You'll be able to complete Tennessee Form Inh 300 without difficulty with our PDFinity® online tool. In order to make our tool better and easier to work with, we consistently come up with new features, with our users' suggestions in mind. All it requires is several easy steps:

Step 1: Click on the orange "Get Form" button above. It is going to open our editor so you could begin filling in your form.

Step 2: With the help of this advanced PDF editor, you are able to accomplish more than simply complete blank form fields. Edit away and make your documents appear professional with custom textual content added, or tweak the original content to perfection - all backed up by the capability to add your personal images and sign the PDF off.

As for the blanks of this particular PDF, this is what you want to do:

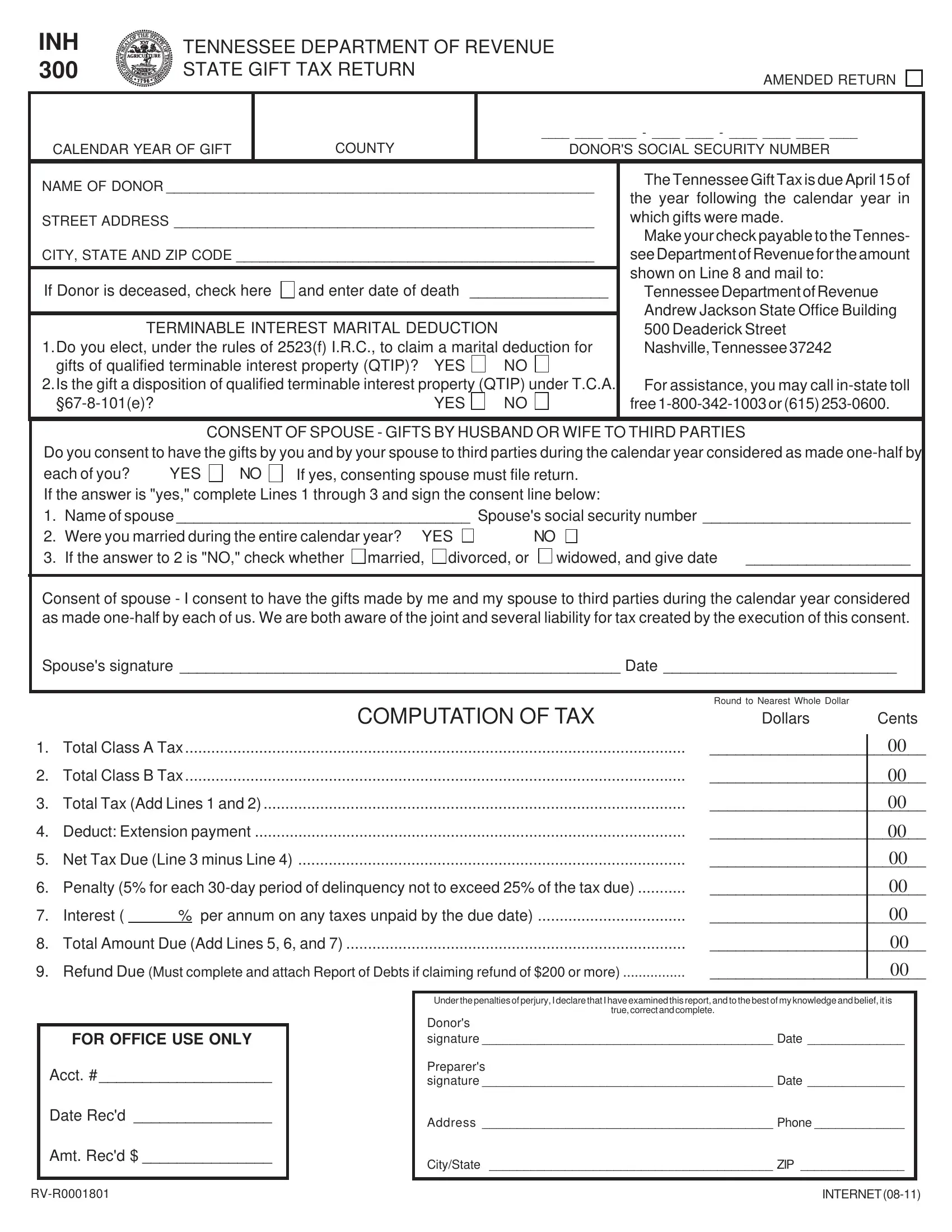

1. Start filling out your Tennessee Form Inh 300 with a selection of major blank fields. Get all of the required information and make sure nothing is left out!

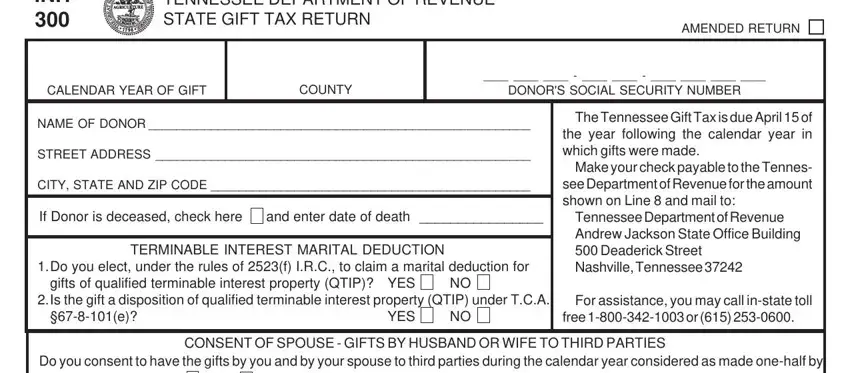

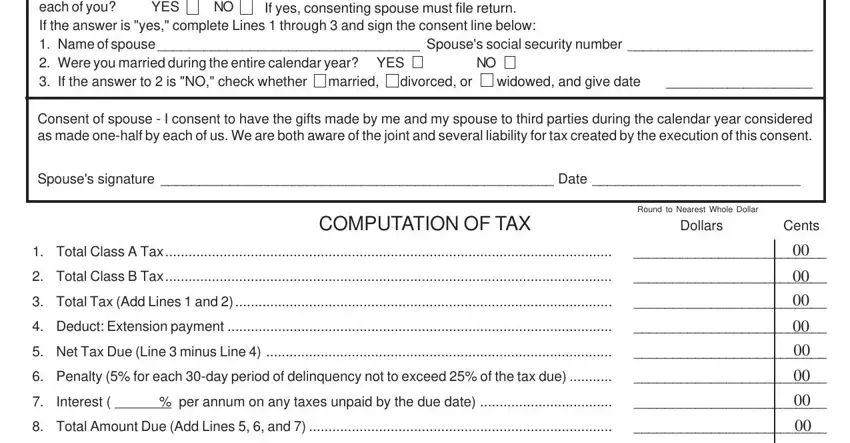

2. When this selection of blank fields is filled out, go on to enter the suitable details in all these: Do you consent to have the gifts, If yes consenting spouse must file, YES, Consent of spouse I consent to, Spouses signature Date, COMPUTATION OF TAX, Round to Nearest Whole Dollar, Dollars, Cents, Total Class A Tax, Total Class B Tax, Total Tax Add Lines and, Deduct Extension payment, Net Tax Due Line minus Line, and Penalty for each day period of.

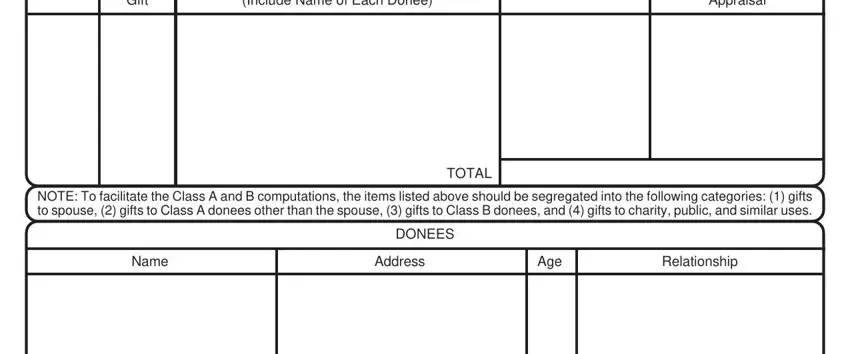

3. This next step is considered rather straightforward, Gift, Include Name of Each Donee, Appraisal, NOTE To facilitate the Class A and, Name, Address, Age, Relationship, DONEES, and TOTAL - every one of these fields is required to be filled out here.

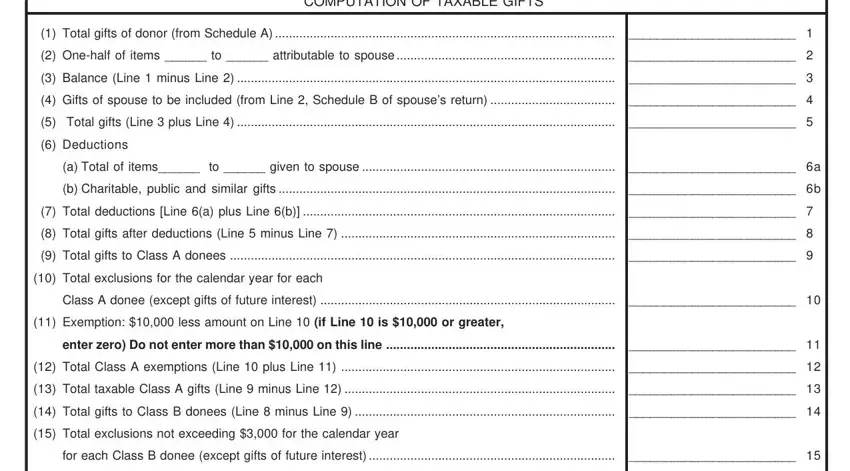

4. The subsequent part needs your involvement in the following areas: COMPUTATION OF TAXABLE GIFTS, Total gifts of donor from, Onehalf of items to, Balance Line minus Line, Gifts of spouse to be included, Total gifts Line plus Line, Deductions, a Total of items to given to, b Charitable public and similar, Total deductions Line a plus Line, Total gifts after deductions Line, Total gifts to Class A donees, Total exclusions for the calendar, Class A donee except gifts of, and Exemption less amount on Line. Make sure that you fill out all needed details to move further.

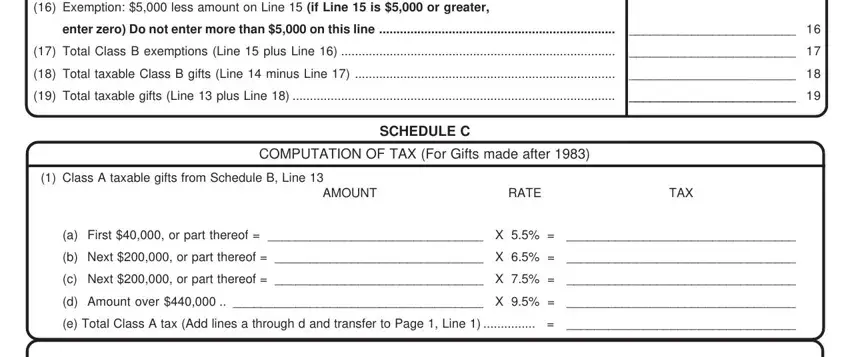

5. The form has to be finished with this segment. Here you have a comprehensive listing of form fields that have to be filled out with appropriate information to allow your document submission to be accomplished: Exemption less amount on Line, enter zero Do not enter more than, Total Class B exemptions Line, Total taxable Class B gifts Line, Total taxable gifts Line plus, SCHEDULE C, COMPUTATION OF TAX For Gifts made, Class A taxable gifts from, AMOUNT, RATE, TAX, a First or part thereof X, b Next or part thereof X, c Next or part thereof X, and d Amount over X.

It is easy to get it wrong while filling out the SCHEDULE C, hence make sure to go through it again prior to when you submit it.

Step 3: Before addressing the next step, it's a good idea to ensure that blank fields are filled out correctly. Once you verify that it's good, press “Done." Try a free trial option at FormsPal and get direct access to Tennessee Form Inh 300 - with all transformations kept and accessible inside your FormsPal cabinet. At FormsPal.com, we do everything we can to be sure that all your details are stored secure.