If one possesses an enterprise of any kind in the United States (regardless of the sphere), they are aware of the necessity of financial results reporting. We all count our money, whether what we review is our personal savings or the budget of the company we manage. To make the accountants’ and managers’ lives easier, special templates exist. By filling them out, one may easily understand how things go right now in the reviewed entity.

While being an irreplaceable template, a profit and loss statement (many people identify it as an “income statement”) helps gather specific ratios and figures for further analysis. The majority of businesses and entities in the United States, regardless of their size, utilize these records to define the current financial situation, how much they have received and forfeited, and their results of a specific time frame.

There are two other templates vital for accounting: a balance sheet and cash flow statement. These papers serve different purposes, but they are also needed to make plans and create forecasts related to businesses and their future actions.

Like any other legal documents, the profit and loss statement has its unique structure, requirements, and details to include. We will review the template completion and describe the items you should use there in this article, so one who has questions can understand all peculiarities about this paper.

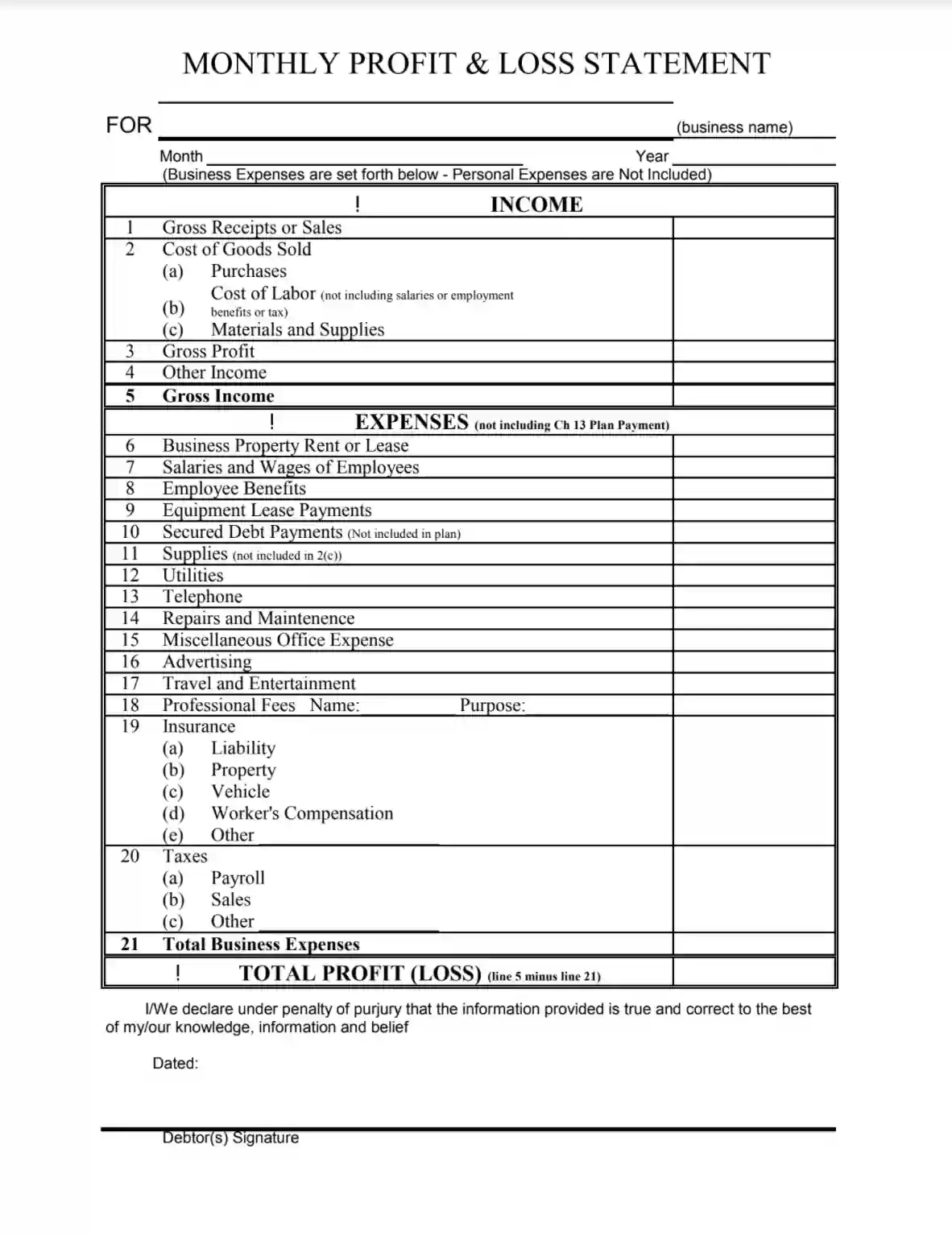

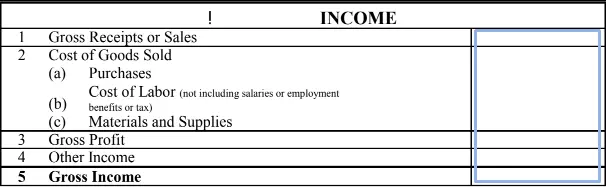

One can define it as a document that lists all the entity’s income and spending over a specific period. The aim of completion here is to recognize how much your firm has gained and spent. After enumerating all positions, a net income (or net loss) can be counted. While reading the statement, one sees the contrast between the present and the past activity. You can easily analyze the company’s performance with this template.

The document looks like a chart where you insert numbers. Some people prefer completing the profit and loss statement in Excel; others stay with traditional handwriting or other software tools. We recommend using our templates building software to create a profit and loss statement from scratch.

All business owners are usually bothered by the profit and loss statements, cash flow statements, and balance sheet creation. In the majority of entities, an accountant (or several accountants) is hired to generate such papers in a required period. Small businesses sometimes cannot afford to hire an accountant, so the managers should create such records by themselves.

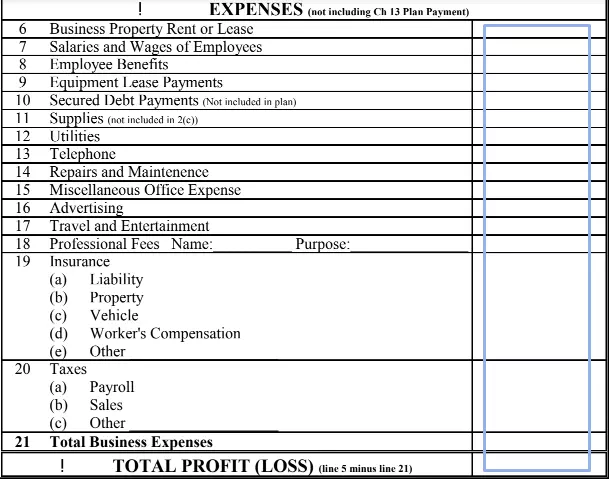

Apart from the company name and the period for which the statement is written, you should prepare various financial details: results of sales and deals, revenues your firm has gained from other sources, operating expenses, paid utility bills, and all other data tied to the money spent and received during the stated time.

These details will be split into two categories: revenue and expenses of your business. Under the income, you will include the cost of goods sold, sales, and other income. Many types of expenses will go under the “expenses” section: you have to gather all of them, so this financial document is properly made.

It is vital to add the author’s name and signature after the work is done.

Other Financial Forms

Do you require other financial forms? Check out the list following next to see what you can fill in and edit with FormsPal. Also, keep in mind that it is easy to upload, fill out, and edit any PDF form at FormsPal.

We have touched on this topic in the previous section; now, let’s see in detail how to create such a record step by step. We will use the monthly profit and loss template. However, the info you add for another time frame template will stay the same.

1) Download the Template

Our form-building software will assist in getting and completing the proper profit and loss statement template.

2) Insert the Business Name

Below the heading, insert the entity’s name for which this profit and loss template is generated.

3) State the Time Frame

Below the business name, insert the time frame for which the profit and loss template is completed. Use the “year” and “month” lines.

4) Count the Income

The first thing you write in the chart is information about the income, including:

After you list everything, you can count the net income for the stated period.

5) Describe the Expenses

Then, state all the costs of your entity during the chosen time frame:

And other happened expenses. You may check the full list below — it consists of 15 positions that describe various types of spendings.

6) Define the Net Income (or Loss)

After you include all the expenses, you can count the total amount and understand your net income or loss. The net income is your total income minus your total expenses. If you get a negative number, it is considered a net loss of your firm, often written in brackets.

7) Confirm that the Added Data Is True

After you have inserted everything in the template and counted the net profit (or loss), double-check the calculation. All numbers should be correct; otherwise, you might be accused of fraud, and penalties would follow.

Giving incorrect or untrue data in such statements is considered unlawful because some business representatives and owners might try to skip paying as much taxes as they should.

8) Sign the Profit and Loss Statement

When every section is filled out, the document’s creator should introduce themselves and sign the paper. Remember to add the date of signing above the signature.

Usually, people who run firms create such statements once in a particular period: a month, quarter, or year. It depends on your needs. Whether you complete the template once per year or month, it will help you keep track of the company results, plan the actions, and react to significant losses.

We have reviewed the monthly statement completion: a convenient tool that lets you improve the performance and avoid financial problems. However, regardless of the time frame, the structure and data you provide in the profit and loss template remain the same.

The goals and structure of these records vary. With cash flow statements, one may define how much money has gone in and out of the corporate accounts during the reviewed term. Balance sheets list all assets and liabilities that the firm currently has.