Are you trying to get your taxes in order and feel like you're drowning in paperwork? You may already be aware that the Sc1065 form is an important part of filing business tax returns, but do you know why exactly? Understanding what goes into submitting this form correctly can save precious time - and money! We'll walk through the ins-and-outs of the Sc1065 form: what it is, when it needs to be filed, who has to fill one out, how to do so properly and answer any lingering questions you may have. If a comprehensive guide on filing this special tax return accurately sounds helpful for your current situation then read on.

| Question | Answer |

|---|---|

| Form Name | Sc1065 Form |

| Form Length | 7 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 1 min 45 sec |

| Other names | fillable sc 1065 form, sc 1065, amazon, sc1065 fill in |

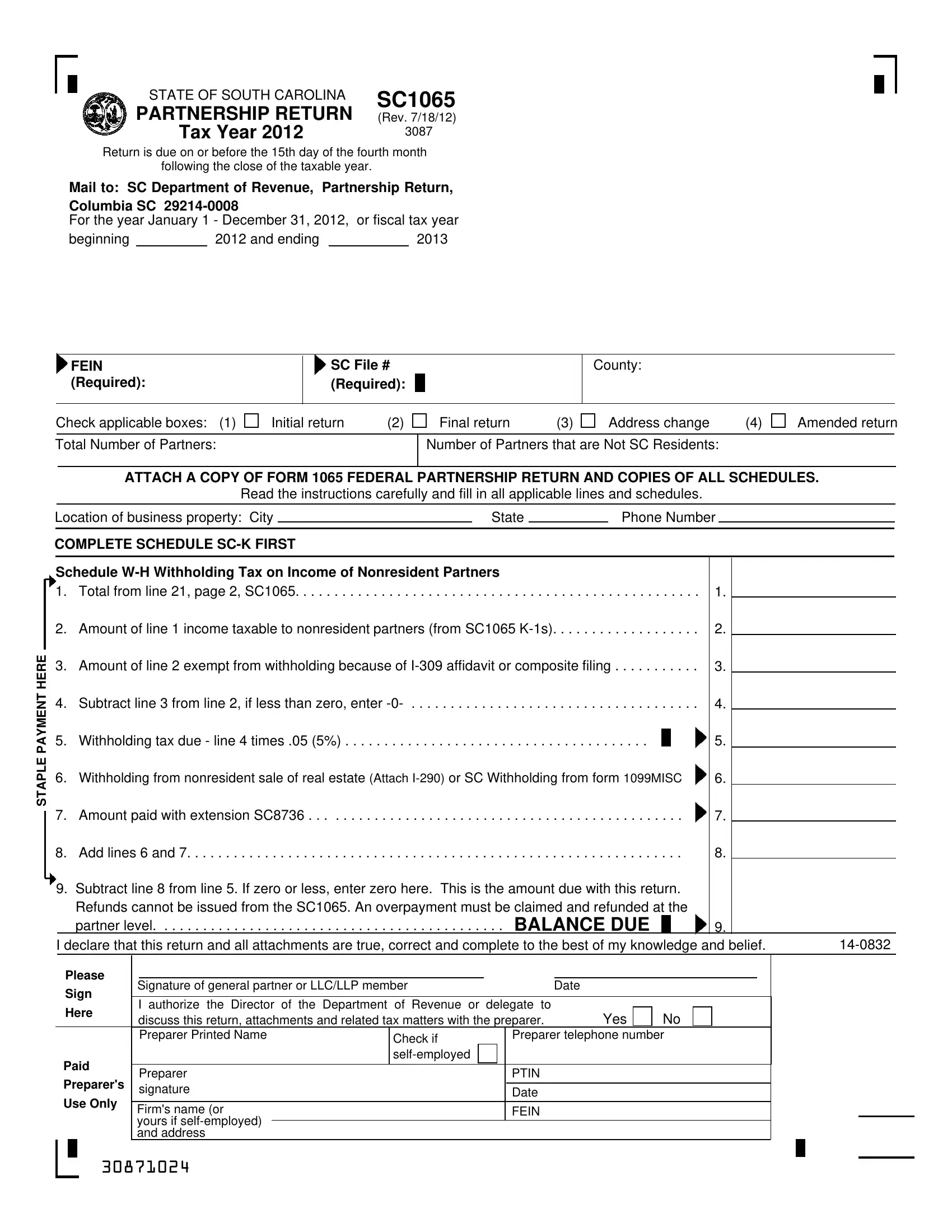

STATE OF SOUTH CAROLINA |

SC1065 |

|

PARTNERSHIP RETURN |

||

(Rev. 7/18/12) |

||

Tax Year 2012 |

3087 |

Return is due on or before the 15th day of the fourth month following the close of the taxable year.

Mail to: SC Department of Revenue, Partnership Return,

Columbia SC |

|

|

|||

For the year January 1 - December 31, 2012, |

or fiscal tax year |

||||

beginning |

|

2012 and ending |

|

|

2013 |

FEIN (Required):

SC File # (Required):

County:

Check applicable boxes: (1) |

Initial return |

(2) |

Final return |

(3) |

Address change |

(4) |

Amended return |

|||

|

|

|

|

|

|

|

|

|

||

Total Number of Partners: |

|

|

Number of Partners that are Not SC Residents: |

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

STAPLE PAYMENT HERE

|

|

ATTACH A COPY OF FORM 1065 FEDERAL PARTNERSHIP RETURN AND COPIES OF ALL SCHEDULES. |

|

|||||||||||

|

|

Read the instructions carefully and fill in all applicable lines and schedules. |

|

|

|

|

||||||||

Location of business property: City |

|

|

State |

|

|

Phone Number |

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

COMPLETE SCHEDULE |

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|||||||

Schedule |

|

|

|

|

|

|

|

|||||||

1. |

Total from line 21, page 2, SC1065 |

. . . . . . . . . . . . . . . . . . |

. . . . . . . |

. . . . . . . . . . |

. . |

. . . . . |

. |

. . . . |

1. |

|

|

|||

2. |

. . . . . . . . . . . . . .Amount of line 1 income taxable to nonresident partners (from SC1065 |

. . . . . |

2. |

|

|

|||||||||

3. |

.Amount of line 2 exempt from withholding because of |

. . . . . |

. . . . . |

3. |

|

|

||||||||

4. |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Subtract line 3 from line 2, if less than zero, enter |

. . . . . |

4. |

|

|

|||||||||

5. |

Withholding tax due - line 4 times .05 (5%) |

|

|

5. |

|

|

||||||||

6. |

Withholding from nonresident sale of real estate (Attach |

6. |

|

|

||||||||||

7. |

. . .Amount paid with extension SC8736 |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

7. |

|

|

|||||||||

8. |

. . . . . . .Add lines 6 and 7 |

. . . . . . . . . . . . . . . . . . |

. . . . . . . |

. . . . . . . . . . . . |

. . . . . . . . |

8. |

|

|

||||||

9.Subtract line 8 from line 5. If zero or less, enter zero here. This is the amount due with this return. Refunds cannot be issued from the SC1065. An overpayment must be claimed and refunded at the

partner level. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . BALANCE DUE |

|

9. |

|

I declare that this return and all attachments are true, correct and complete to the best of my knowledge and belief. |

|||

|

Please |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Signature of general partner or LLC/LLP member |

|

|

|

Date |

|

|

|

|

|

|

|

|

|

|

||||||||

|

Sign |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

I authorize the Director of the Department of Revenue or delegate to |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

Here |

Yes |

|

No |

|

|

|

|

|

|

|

|

||||||||||

|

discuss this return, attachments and related tax matters with the preparer. |

|

|

|

|

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

Preparer Printed Name |

Check if |

|

|

Preparer telephone number |

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

Paid |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

Preparer |

|

|

|

|

PTIN |

|

|

|

|

|

|

|

|

|

|

|

|||||

|

Preparer's |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

signature |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

Date |

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Use Only |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Firm's name (or |

|

|

|

|

FEIN |

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

yours if |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

and address |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

30871024

|

|

|

Form SC1065 |

|

|

|

|

|

|

|

|

|

|

|

|

SCHEDULE |

PARTNERS' SHARES OF INCOME (LOSSES), DEDUCTIONS, CREDITS ETC. (See instructions.) |

|

|||||||

|

|

|

* Enter amounts from corresponding lines on your federal Schedule K in Column A. |

|

|

|

|

|||||

|

|

|

(A)* |

(B) |

|

(C) |

|

(D) |

|

(E) |

|

|

|

|

|

|

|

|

|

|

|

|

Amounts Subject |

|

|

|

|

|

|

Plus or Minus |

Federal Schedule K |

|

Amounts |

|

to Apportionment |

|

|

|

|

|

|

Amounts From |

South Carolina |

Amounts After |

|

Allocated to SC |

DO NOT Include amounts |

|

|

||

|

|

|

Federal Schedule K |

Adjustment |

SC Adjustments |

|

|

allocated to other states |

|

|

||

|

|

|

Ordinary Business Income (loss) |

|

|

|

|

|

|

|

|

|

1 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net Real Estate Rents (loss) |

|

|

|

|

|

|

|

|

|

2 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Other Net Rents (loss) |

|

|

|

|

|

|

|

|

|

3 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Guaranteed Payments |

|

|

|

|

|

|

|

|

|

4 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Interest Income |

|

|

|

|

|

|

|

|

|

5 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Dividends |

|

|

|

|

|

|

|

|

|

6 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Royalties |

|

|

|

|

|

|

|

|

|

7 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net Short Term Cap. Gain (loss) |

|

|

|

|

|

|

|

|

|

8 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net Long Term Cap. Gain (loss) |

|

|

|

|

|

|

|

|

|

9 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net § 1231 gain (loss) |

|

|

|

|

|

|

|

|

|

10 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Other Income (loss) |

|

|

|

|

|

|

|

|

|

11 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

§ 179 Deduction |

|

|

|

|

|

|

|

|

|

12 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Contributions |

|

|

|

|

|

|

|

|

|

13a |

|

|

|

|

|

|

|

|

|

|

||

|

|

|

Investment Interest Expense |

|

|

|

|

|

|

|

|

|

13b |

|

|

|

|

|

|

|

|

|

|

||

|

|

|

§ 59 (e)(2) Expenditures |

|

|

|

|

|

|

|

|

|

13c |

|

|

|

|

|

|

|

|

|

|

||

|

|

|

Other Deductions |

|

|

|

|

|

|

|

|

|

13d |

|

|

|

|

|

|

|

|

|

|

||

|

|

|

Total |

|

|

|

|

|

|

|

|

|

14 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

15. Amounts from federal Schedule K (line 14, Schedule |

15 |

|

|

|

|||||

|

|

|

16. Amount Allocated to South Carolina (from line 14, Schedule |

16 |

|

|

|

|||||

|

|

|

17. Net income (loss) subject to apportionment (from line 14, Schedule |

17 |

|

|

|

|||||

|

|

|

APPORTIONMENT |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

TOTAL |

|

SC |

|

|

|

|

|

|

|

18. Total Sales or Gross Receipts |

|

|

|

|

|

|

|

||

|

|

|

19. Apportionment factor (SC ÷ TOTAL). 100% if operating entirely within SC |

19 |

% |

|

|

|||||

|

|

|

20. Net business income (loss) apportioned to SC (line 17 multiplied by line 19) |

20 |

|

|

|

|||||

|

|

|

|

|

|

|

|

|||||

|

|

|

21. Net business income (loss) taxable to SC (line 16 plus line 20) |

21 |

|

|

|

|||||

30872022

INSTRUCTIONS FOR PARTNERSHIP INCOME TAX RETURN

South Carolina Department of Revenue SC1065

The references to line numbers and form numbers on federal income tax forms were correct at the time of printing. If they have changed and you are unable to determine the proper line to use, please contact the Department of Revenue. These instructions are to be used as a guide in the preparation of a South Carolina partnership income tax return and are not intended to cover all provisions of the law.

CHANGE IN APPORTIONMENT METHOD

Beginning with Tax Year 2011, manufacturers, sellers, distributors, and renters of tangible property must use the sales ratio for apportionment purposes. The apportionment method for tax years before 2007 had been

A.Who Must File - Every partnership (including any multiple member LLC not taxed as a corporation), domestic or foreign, doing business or owning property in South Carolina must file SC1065. Partnership income or loss is computed in the same manner and on the same basis as for an individual. Taxpayers carrying on business in a partnership are liable for income tax in their individual capacities. Each partner's return shall include his distributive share, whether distributed or not, of the net income or loss of the partnership for the taxable year. If a partner and partnership have different taxable years, the partner’s return shall include income or loss reported by the partnership during the partner’s taxable year.

B.Registration Information – A newly formed partnership can be registered by using the Business One Stop

C.Filing Requirements - File SC1065 and include the amount required to be withheld to the Department of Revenue by the 15th day of the fourth month following the end of the partnership’s taxable year. Within the same deadline, provide each nonresident partner with a federal Form

D.Balance Due With Return - Payment must be made for any balance due amount calculated on the return. Make the check payable to the “SC Department of Revenue.” Write the file number or federal employer identification number (FEIN) and “SC1065 and the year of the tax return” on the payment. Staple the payment to the front of the form in the indicated area. NOTE: refunds cannot be claimed through SC1065. An overpayment must be claimed and refunded at the partner level.

E.How To Obtain Past Year Forms – Past year SC1065 partnership forms can be found on our website www.sctax.org by clicking on Quick Links, Forms and Instructions, and then Past Years Tax Forms and Instructions.

F.Composite Filing - A composite return is a single nonresident individual income tax return filed by a partnership on behalf of two or more nonresident partners who are individuals, trusts or estates. See SC form

G.Extensions - A partnership may request an extension of time to file SC1065 by filing SC8736 by the 15th day of the fourth month following the end of the partnership’s taxable year. When filing SC8736, include withholding of 5% of income taxable to South Carolina on all nonresident partners. However, you are not required to withhold on behalf of partners that

(a)participate in a composite return, or (b) provide an

1

H.Composite Extensions - In order to extend the time allowed for filing a composite return, file SC4868 using the name and FEIN of the partnership, estimate the tax due, and pay the tax estimate on or before the 15th day of the 4th month following the end of the partner’s taxable year. Do not use the SC8736 to extend the time allowed to file a composite return, file SC4868 instead. For tax years after 2004, nonresident partners may participate in composite returns even if they have other sources of income taxable to South Carolina. Disregard the other sources of income taxable to South Carolina when preparing the composite return. For more detailed information, see SC Revenue Procedure

I.Information To Be Furnished To Partners - Supply SC1065

J.Acceptable Forms of

K.Tax Credits - Enter

L.Allocation and Apportionment of Income: A taxpayer whose entire business is transacted or conducted in SC is subject to income tax based on the entire taxable income of the business for the taxable year. A taxpayer that transacts or conducts its business partly within and partly outside of SC is subject to income tax based on the portion of its business carried on in SC. This portion is determined through allocation and apportionment of income. SC Code

1.A “sales only” apportionment method for taxpayers whose principle business in SC is dealing in tangible personal property. This method is used by businesses that manufacture, sell, or rent tangible personal property. The SALES factor is all sales of goods, merchandise and property in South Carolina to anyone other than the US government, divided by total sales everywhere. The sale takes place where goods are received by the purchaser or his designee after all transportation is completed. Sales in South Carolina include all rentals not allocated from tangible personal property located in South Carolina and sales of intangible personal property and receipts from services of

2.A “gross receipts” apportionment method for taxpayers not dealing in tangible personal property. This method is used by financial businesses and service businesses, including businesses that install or repair tangible personal property, and contractors. This apportionment factor is SC gross receipts divided by gross receipts everywhere. See SC Code

3.A “special” apportionment method provided in SC Code

4.A taxpayer may apply pursuant to SC Code

See our publication South Carolina Tax Incentives for Economic Development for details. This publication can be found on our website at www.sctax.org under Publications, Information for Tax Professionals.

2

M. Completing the SC1065

Print or type the legal name and address of the partnership.

Both FEIN and SC File numbers are required. If the SC File number has not been assigned by the South Carolina Department of Revenue, refer to the Registration Information included in these instructions. For FEIN information, contact the Internal Revenue Service.

Enter the county where the partnership is located.

Check the boxes that apply:

1.Initial Return – mark this box if this return is the first SC1065 filed for this entity.

2.Final Return – mark this box if this return is the last SC1065 that will be filed for this entity. Marking this box will allow us to close the partnership account. The Account Closing Form C278 should be filed to close any other tax accounts for this entity such as Sales or Employer Withholding.

3.Address Change – mark this box if the address shown on this return is different than the address on the last SC1065 filed or than on any other address documentation sent to our office. Form SC8822 should be submitted to change the address on any other tax accounts for this entity such as Sales or Employer Withholding.

4.Amended Return – mark this box if this return amends a previously filed return for this period.

The SC1065 is a four step process described below in general terms. Step by step instructions follow these brief descriptions.

1.Complete Schedule

2.Complete the Apportionment, lines

3.Complete SC1065

4.Complete Schedule

3

STEP 1

COMPLETING THE SCHEDULE

Schedule

Column A Computation of Income: Enter the amounts from Column A of federal Schedule K, lines 1 through 13d in the same line numbers of Column A of

Column B South Carolina Adjustment: Include in Column B additions and subtractions resulting from differences between federal and South Carolina law. Show any income taxed by South Carolina but not subject to federal income tax, such as interest income received from states other than South Carolina, or their political subdivisions as an addition. Some other examples of additions are:

Expenses deducted on the federal return related to income exempt or not taxable to SC.

Federal bonus depreciation. For the year an asset is placed in service, add back the difference between the depreciation taken and the depreciation that would have been allowed without bonus depreciation. A subtraction resulting from a higher SC basis applies to all remaining years of depreciation.

A nonresident seller of South Carolina real property who elects out of installment sales treatment must report the entire gain for the taxable year in which the sale took place. Show any income not taxed by South Carolina but subject to federal income tax, such as interest paid by the US government on US savings bonds, treasury bills etc. as a subtraction.

Total Column B lines 1 - 13d and enter on line 14.

Column C Federal Schedule K Amounts after SC Adjustments: This amount is the sum of Columns A and B.

Column D Allocation of Income: Allocation and apportionment statutes are located in SC Code Sections

Personal service income: Allocate personal service income, including guaranteed payments, to South Carolina if (a) the income is received by a resident individual or (b) the income is for services performed in South Carolina.

Gains and losses from sale of property: Allocate gains and losses from the sale of real property, less all related expenses, to the state in which the real property is located, except that the amount of gain which represents the return of amounts deducted in South Carolina as depreciation is allocated to South Carolina. If a taxpayer’s business is conducted partly within and partly without South Carolina, allocate gains and losses from sales of tangible personal property unrelated to the business activity of the taxpayer to the state in which the business situs of the investment is located, unless the business situs of the investment is partly within and partly without South Carolina. Allocate gains and losses from sales of intangible personal property not connected with the business of the taxpayer and not held for sale to customers in the regular course of business to a corporate partner’s principal place of business and a noncorporate partner’s domicile.

Rents and royalties: Allocate rents and royalties from the lease of rental real estate or tangible personal property not used or connected with the taxpayer’s trade or business during the year, less all related expenses, to the state where the property was located at the time the income was derived.

Interest and dividends: Allocate interest and dividends not connected with the taxpayer’s business, less all related expenses, to a corporate partner’s principal place of business and a noncorporate partner’s domicile.

Other income subject to allocation: Any income, less all related expenses that are not otherwise allocated and that are unrelated to a taxpayer’s business activity conducted partly within and partly without this State is allocated to the state in which the business situs of the investment is located. If the business situs of the investment is partly within and partly without South Carolina, the investment is apportioned using the same formula used for apportioning the net income of the corporation.

Total Column D lines 1 - 13d and enter on line 14.

Column E Amounts Subject to Apportionment: Enter the amounts in Column E that are not allocated to South Carolina or any other state. These amounts are subject to apportionment. Total Column E lines 1 – 13d and enter on line 14.

Line 15 – Enter the amounts from federal Schedule K on line 14, Schedule

Line 16 – Enter the amounts allocated to South Carolina from line 14, Schedule

Line 17 – Enter the Net income (loss) subject to apportionment from line 14, Schedule

4

STEP 2

APPORTIONMENT

Line 18 - Enter total sales or gross receipts in the first column and SC sales or gross receipts in the second column.

Line 19 -

Line 20 -

Line 21 -

STEP 3

COMPLETING THE SC1065

General purpose: SC1065

See the SC1065

Enter the amount of income taxable to nonresident partners on line 2 of Schedule

STEP 4

COMPLETING SCHEDULE

INCOME OF NONRESIDENT PARTNERS

Important:

Line 1 – Enter the net business income (loss) taxable to South Carolina from line 21, page 2 of form SC1065.

Line 2 – Enter the amount of line 1 income taxable to nonresident partners. (From SC1065

Line 3 – Enter any portion from line 2 which would be exempt from withholding due to form

Line 6 – Enter the amount of withholding from nonresident seller real estate or South Carolina withholding from form

Line 7 – Enter the amount paid with extension request, form SC8736.

Line 9 – Subtract line 8 from line 5. If zero or less, enter zero. This is the amount due with this return.

PLEASE NOTE: Refunds cannot be issued from form SC1065 since this is an information return only. Any overpayment must be claimed and refunded at the partner(s) level.

5