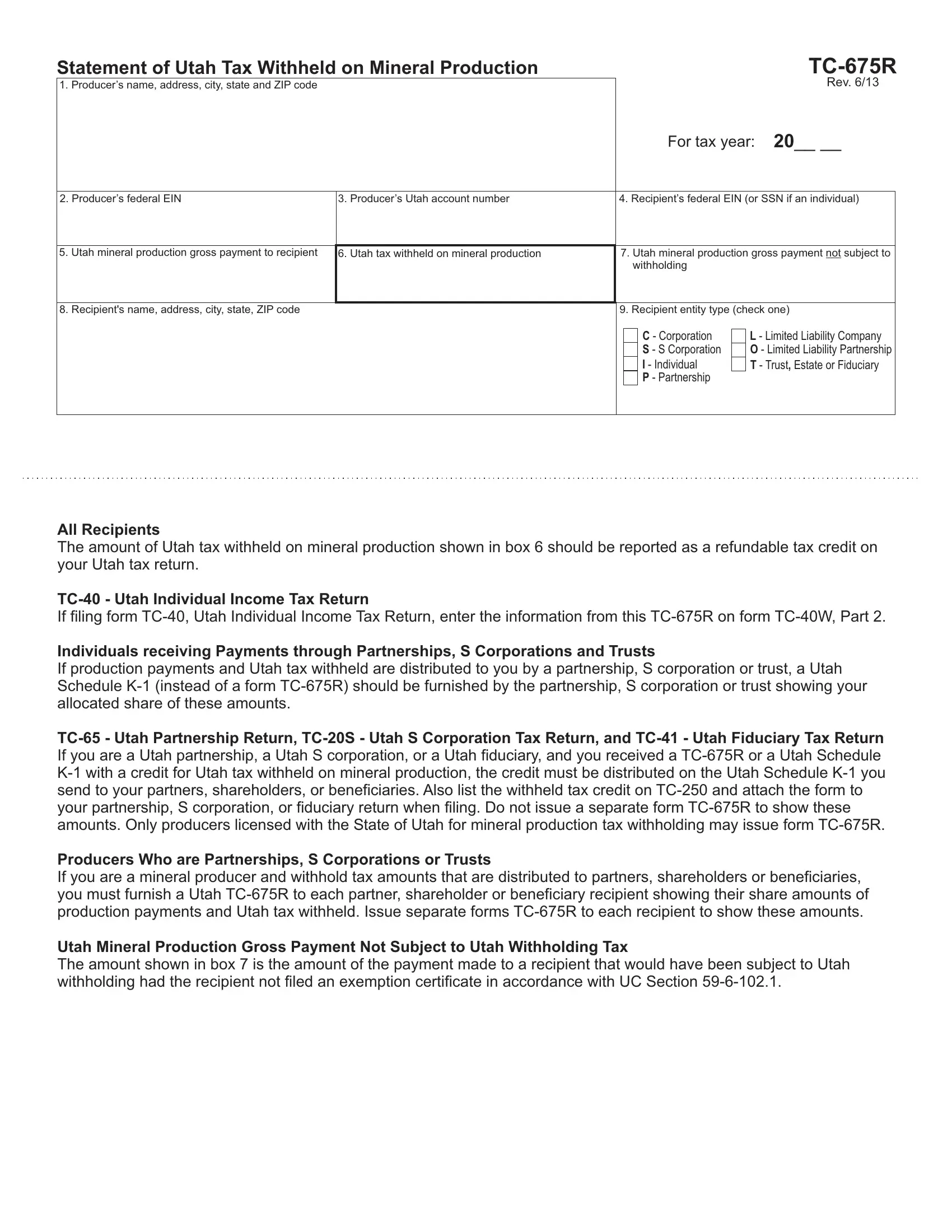

In exploring the intricacies of tax compliance within Utah, especially in the domain of mineral production, the TC-675R form stands out as a critical document. This form, officially titled "Statement of Utah Tax Withheld on Mineral Production," serves multiple functions, primarily aimed at reporting Utah state tax withheld from payments to entities involved in mineral production. It encapsulates comprehensive details such as the producer's and recipient's names, addresses, and federal identification numbers, alongside specifics about the Utah mineral production's gross payments and the tax withheld. Notably, the form is applicable for various entity types, including corporations, limited liability companies, partnerships, and individuals, indicating its broad relevance across the industry. Additionally, the form outlines procedures for reporting withheld tax as a refundable credit on Utah tax returns, balancing between leveraging direct filings and the distribution of credits through entities like partnerships, S corporations, and trusts. With guidelines for both recipients and producers on handling these tax credits, coupled with stipulations for payments not subjected to withholding under certain exemptions, the TC-675R form embodies a pivotal element of Utah's tax structure related to mineral production. By offering a structured approach for tax reporting and credit allocation, the form facilitates compliance, ensuring entities accurately account for and report their tax obligations within the state’s mineral production sector.

| Question | Answer |

|---|---|

| Form Name | Tc 675R Form |

| Form Length | 1 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 15 sec |

| Other names | tc form, nyc tc form tc 140, K-1, allocated |