Working with PDF documents online is certainly very simple with this PDF editor. Anyone can fill out use tax exemption certificate here effortlessly. To make our tool better and more convenient to use, we consistently develop new features, considering feedback from our users. To get the ball rolling, go through these basic steps:

Step 1: First of all, open the pdf editor by pressing the "Get Form Button" in the top section of this page.

Step 2: When you start the editor, you will see the document ready to be filled in. Besides filling in different blanks, you could also do other things with the PDF, such as writing any text, editing the original text, adding illustrations or photos, putting your signature on the document, and a lot more.

It really is simple to fill out the form adhering to our detailed guide! Here is what you should do:

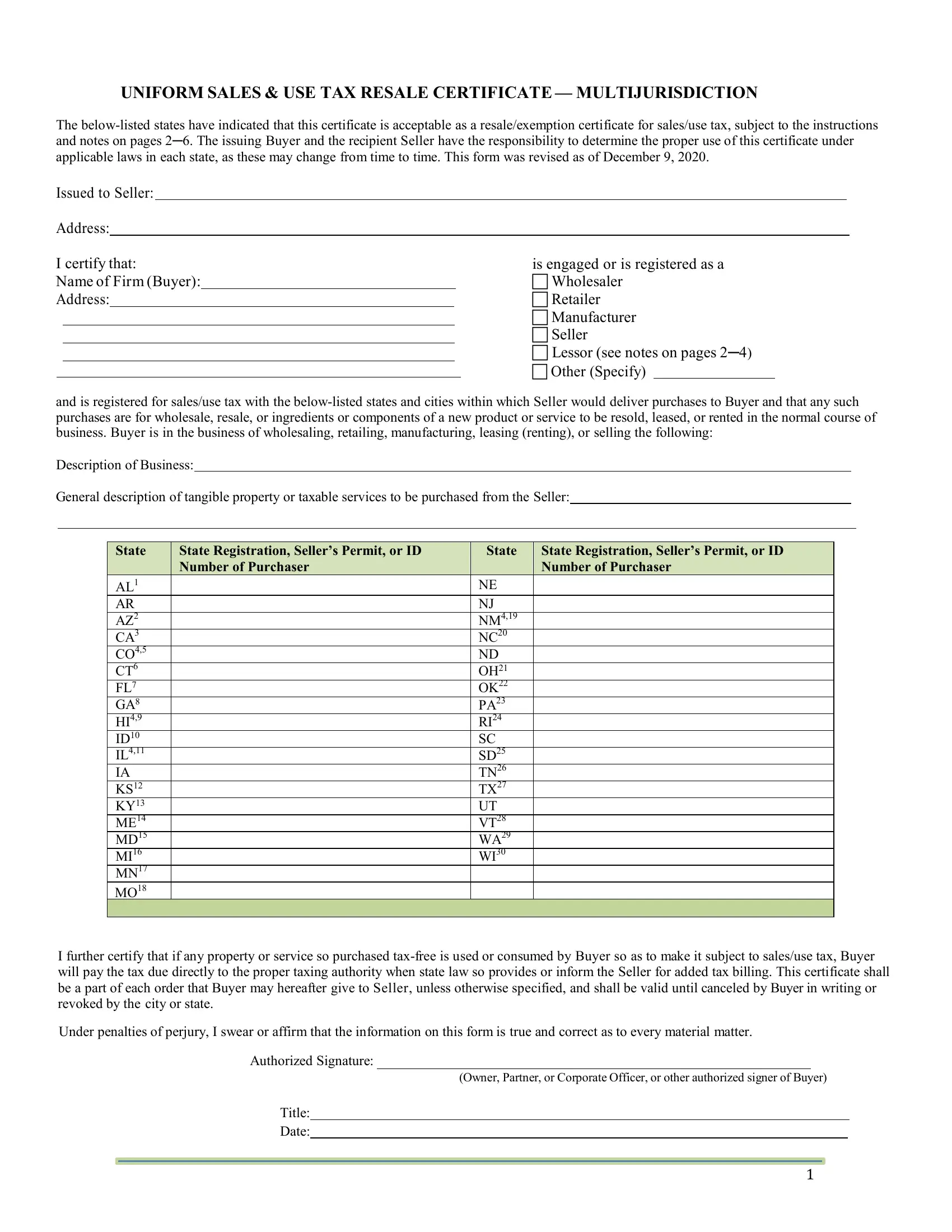

1. To start with, while completing the use tax exemption certificate, start in the part that features the next blank fields:

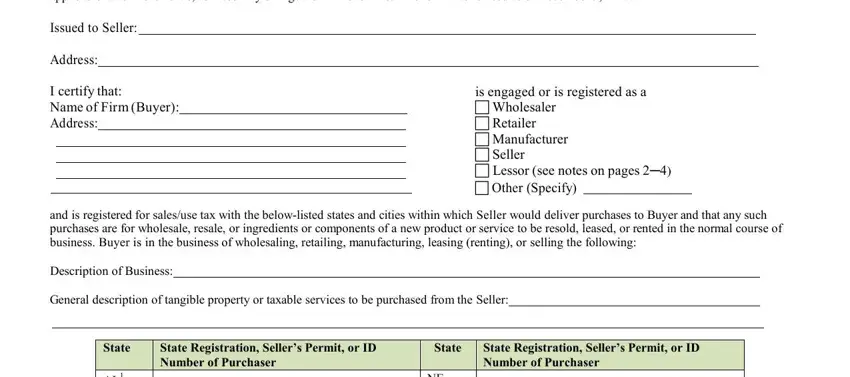

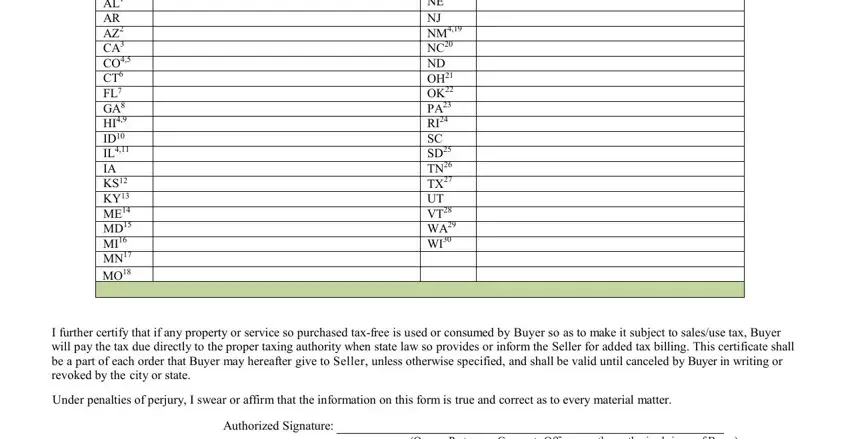

2. The subsequent step would be to fill out the following blanks: AL AR AZ CA CO CT FL GA HI ID IL, NE NJ NM NC ND OH OK PA RI SC SD, I further certify that if any, Under penalties of perjury I swear, Authorized Signature, and Owner Partner or Corporate Officer.

3. In this specific step, check out Owner Partner or Corporate Officer, and Title Date. Every one of these must be taken care of with utmost precision.

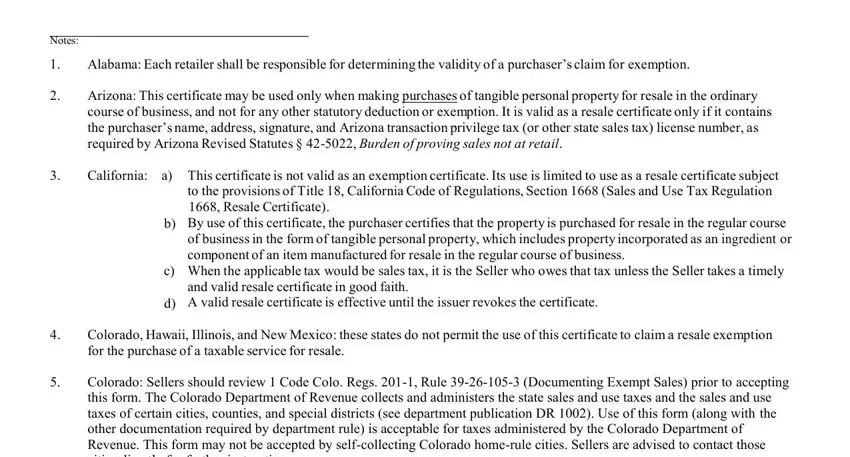

4. The next part requires your information in the subsequent areas: Notes, Alabama Each retailer shall be, Arizona This certificate may be, California a This certificate is, to the provisions of Title, b By use of this certificate the, c When the applicable tax would be, and valid resale certificate in, Colorado Hawaii Illinois and New, and Colorado Sellers should review. Remember to give all of the requested details to go further.

As to Alabama Each retailer shall be and b By use of this certificate the, make sure that you review things in this current part. Those two are certainly the most important ones in this file.

Step 3: Revise what you've inserted in the blanks and then click on the "Done" button. Sign up with us right now and immediately use use tax exemption certificate, available for download. Every last change made is conveniently kept , helping you to edit the document later on if necessary. FormsPal guarantees your data confidentiality with a protected method that never saves or distributes any sort of personal data provided. Be confident knowing your docs are kept protected every time you use our service!