsa, unforeseeable |

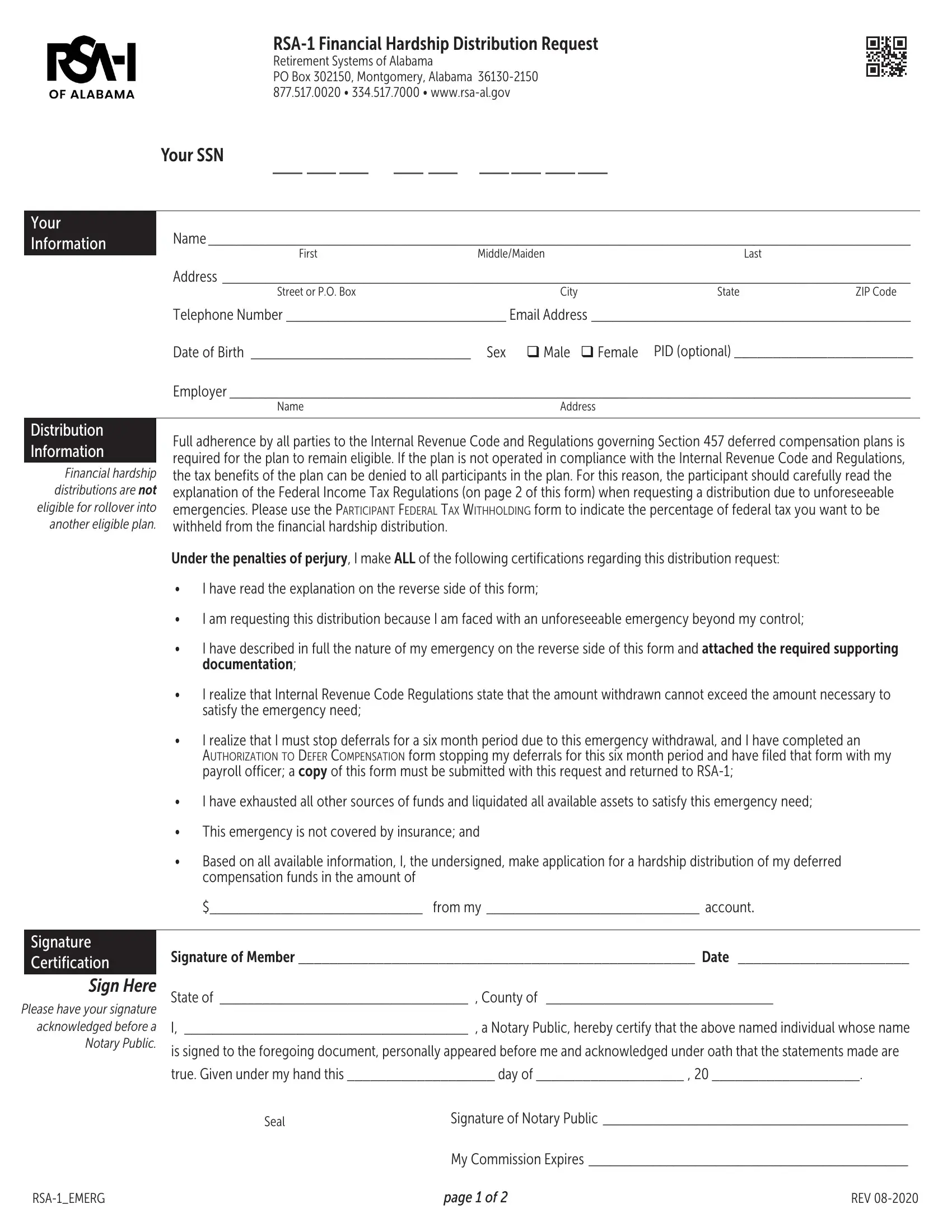

FINANCIAL HARDSHIP DISTRIBUTION REQUEST

Retirement Systems of Alabama

P. O. Box 302150 Montgomery, AL

Name

|

|

|

First |

|

Middle/Maiden |

Last |

|

|

||

Address |

|

|

|

|

|

|

||||

|

|

|

|

|

Street or P. O. Box |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City |

|

State |

|

|

Zip Code |

|

||

Social Security No. |

Phone Number |

Date of Birth |

|

|

||||||

|

|

|

|

|

|

|

|

Month |

Day |

Year |

Employer’s Name and Address _____ |

______________________________________________________ |

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

Notice: Full adherence by all parties to the Internal Revenue Code and Regulations governing Section 457 deferred compensation plans is required for the plan to remain eligible. If the plan is not operated in compliance with the Internal Revenue Code and Regulations, the tax benefits of the plan can be denied to all participants in the plan. For this reason, the participant should carefully read the explanation of the Federal Income Tax Regulations contained on the reverse side of this form when requesting a distribution due to unforeseeable emergencies.

Under the penalties of perjury, I make ALL of the following certifications regarding this distribution request:

∙I have read the explanation on the reverse side of this form;

∙I am requesting this distribution because I am faced with an unforeseeable emergency beyond my control;

∙I have described in full the nature of my emergency on the reverse side of this form and attached the required supporting documentation;

∙I realize that Internal Revenue Code Regulations state that the amount withdrawn cannot exceed the amount necessary to satisfy the emergency need;

∙I realize that I must stop deferrals for a six (6) month period due to this emergency withdrawal, and I have completed an

“Authorization to Defer” form stopping my deferrals for this six (6) month period and have filed that form with my payroll officer; a copy of this form must be submitted with this request and returned to

∙I have exhausted all other sources of funds and liquidated all available assets to satisfy this emergency need;

∙This emergency need is not covered by insurance; and

∙Based on all available information, I, the undersigned, make application for a hardship distribution of my deferred compensation funds in the amount of $ ______________.

Signature of |

_ ______ Date _______________ |

|||||

STATE OF |

|

|

, COUNTY OF |

|

|

|

On this _____________day of ____________________, 20______ before me, the undersigned authority, a Notary Public in and for

said County and State, personally appeared the applicant for distribution, known to me to be the person whose name is subscribed to the foregoing instrument, and declared to me upon oath that the foregoing instrument is true and correct.

|

Signature of Notary Public ________________________________________________ _ |

|

Seal |

My Commission Expires |

|

DEFERRED COMPENSATION PLAN DISTRIBUTIONS DUE TO UNFORESEEABLE EMERGENCIES

Your

According to Federal Income Tax Regulations, an unforeseeable emergency is a severe financial hardship to the participant or his dependent (for federal income tax purposes) resulting from:

1.A sudden and unexpected illness or accident,

2.Loss of property due to flood, fire or windstorm, or

3.Other similar extraordinary and unforeseeable circumstances arising as a result of events beyond the control of the participant.

Federal Income Tax Regulations provide that payment from deferred compensation may not be made to the extent such hardship is or may be relieved:

1.Through reimbursement or compensation by insurance or otherwise,

2.By liquidation of the participant’s assets, to the extent the liquidation of such assets would not itself cause

severe financial hardship, or

3.By cessation of deferrals under the plan.

Withdrawals because of an unforeseeable emergency are permitted ONLY to the extent reasonably needed to satisfy the emergency need.

Sending a child to college and/or purchasing a home are specifically listed in the Federal Income Tax Regulations as not

qualifying as unforeseeable emergencies.

Please describe in full the nature of your emergency (attach additional sheets if necessary). Documentation supporting your request must be attached.

Name of Member (Print)

Signature of |

|

Date |