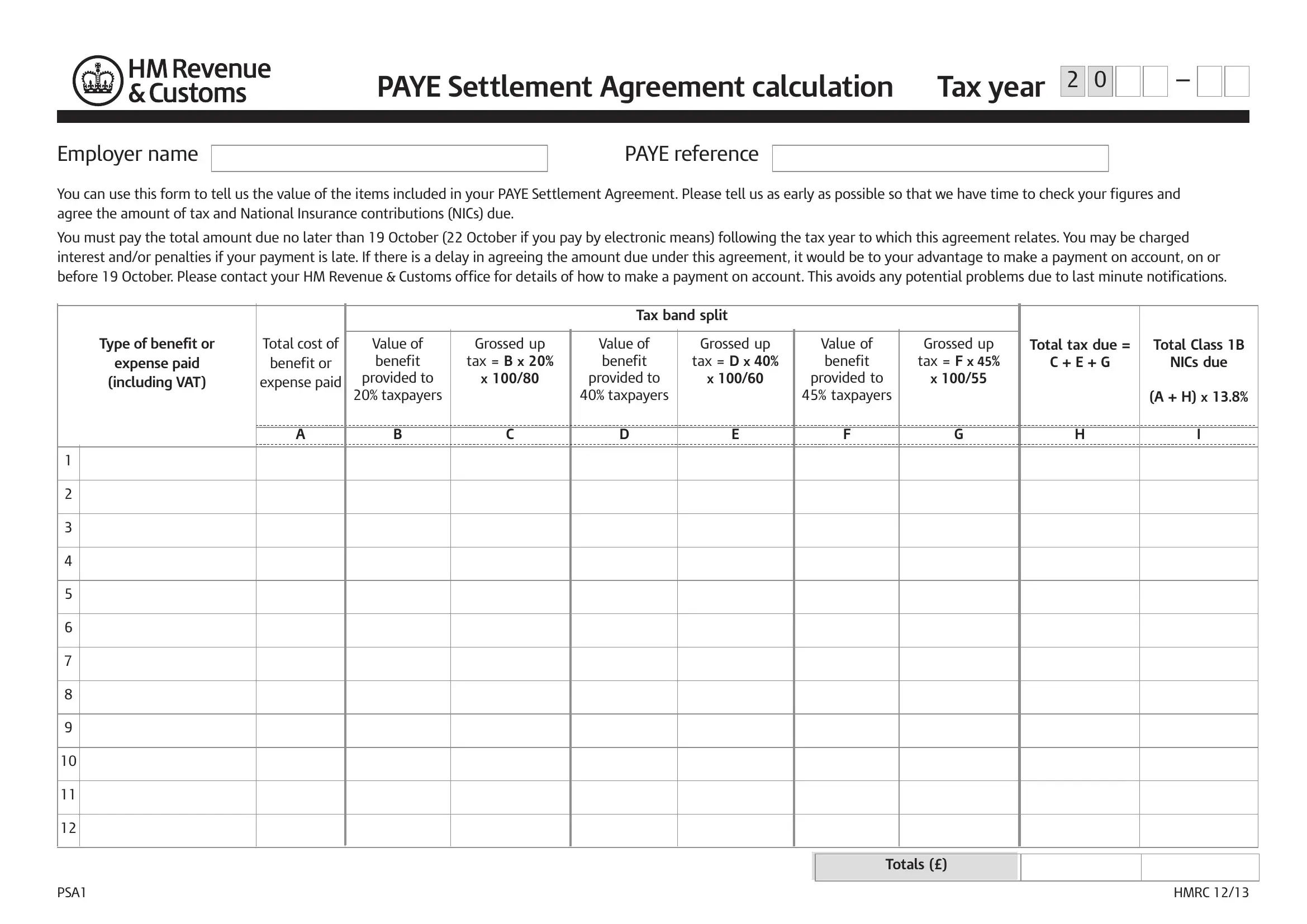

In the complex world of employment taxation, navigating the intricacies of settlements can be a daunting task. The PAYE Settlement Agreement calculation form serves as a vital tool for employers, simplifying this process significantly. It's designed to provide HM Revenue & Customs (HMRC) with detailed information about the taxable items included in the PAYE Settlement Agreement for a specific tax year. Employers must diligently record the value of each benefit or expense paid, helping HMRC to determine the precise amount of tax and National Insurance contributions (NICs) due. The form insists on timely submission, ideally well before the payment deadline of 19 October—or 22 October for those opting for electronic payment methods—to avoid potential interest and/or penalties. Moreover, the form outlines a method to calculate taxes and NICs based on the tax bands of the recipients, ensuring accuracy in the grossed-up value of benefits provided. In instances where the final settlement amount might be delayed, employers are encouraged to make a payment on account by the due date to mitigate against any unforeseen issues. This prudent approach underscores the importance of early and transparent communication with HMRC, aiming to foster a smooth settlement process.

| Question | Answer |

|---|---|

| Form Name | Settlement Agreement Calculation Form |

| Form Length | 1 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 15 sec |

| Other names | hmrc psa1, settlement agreement calculator, paye settlement agreement calculator, psa1 form 2020 21 |