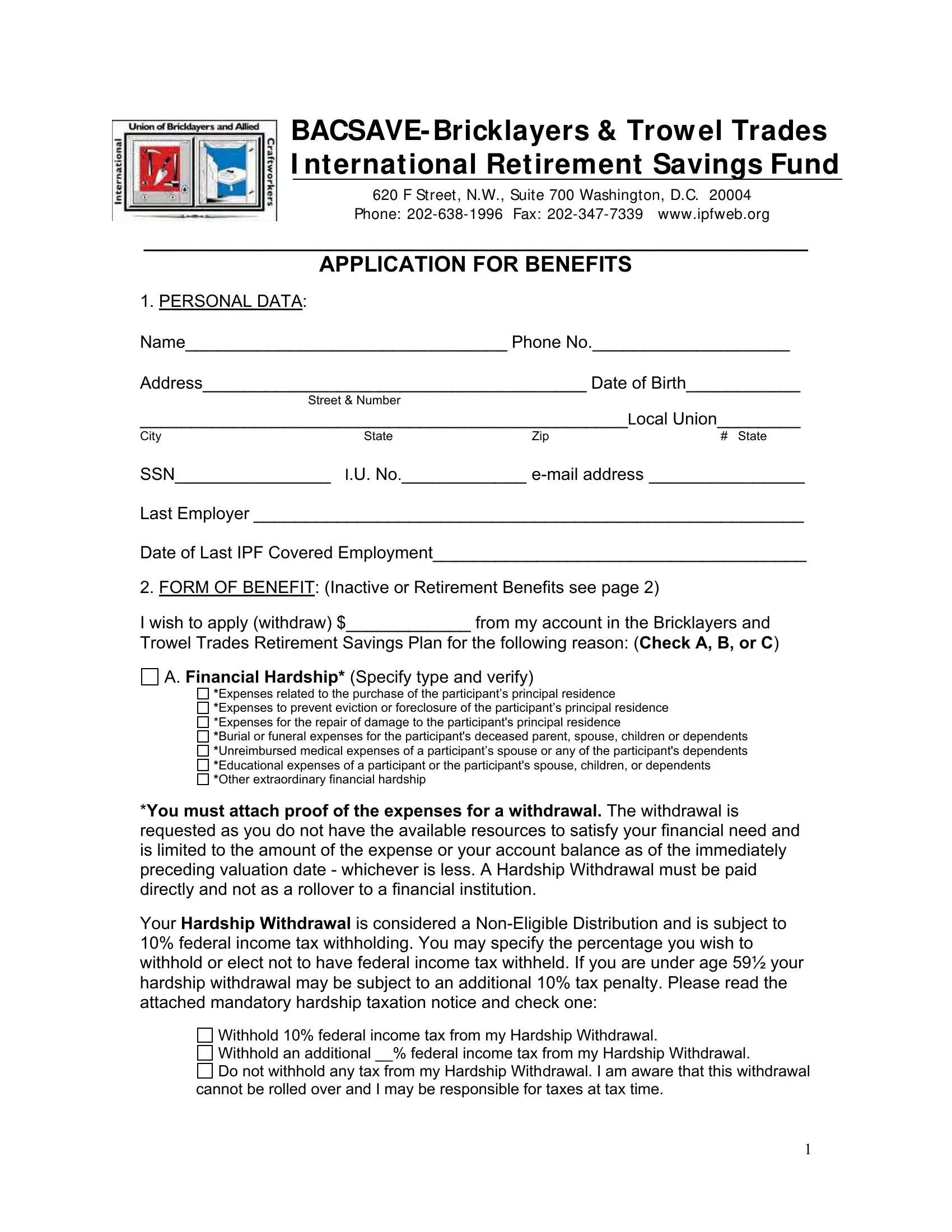

The world of retirement savings is complex, featuring various forms and procedures that can make navigating retirement benefits a daunting task. At the heart of these complexities for bricklayers and trowel trade professionals stands the Trowel International form, formally recognized as the BACSAVE- Bricklayers & Trowel Trades International Retirement Savings Fund Application for Benefits. Located in Washington, D.C., this fund provides a crucial structure for those in the masonry field to secure their financial future post-retirement. The application process itself touches on several key aspects, including personal data submission, benefit selection options ranging from hardship withdrawals to retirement payouts, and the critical element of taxation how it applies to different distributions. Additionally, it acknowledges the importance of beneficiary designation, marital status verification, and the potential need for notarization across various sections, ensuring that the applicant's intentions for benefit disbursement are clearly understood and adhered to. The process also delineates between types of withdrawals, from lump sums to annuities, and the protocols for each, depending on the applicant's marital status, offering guidance on navigating through common law marriage claims or the aftermath of spousal loss. This rigor ensures that every participant's benefits are tailor-made to their life situation, providing a secure and reliable foundation for post-career life.

| Question | Answer |

|---|---|

| Form Name | Trowel International Form |

| Form Length | 10 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 2 min 30 sec |

| Other names | bricklayers trowel international, bricklayers trades international, bricklayers trades fund, trades international application |