In the comprehensive realm of global insurance, the Zurich Insurance Company Group stands as a paragon, elucidating its operational and financial dynamics through its Annual Report for 2020. This document, a rich tapestry of intricate details, spans from a meticulous risk review to a thorough financial scrutiny, underscoring the conglomerate's commitment to transparency and robust risk management. Serving a diverse clientele that includes individuals, small businesses, and multinational corporations across more than 215 countries and territories, Zurich highlights its foundational strengths and strategic foresight. Established in 1872 in Zurich, Switzerland, the Group not only pledges an unparalleled range of property and casualty, and life insurance products but also showcases a steadfast dedication to risk management principles that are designed to bolster its financial resilience and strategic objectives. The risk review section, an integral component of the consolidated financial statements, lays bare the framework and objectives guiding Zurich’s risk management and capital allocation - from ensuring adherence to a pre-determined risk appetite to enhancing value creation through disciplined risk-taking. Moreover, the financial review offers a panoramic view of the Group's financial health, featuring consolidated financial statements and a breakdown of its statutory accounts. The laudable endeavor to balance risk and reward, safeguard liquidity and earnings, and protect its venerable reputation, positions the Zurich Insurance Company Group as a luminary in the global insurance landscape.

| Question | Answer |

|---|---|

| Form Name | Zurich Insurance |

| Form Length | 178 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 22 min 15 sec |

| Other names | zurich gap insurance, zurich cancellation, zurich extended warranty cancellation, zurich warranty refund |

Zurich Insurance Company Group

Annual Report 2020

Zurich Insurance Company Group

Annual Report 2020

Contents

Risk review |

2 |

|

|

Financial review |

24 |

|

|

Financial overview |

24 |

|

|

Consolidated financial statements |

32 |

|

|

Financial statements – |

|

statutory accounts |

146 |

|

|

Zurich Insurance Company Group |

1 |

|

Annual Report 2020 |

||

|

||

|

|

About us

Zurich Insurance Group (Zurich) is

a leading

in 1872. The holding company, Zurich Insurance Group Ltd (ZURN), is listed on the SIX Swiss Exchange and has a level I American Depositary Receipt (ZURVY) program, which is traded

Zurich Insurance Company Group |

2 |

|

Annual Report 2020 |

||

|

||

|

|

Risk review

Contents

Risk management |

3 |

|

|

Objectives of risk management |

3 |

|

|

Risk management framework |

3 |

|

|

Risk governance and risk |

|

management organization |

5 |

|

|

Capital management |

6 |

|

|

Objectives of capital management |

6 |

|

|

Capital management framework |

6 |

|

|

Capital management program |

6 |

|

|

Insurance financial strength rating |

7 |

|

|

Regulatory capital adequacy |

7 |

|

|

Regulatory solvency regimes |

7 |

|

|

Analysis by risk type |

8 |

|

|

Insurance risk |

8 |

|

|

Market risk, including investment credit risk |

15 |

|

|

Other credit risk |

19 |

|

|

Liquidity risk |

21 |

|

|

Strategic risk and risks to the |

|

Zurich Insurance Group’s reputation |

22 |

|

|

Zurich Insurance Company Group |

3 |

|

Annual Report 2020 |

||

|

||

|

|

Risk review (continued)

Basis of presentation

The risk review is an integral part of the consolidated financial statements.

Risk and capital are managed at the Zurich Insurance Group, segment, region and business unit level according to the Zurich Insurance Group risk and capital management framework. The principles of the Zurich Insurance Group enterprise risk management described in the risk management and capital management sections are equally applicable to Zurich Insurance Company Ltd (ZIC) and its consolidated subsidiaries (collectively the ZIC Group).

The Zurich Insurance Group Ltd Board of Directors, Chief Executive Officer, and Chief Risk Officer equally serve as Board of Directors, Chief Executive Officer, and Chief Risk Officer for Zurich Insurance Company Ltd.

The figures presented are prepared on a ZIC Group basis.

Risk management

Objectives of risk management

Taking and managing risk is an integral part of the insurance business. Zurich Insurance Group takes and manages risks in an informed and disciplined manner and within a

The major risk management objectives at Zurich Insurance Group are to:

––Support achievement of the Zurich Insurance Group strategy and protect capital, liquidity, earnings and reputation by monitoring that risks are taken within Zurich Insurance Group’s risk tolerance

––Enhance value creation by embedding disciplined

––Efficiently and effectively diversify risk and avoid or mitigate unrewarded risks

––Encourage openness and transparency to enable effective risk management

––Support

––Protect Zurich Insurance Group’s reputation and brand by promoting a sound culture of risk awareness, and disciplined and informed

Risk management framework

The risk management framework is based on a governance process that sets forth clear responsibilities for taking, managing, monitoring and reporting risks.

The Zurich Risk Policy (ZRP) is Zurich Insurance Group’s main risk governance document. It sets standards for effective risk management throughout Zurich Insurance Group. The policy describes Zurich Insurance Group’s risk management framework, provides a standardized set of risk types and defines Zurich Insurance Group’s appetite for risks at Zurich Insurance Group level.

Zurich Insurance Group regularly reports on its risk profile at local and Zurich Insurance Group levels. Zurich Insurance Group has procedures to refer risk topics to senior management and the Board of Directors in a timely manner. To foster transparency about risk, the Board receives quarterly risk reports and risk updates. In 2020, additional dynamic reporting of

Zurich Insurance Group identifies, assesses, manages, monitors and reports risks that have an impact on the achievement of its strategic objectives by applying its proprietary Total Risk Profiling™ methodology. The methodology allows Zurich Insurance Group to assess risks in terms of severity and probability and supports the definition and implementation of mitigating actions. At Zurich Insurance Group level, this is an annual process, followed by regular reviews and updates by management.

Zurich Insurance Company Group |

4 |

|

Annual Report 2020 |

||

|

||

|

|

Risk review (continued)

Zurich Insurance Group’s risk appetite and tolerance reflects Zurich Insurance Group’s willingness and capacity to take risks in pursuit of value creation and sets boundaries within which the businesses act. Zurich Insurance Group protects its capital, liquidity, earnings and reputation by monitoring that risks are taken within agreed risk appetite levels and tolerance limits. Zurich Insurance Group regularly assesses and, to the extent possible, quantifies material risks to which it is exposed.

Starting as of 2020, Zurich Insurance Group’s solvency position will be disclosed on the basis of the Swiss Solvency Test (SST) ratio to be more aligned with reporting by Zurich Insurance Group’s Swiss and European peers. The Zurich Insurance Group’s SST internal model has been fully approved by the Swiss Financial Supervisory Authority (FINMA). Zurich Insurance Group’s goal is to maintain capital consistent with a ‘AA’ financial strength rating for the Zurich Insurance Group, which translates into an SST ratio target of 160 percent or above.

Zurich Insurance Group continues to apply the Zurich Economic Capital Model

Based on Zurich Insurance Group’s remuneration rules, the Board of Directors designs and structures remuneration arrangements that support the achievement of strategic and financial objectives and do not encourage inappropriate

Zurich Insurance Company Group |

5 |

|

Annual Report 2020 |

||

|

||

|

|

Risk review (continued)

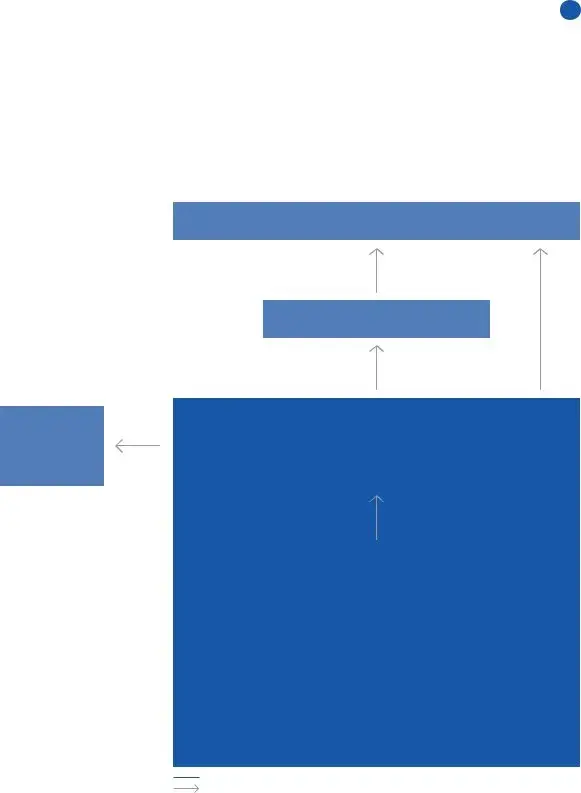

Risk governance and risk management organization

Risk management organization

The Group Risk Management function is a global function, led by Zurich Insurance Group’s Chief Risk Officer (CRO).

Executive

management committees

Risk and Investment Committee of the Board

Group Chief Executive Officer

Group Chief Risk Officer

Leads the Group Risk Management function, which develops frameworks and

methodologies for identifying, assessing, measuring, managing and reporting risks throughout the Group. The Group CRO has direct access to the Board of Directors.

Group level |

|

Region and business unit level |

|

|

|

Staff at Group level focus |

|

Regional and business heads of risk |

on risk management |

|

Business unit chief risk officers |

frameworks, risk |

|

Each country has a dedicated risk management |

governance, risk reporting, |

|

|

|

team located with the local management team |

|

methodologies and tools, |

|

|

|

for effective business partnering activities, serving |

|

and qualitative and |

|

|

|

both management and legal entity view. |

|

quantitative assessments. |

|

|

|

|

|

They quantify the Group’s |

|

|

risk and economic capital |

|

|

position and monitor |

|

|

adherence to risk tolerance. |

|

|

They quantitatively assess |

|

|

insurance, market, |

|

|

credit and operational |

|

|

risk, and focus |

|

|

on model validation. |

|

|

Risk function |

The Group has committees covering oversight activities that |

Reporting about risks |

encompass major business areas. The committees review certain |

|

risk management matters for their respective areas. At the local |

|

level, these oversight activities are conducted through risk and |

|

control committees. |

The risk function is independent of the business by being a vertically integrated function where, unless otherwise required by local laws or regulations, global risk employees report directly into the Zurich Insurance Group CRO, except for Farmers’ Chief Risk Officer who has a matrix reporting line to Zurich Insurance Group’s CRO. Risk officers are embedded in the business, positioning them to support and advise on, and independently challenge, business decisions from a risk perspective. As business advisers on risk matters, the risk officers, equipped with technical risk skills as well as business skills, help foster a

Zurich Insurance Company Group |

6 |

|

Annual Report 2020 |

||

|

||

|

|

Risk review (continued)

Capital management

Objectives of capital management

Zurich Insurance Group manages capital to maximize

As of December 31, 2020, the International Financial Reporting Standards (IFRS) for Zurich Insurance Company Group (ZIC Group) shareholders’ equity amounted to USD 37.5 billion and subordinated debt of USD 8.3 billion.

ZIC Group strives to simplify its legal entity structure to reduce complexity and increase fungibility of capital.

Capital management framework

Zurich Insurance Group’s capital management framework forms the basis for actively managing capital within Zurich Insurance Group. Zurich Insurance Group uses a number of different capital models, taking into account economic, regulatory, and rating agency constraints. Zurich Insurance Group’s capital and solvency position is monitored and regularly reported to the Executive Committee (ExCo) and Board of Directors.

Zurich Insurance Group’s policy is to allocate capital to businesses earning the highest

Zurich Insurance Group’s executive management determines the capital management strategy and sets the principles, standards and policies to execute the strategy. Group Treasury and Capital Management executes the strategy.

Capital management program

Zurich Insurance Group’s capital management program comprises various actions to optimize shareholders’ total return and to meet capital needs, while enabling Zurich Insurance Group to take advantage of growth opportunities. Such actions include paying and receiving dividends, capital repayments, share

Zurich Insurance Group seeks to maintain a balance between higher returns for shareholders on equity held and the security that a sound capital position provides, also for our customers. Dividends, share

The Swiss Code of Obligations stipulates that dividends may only be paid out of freely distributable reserves or retained earnings. Apart from what is specified by the Swiss Code of Obligations, Zurich Insurance Company Ltd (ZIC) faces no legal restrictions on dividends it may pay to its shareholders. As of December 31, 2020, the amount of the statutory general legal reserve was more than 40 times the

For details on issuances and redemptions of debt, see note 18 of the ZIC Group consolidated financial statements.

Zurich Insurance Company Group |

7 |

|

Annual Report 2020 |

||

|

||

|

|

Risk review (continued)

Insurance financial strength rating

Zurich Insurance Group has interactive relationships with three global rating agencies: S&P Global Ratings, Moody’s, and AM Best. The insurance financial strength rating (IFSR) of Zurich Insurance Group’s main operating entity, Zurich Insurance Company Ltd, is an important element of Zurich Insurance Group’s competitive position, while Zurich Insurance Group’s credit ratings also affect the cost of debt capital.

The insurance financial strength ratings remained unchanged in 2020 despite the impact of

The planned acquisition by Zurich Insurance Group’s subsidiary Farmers Group, Inc (FGI) and Farmers Exchanges of the U.S. Property & Casualty division of MetLife and its financing was seen as a credit positive for Zurich Insurance Group by Moody’s and further supported Zurich Insurance Group’s positive outlook by S&P. The agencies consider that the acquisition will increase the contribution of Farmers Management fees to the profits, while Zurich Insurance Group maintains a strong capitalization and high financial flexibility.

As of December 31, 2020, the IFSR of Zurich Insurance Company Ltd, the main operating entity of Zurich Insurance Group, was

Regulatory capital adequacy

Zurich Insurance Group endeavors to manage its capital so that its regulated entities meet local regulatory capital requirements. In each country in which Zurich Insurance Group operates, the local regulator specifies the minimum amount and type of capital that each of the regulated entities must hold in addition to their liabilities. In addition to the minimum capital required to comply with the solvency requirements, Zurich Insurance Group aims to hold an adequate buffer under local solvency requirements to ensure regulated subsidiaries can absorb a level of volatility and meet local capital requirements.

Regulatory solvency regimes

Regulatory requirements in Switzerland

The Swiss Solvency Test (SST) adopts a

Under SST, insurance companies and insurance groups can apply to use

Regulatory requirements in the European Economic Area (EEA)

The main regulatory framework governing Zurich Insurance Group’s subsidiaries in the EEA is Solvency II. This is

a

Regulatory requirements in the UK

The United Kingdom left the EU and the EEA on January 31, 2020 and the transition period ended on December 31, 2020, meaning that UK regulations can diverge from Solvency II regulatory requirements.

Regulatory requirements in the U.S.

In the U.S., required capital is determined to be ‘company action level

Regulatory requirements in other jurisdictions

Every country has a capital standard for insurance companies. Several jurisdictions (e.g., Brazil and Mexico) have implemented approaches similar to Solvency II.

Zurich Insurance Company Group |

8 |

|

Annual Report 2020 |

||

|

||

|

|

Risk review (continued)

Analysis by risk type

Insurance risk

Insurance risk is the inherent uncertainty regarding the occurrence, amount or timing of insurance cash flows. The profitability of insurance business is also susceptible to business risk in the form of unexpected changes in expenses, policyholders’ behavior, and fluctuations in new business volumes. Zurich Insurance Group manages insurance risk through:

––Specific underwriting and claims standards and controls

––Robust reserving processes

––External reinsurance

Property and casualty insurance risk

Property and casualty insurance risk arises from coverage provided for motor, property, liability, special lines and worker injury. It comprises premium and reserve risk, catastrophe risk, and business risk. Premium and reserve risk covers uncertainties in the frequency of the occurrence of the insured events as well as in the severity of the resulting claims. Catastrophe risk predominantly relates to uncertainty around natural catastrophes. Business risk for property and casualty predominantly relates to unexpected increases in the expenses relating to claims handling, underwriting, and administration.

Management of Property & Casualty business insurance risk

Zurich Insurance Group’s underwriting strategy takes advantage of the diversification of Property & Casualty (P&C) risks across lines of business, customers and geographic regions. Zurich Insurance Group defines

Property & Casualty insurance reserves are regularly estimated, reviewed and monitored by qualified and experienced actuaries at local, regional and Zurich Insurance Group levels. To arrive at their reserve estimates, the actuaries take into consideration, among other things, the latest available facts, trends and patterns of loss payments. Inflation is monitored with insights feeding into actuarial reserving models and Zurich Insurance Group’s underwriting processes and pricing.

To ensure a common understanding of business insights and new trends for reserve analysis, financial plans, underwriting and pricing decisions, Zurich Insurance Group has established a culture of continuous

Zurich Insurance Group’s Emerging Risk Committee, with

Governance is in place to ensure appropriate focus on

Zurich Insurance Group is exposed to losses that could arise from natural and