Our PDF editor works to make filling out files convenient. It is rather not hard to edit the [FORMNAME] document. Consider these particular actions to be able to accomplish this:

Step 1: The initial step is to choose the orange "Get Form Now" button.

Step 2: Once you've got entered the editing page 01 924, you should be able to see all the actions available for your document inside the top menu.

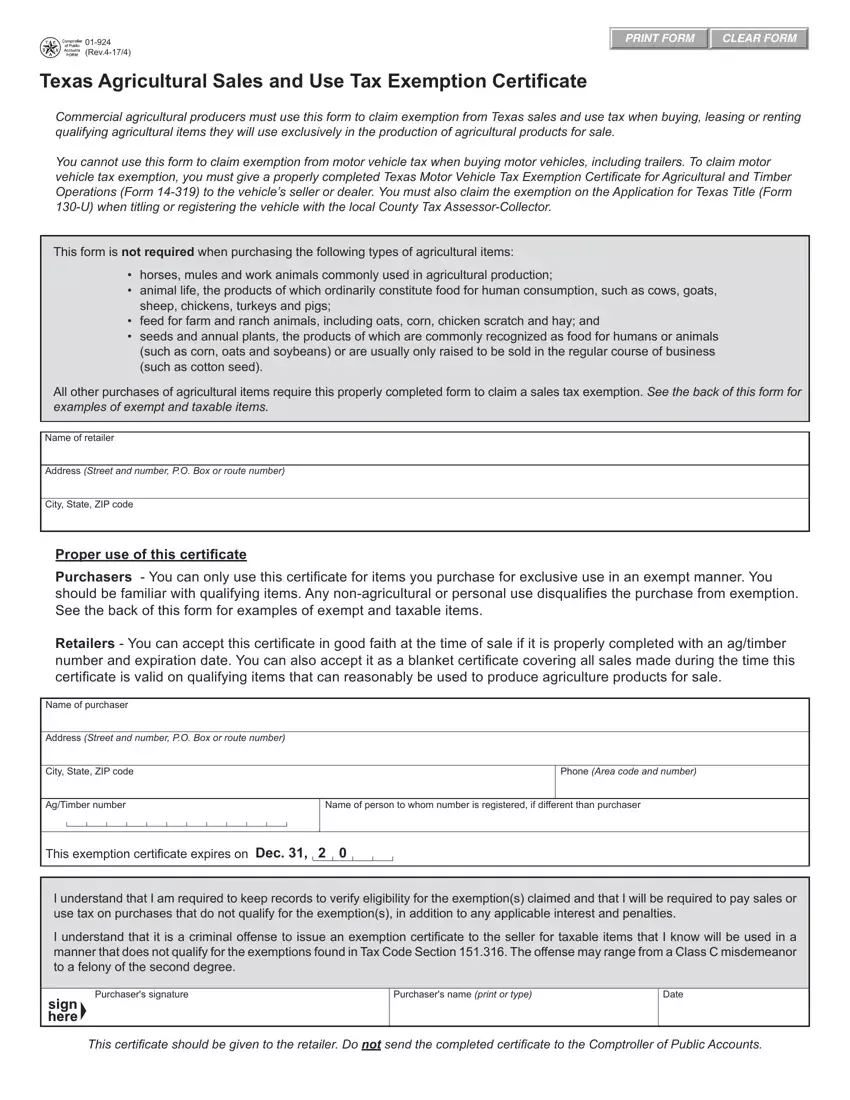

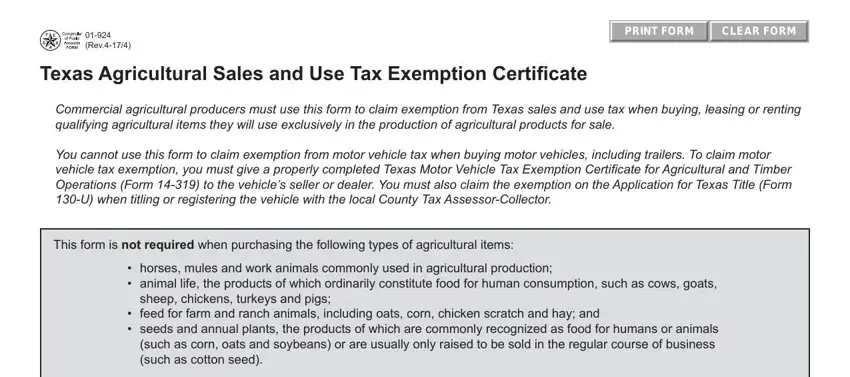

You'll need to provide the following details so you can fill in the document:

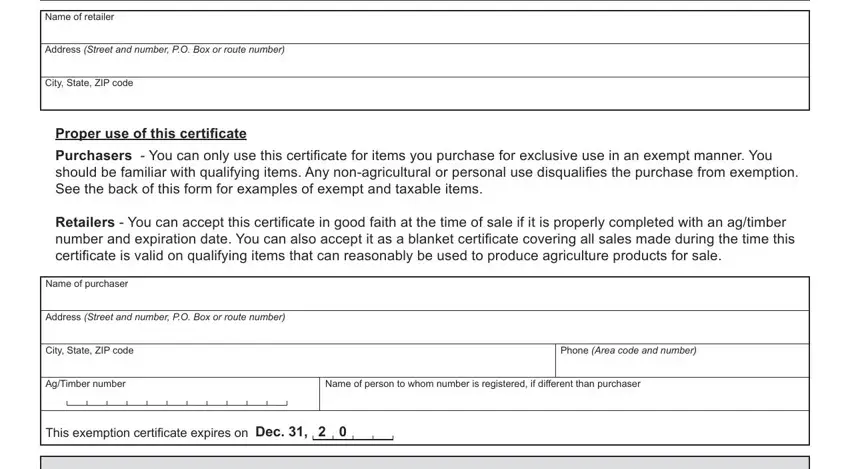

Enter the required details in the area Name of retailer, Address Street and number PO Box, City State ZIP code, Proper use of this certificate, Purchasers You can only use this, Retailers You can accept this, Name of purchaser, Address Street and number PO Box, City State ZIP code, Phone Area code and number, AgTimber number, Name of person to whom number is, and This exemption certificate expires.

Mention the important information in Purchasers signature, Purchasers name print or type, Date, and This certificate should be given section.

The Guns ammunition traps and similar, See, and Tax Help section is the place where either side can indicate their rights and responsibilities.

Step 3: Choose the Done button to ensure that your finalized file could be exported to any gadget you decide on or sent to an email you indicate.

Step 4: It is safer to keep copies of your form. You can be sure that we are not going to share or view your particulars.