We've applied the hard work of our best programmers to develop the PDF editor you are about to use. The software allows you to prepare the usda credit waiver form easily and don’t waste time. All you should undertake is try out the following straightforward rules.

Step 1: Click the orange button "Get Form Here" on the web page.

Step 2: Now you are free to edit usda credit waiver. You possess a lot of options with our multifunctional toolbar - you'll be able to add, delete, or alter the text, highlight the specific components, and perform several other commands.

Type in the essential data in each one segment to complete the PDF usda credit waiver

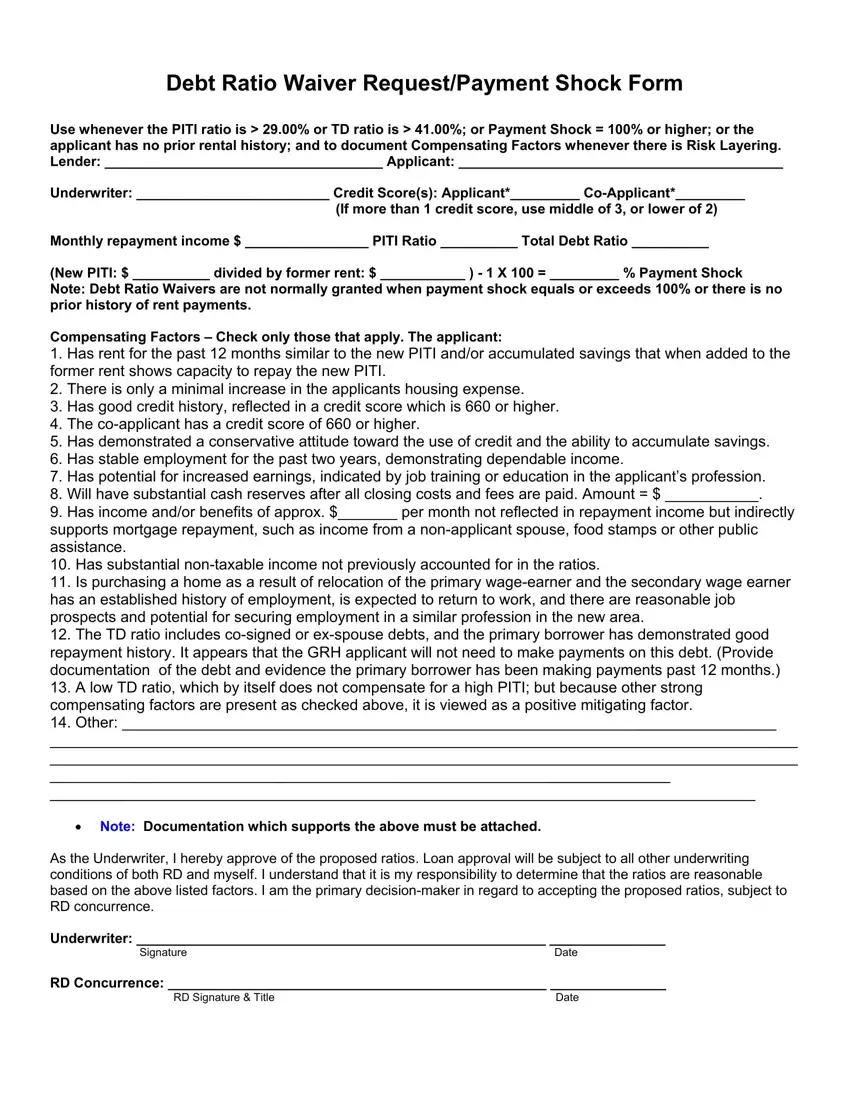

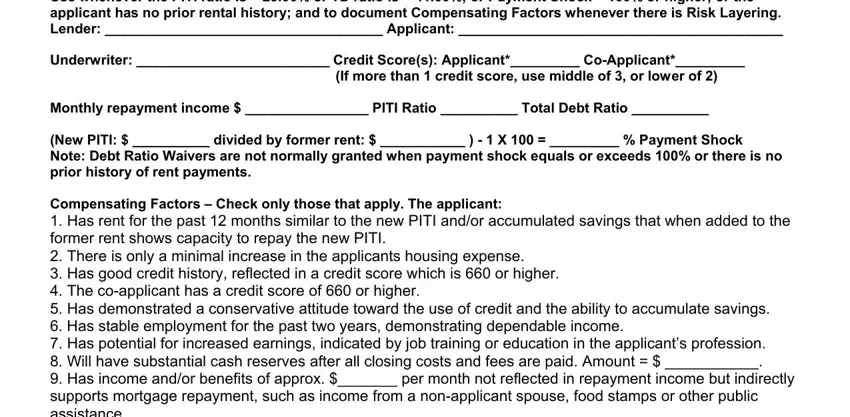

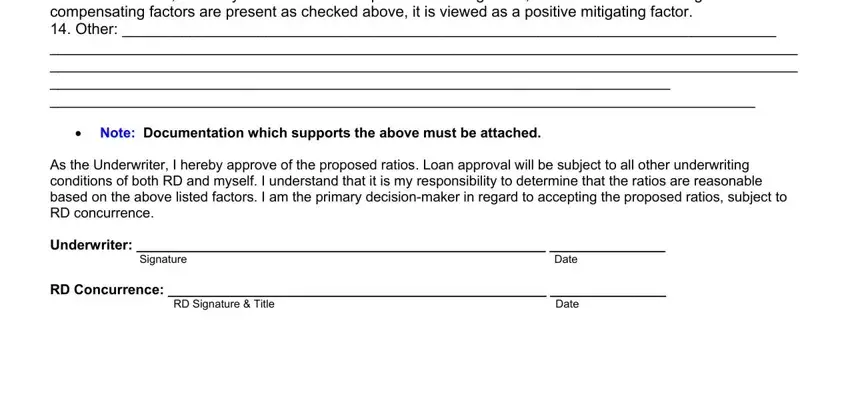

Write the requested data in the Compensating Factors Check only, Note Documentation which supports, As the Underwriter I hereby, Underwriter Signature Date, and RD Concurrence RD Signature box.

Step 3: Press the "Done" button. Now it's easy to upload your PDF form to your device. In addition, you'll be able to send it via electronic mail.

Step 4: You can generate duplicates of the form tokeep clear of any type of potential future difficulties. Don't be concerned, we do not distribute or monitor your data.