Engaging with a 403B Request form is a critical process for individuals looking to withdraw funds from their tax-sheltered annuity plans, often utilized by non-profit employees, teachers, and certain ministers. The form, provided by insurance giants like the Metropolitan Life Insurance Company and its affiliates, is comprehensive, covering various aspects from personal information to the specific reasons for the withdrawal. Reasons for withdrawal can range widely – from reaching the age of 59 1/2, experiencing a disability, severance from employment, to retirement, among others. The form also guides participants through selecting the amount and source of withdrawal, including the intricate details regarding loan payoffs, payment instructions, and federal and state tax withholding notices. A significant emphasis is placed on ensuring participants understand the potential tax implications and penalties, especially for those under the age of 59 1/2, who might face a 10% federal income tax penalty along with any applicable withdrawal charges. Detailed instructions are provided for circumstances requiring additional documentation, such as physician's confirmation for disability withdrawals or employer authorization for severance-based requests. The form also addresses direct transfers or rollovers to other retirement accounts, highlighting compliance with recent regulatory changes to maintain the tax-deferred status of the account. Towards the end, the form explores the options regarding annuity information, waivers, and spousal consent, adding layers of complexity that underscore the importance of thoroughly understanding the 403B withdrawal request process and the potential consequences across various scenarios.

| Question | Answer |

|---|---|

| Form Name | 403B Request Form |

| Form Length | 12 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 3 min |

| Other names | what is fsk modulation, metlife 403b terms of withdrawal, metlife 403b withdrawal request form, metlife erisa 403 b withdrawal request form |

Metropolitan Life Insurance Company

MetLife Investors USA Insurance Company

MetLife Insurance Company of Connecticut

403(b) Withdrawal Request Form

Because 403(b) withdrawal rules are complex, please read Instructions and Special Tax Notice Regarding TSA Payments before completing this form. If you are under 59 1/2, your withdrawal may be subject to a 10% federal income tax penalty. Your withdrawal may also incur withdrawal charges.

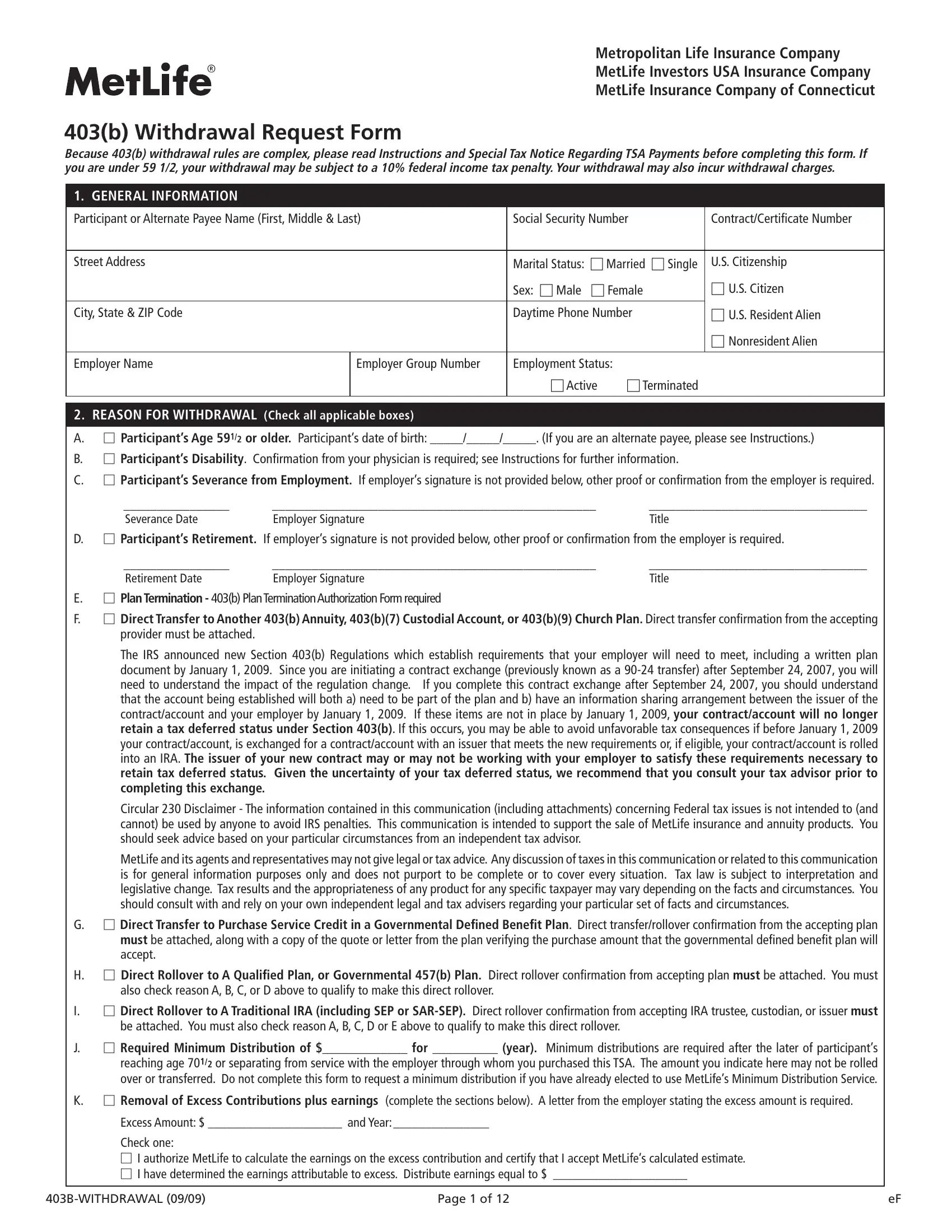

1. GENERAL INFORMATION

Participant or Alternate Payee Name (First, Middle & Last) |

Social Security Number |

Contract/Certiicate Number |

|||

|

|

|

|

||

Street Address |

|

Marital Status: Married Single |

U.S. Citizenship |

||

|

|

Sex: Male Female |

U.S. Citizen |

||

|

|

|

|||

City, State & ZIP Code |

|

Daytime Phone Number |

U.S. Resident Alien |

||

|

|

|

|

|

|

|

|

|

|

|

Nonresident Alien |

|

|

|

|

|

|

Employer Name |

Employer Group Number |

Employment Status: |

|

|

|

|

|

|

Active |

Terminated |

|

2.REASON FOR WITHDRAWAL (Check all applicable boxes)

A. Participant’s Age 591/2 or older. Participant’s date of birth: _____/_____/_____. (If you are an alternate payee, please see Instructions.)

B.Participant’s Disability. Conirmation from your physician is required; see Instructions for further information.

C.Participant’s Severance from Employment. If employer’s signature is not provided below, other proof or conirmation from the employer is required.

________________ |

_________________________________________________ |

_________________________________ |

Severance Date |

Employer Signature |

Title |

D.Participant’s Retirement. If employer’s signature is not provided below, other proof or conirmation from the employer is required.

________________ |

_________________________________________________ |

_________________________________ |

Retirement Date |

Employer Signature |

Title |

E.Plan Termination - 403(b) Plan Termination Authorization Form required

F.Direct Transfer to Another 403(b) Annuity, 403(b)(7) Custodial Account, or 403(b)(9) Church Plan. Direct transfer conirmation from the accepting provider must be attached.

The IRS announced new Section 403(b) Regulations which establish requirements that your employer will need to meet, including a written plan document by January 1, 2009. Since you are initiating a contract exchange (previously known as a

Circular 230 Disclaimer - The information contained in this communication (including attachments) concerning Federal tax issues is not intended to (and cannot) be used by anyone to avoid IRS penalties. This communication is intended to support the sale of MetLife insurance and annuity products. You should seek advice based on your particular circumstances from an independent tax advisor.

MetLife and its agents and representatives may not give legal or tax advice. Any discussion of taxes in this communication or related to this communication is for general information purposes only and does not purport to be complete or to cover every situation. Tax law is subject to interpretation and legislative change. Tax results and the appropriateness of any product for any speciic taxpayer may vary depending on the facts and circumstances. You should consult with and rely on your own independent legal and tax advisers regarding your particular set of facts and circumstances.

G.Direct Transfer to Purchase Service Credit in a Governmental Deined Beneit Plan. Direct transfer/rollover conirmation from the accepting plan must be attached, along with a copy of the quote or letter from the plan verifying the purchase amount that the governmental deined beneit plan will accept.

H.Direct Rollover to A Qualiied Plan, or Governmental 457(b) Plan. Direct rollover conirmation from accepting plan must be attached. You must also check reason A, B, C, or D above to qualify to make this direct rollover.

I.Direct Rollover to A Traditional IRA (including SEP or

J.Required Minimum Distribution of $_____________ for __________ (year). Minimum distributions are required after the later of participant’s reaching age 701/2 or separating from service with the employer through whom you purchased this TSA. The amount you indicate here may not be rolled over or transferred. Do not complete this form to request a minimum distribution if you have already elected to use MetLife’s Minimum Distribution Service.

K.Removal of Excess Contributions plus earnings (complete the sections below). A letter from the employer stating the excess amount is required.

Excess Amount: $ _____________________ and Year: _______________ |

|

|

Check one: |

|

|

I authorize MetLife to calculate the earnings on the excess contribution and certify that I accept MetLife’s calculated estimate. |

||

I have determined the earnings attributable to excess. Distribute earnings equal to $ |

_____________________ |

|

Page 1 of 12 |

eF |

|

Contract/Certiicate Number:

3. AMOUNT AND SOURCE OF WITHDRAWAL

A.I wish to withdraw my entire Account Balance.

•If you currently contribute to your contract through payroll deductions, you must contact your payroll department to stop contributions to your contract. If contributions are received after a full surrender is taken, they will be sent back to the employer.

•If you have an oustanding loan, it will automatically be closed upon request of a full surrender.

Check here if this is a “systematic termination” request (EPPA or FFA only). B. I wish to withdraw a NET amount of $_______________.

•Only complete items below if you have variable funding option allocations in a variable annuity.

•Distributions will be automatically prorated against all funding and money type options unless you specify otherwise in the section below.

I wish to withdraw the requested amount using the following allocation or money types. (Indicate from which funding options and/or money types we should take this withdrawal. Write percentages in whole number, e.g., 33% not 331/3%.)

|

Percentage or |

Investment Options/Money Type |

Dollar Amount |

_____________________________________________________________________________________ |

______________________ |

_____________________________________________________________________________________ |

______________________ |

_____________________________________________________________________________________ |

______________________ |

_____________________________________________________________________________________ |

______________________ |

_____________________________________________________________________________________ |

______________________ |

_____________________________________________________________________________________ |

______________________ |

TOTAL (100% or $) |

______________________ |

|

4. REQUIRED MINIMUM DISTRIBUTION INSTRUCTIONS FOR ROLLOVERS/TRANSFERS

If you checked withdrawal reason F, G, H or I in section 2 on page 1, and you have been taking minimum distributions from this account, you must take one for this tax year before the account is rolled over.

A. Check here if you are enrolled in MetLife’s Minimum Distribution Service (a check will be automatically sent to you for the required amount).

B.Check here if you are NOT enrolled in MetLife’s Minimum Distribution Service. Please indicate the required minimum distribution amount $________________

(See sections 8 and 9 for important income tax withholding instructions and election options).

5. OUTSTANDING LOAN PAYOFF INFORMATION AND INSTRUCTIONS

A.Attached is a certiied check to pay off my outstanding loan balance. (Use eService or call our customer service number for loan payoff amount.)

B. Treat my outstanding loan (principal and interest) as a distribution. (This option only available after you reach age 591/2 have a severance from employment, or become disabled.) I understand that if my loan is not currently in default, this offset will be reported as a taxable distribution for the year of offset.

C. For partial withdrawals: I have not separated from service and the partial withdrawal amount I have requested does not exceed the amount permitted as a partial withdrawal while I have a loan outstanding. Do not treat my outstanding loan as a taxable distribution. I understand that my loan will remain in force and I must continue to repay it; my account will remain open for crediting of future loan repayments.

Note: If you have an outstanding loan, it will automatically be closed upon request of a full surrender.

6. PAYMENT INSTRUCTIONS

A. Send check to the address listed in Section 1 above.

B. Send check to the following address:

Address: _______________________________________ City:________________________ State:_____ ZIP:_______________

Special Mailing Instructions: _________________________________________________________________________________

C.To the extent permitted under the Internal Revenue Code, I wish to have the entire amount requested in section 3 (net of any applicable charges) directly transferred or rolled over as indicated in item F, G, H, or I of section 2 to the plan or provider below. (Conirmation from accepting plan or provider must be attached to this form.)

Plan or Provider Name: ___________________________________________________________ Phone Number: _________________________

Address: _____________________________________________________________________________________________________________

Name on Account: _______________________________________________________________ Account Number: _______________________

Page 2 of 12 |

eF |

7. FEDERAL INCOME TAX WITHHOLDING NOTICE – Eligible Rollover Distribution Amounts Paid to You

If you withdraw eligible rollover distribution amounts and have such amounts paid to you (rather than transferring or rolling over such amounts to another plan or an IRA), the taxable portion of such amounts will be subject to mandatory 20% Federal income tax withholding. You may have more than 20% withheld by checking the box below and writing in a dollar amount. If you are under 591/2, you may owe a 10% IRS premature distribution penalty.

In addition to the mandatory 20% Federal income tax withholding applicable to eligible rollover distribution amounts not rolled over, I want an additional

_________% or $___________ withheld on such amounts.

8.FEDERAL INCOME TAX WITHHOLDING INSTRUCTIONS – Amounts Not Eligible for Rollover Paid to You (Complete only if applicable)

If you withdraw amounts that cannot be rolled over (for example, a required minimum distribution after you reach age 701/2 or a payment to an alternate payee who is not the participant’s former spouse), the taxable part of such amounts will be subject to 10% Federal income tax withholding unless you elect to have no withholding apply. If you elect no withholding, or if you elect withholding and have insuficient Federal income tax withheld, you may be responsible for payment of estimated tax. You may incur penalties under the estimated tax rules if your withholding and estimated tax payments are insuficient. Even if you elect no Federal income tax withholding, you are responsible for Federal income tax on the taxable part of this withdrawal. You may owe a 10% IRS premature distribution penalty if you are under 591/2.

A. Do not withhold Federal income tax on payment to me of amounts not eligible for rollover. (Note: Checking this box does not waive the mandatory 20% Federal income tax withholding on eligible rollover distribution amounts paid to you.)

B. Withhold __________% (greater than 10%) for Federal income tax on payment to me of amounts not eligible for rollover.

9. STATE INCOME TAX WITHHOLDING INSTRUCTIONS (Complete only if applicable.)

Some states require MetLife to withhold state income tax if we withhold for Federal income tax. MetLife will calculate the amount of withholding for you. In some of these states, you may ask for no state income tax withholding (even though you requested or we are required to withhold for Federal income tax) or you may specify the amount you want withheld. In other states, no state income tax withholding will apply unless you indicate the amount you want withheld for state income tax.

A. Do NOT withhold for state income tax.

B. Withhold_____________% for state income tax.

10. PARTICIPANT/ALTERNATE PAYEE STATEMENT & SIGNATURE

As a participant or a former spouse alternate payee, I understand I have the right to consider whether to make or not make a direct rollover election with respect to eligible rollover distribution amounts and to consent to a distribution from my annuity account or contract without regard to the

I certify all of the information I have provided is true, accurate and complete to the best of my knowledge.

Participant/Alternate Payee Signature: ________________________________________________ Date: _________________________________

Participant/Alternate Payee Name (please print): _______________________________________________________________________________

Contract/Certiicate Number: _________________________________

11. PLAN ADMINISTRATOR/AUTHORIZED REPRESENTATIVE SIGNATURE (Complete for all ERISA Plans or Direct Transfer/Rollover Requests)

Participant is __________% vested. (only required for ERISA Plans)

I certify this withdrawal is permissible under the terms of the Plan, that all ERISA and Plan requirements have been satisied, and hereby approve this withdrawal request.

____________________________________________________________________________________________________________________

Plan Administrator/Authorized Representative Name (please print)

__________________________________________________________________________________ |

_______________________________ |

Plan Administrator/Authorized Representative Signature |

Date |

FOR

Page 3 of 12 |

eF |

12. ANNUITY INFORMATION, QJSA AND NOTICE WAIVER, AND SPOUSAL CONSENT

Note: This section does not apply if your Employer’s plan does not include a qualiied joint and survivor annuity (“QJSA”) provision.

Qualiied Joint and Survivor Annuity. ERISA and/or your Employer’s plan requires that your vested Plan Account Balance be paid in the form of a qualiied joint and survivor annuity (“QJSA”) unless you and (if you are married) your spouse elect a different payment alternative. The QJSA is an annuity payable to you for your lifetime and, upon your death, an annuity payable to your spouse for his or her lifetime. The amount of each annuity payment to your spouse will equal at least 50% of the annuity payment made to you. If you are not married or your spouse does not survive you, the payments under the QJSA will stop at your death. For more information concerning the amount of each payment and other terms of the QJSA, see the Plan Administrator or your Employer.

You may waive your right to have your vested Plan Account Balance paid in the form of a QJSA. If you are married and the contract value exceeds $5,000, your spouse must consent to this waiver in order for it to be valid. You (and your spouse) may do this by completing items A. and B. below. If you make such a waiver, all or part of your vested Plan Account Balance will be paid in accordance with your withdrawal election above.

A.Waiver of Annuity and Minimum Notice Period. I waive any right to claim that the part of my vested Plan Account Balance payable as a result of this withdrawal request be paid in the form of a QJSA. I request that my vested Plan Account Balance instead be paid to me in accordance with my election above. This waiver does not affect the payment of the remainder of my vested Plan Account Balance as a QJSA. I consent to an immediate distribution of the elected part of my vested Plan Account Balance. I afirmatively waive any unexpired part of the minimum

Participant Signature: ______________________________________________________ Date: ________________________

B.Spousal Consent*. (This section must be completed if the Participant is married and the contract value amount exceeds $5,000.) I, the Participant’s spouse, have received and understand the information provided above. I voluntarily consent to the payment election and above Waiver of Annuity completed by my spouse, the Participant. I understand the law requires my spouse’s Plan Account Balance be paid as an annuity (called a qualiied joint and survivor annuity) that will pay lifetime beneits to me if I survive my spouse. I may, but am not required to, waive my rights to this annuity. My spouse’s election to not receive his or her Plan Account Balance in the form of the qualiied joint and survivor annuity is not valid unless I consent to such election. By signing this Consent, I forever waive my rights to the annuity for this part of my spouse’s Plan Account Balance.

Spouse Signature: _________________________________________________________ Date: __________________________

Notarization of Spouse’s Signature

STATE OF ___________________________________________

COUNTY OF _________________________________________

The undersigned Notary Public certiies that ______________________________________ , personally known to me to be the same person whose name is subscribed to the foregoing document, appeared before me in person, and acknowledged the signature and delivery of this instrument as his or her free and voluntary act, for the uses and purposes therein set forth.

Notary Public Signature: ___________________________________________ |

Date: ___________________________________ |

Print Name of Notary: _____________________________________________ |

My Commission Expires: ____________________ |

OR

Plan Administrator/Authorized Representative Witness

The undersigned, with authority to act on behalf of the Plan, certiies that ________________________________ , the Participant’s spouse, appeared

before me in person, and executed the foregoing document freely and voluntarily.

Plan Administrator/Authorized Representative Signature: ____________________________ Date: __________________________

*If spousal consent is required but cannot be obtained, this form must be accompanied by an afidavit completed by the participant and approved by the Plan Administrator. The afidavit must state that spousal consent is not needed or cannot be obtained because: (1) the participant’s spouse cannot be found; or (2) the participant is legally separated from or has been abandoned by the spouse (within the meaning of local law) and has a court order to such effect and no qualiied domestic relations order exists that requires spousal consent to this withdrawal.

Page 4 of 12 |

eF |

INSTRUCTIONS

WHO MAY USE THIS FORM

If you are a participant, use this form to request a withdrawal from your 403(b) annuity (also known as a

If you are an alternate payee, use this form to request a distribution from a segregated TSA account set up on your behalf. Do not use this form if you are a beneiciary.

Be sure to read the attached Special Tax Notice Regarding TSA Payments information about rollovers, when they are allowed and not allowed, and the Federal income tax consequences of rollovers, direct rollovers, and payments not rolled over. Please note that a withdrawal may incur withdrawal charges. If your certiicate is for a

These instructions summarize MetLife’s understanding of tax rules that may apply to your withdrawal. Tax rules are complex and contain conditions and exceptions not included in these Instructions. MetLife does not offer these Instructions as tax advice, and you may not rely upon any statement therein as such. Consult your tax advisor and/or retirement planner before you request a withdrawal. For more speciic information on the tax treatment of payments from

TSA WITHDRAWAL INFORMATION

IRS rules restrict when you may make withdrawals from your TSA or 403(b)(7) custodial account. Your employer’s plan may include provisions in addition to the IRS restrictions below that further limit your ability to make withdrawals before you have a severance from employment.

|

|

|

IRS 403(b) Withdrawal Restrictions |

|

|

|

|

|

|

|

|

|

|

|

|

Restricted |

Restricted But Available for Hardship |

Unrestricted |

|

|

|

|

|

|

|||

|

Other than for hardship, amounts below are |

Subject to certain conditions, amounts below are |

Amounts below are generally eligible for |

|||

|

eligible for withdrawal only after participant’s |

available for hardship before participant’s age |

withdrawal at any time: |

|

||

|

age 591⁄2, severance from employment, death, |

591⁄2 or severance from employment: |

|

|

|

|

|

or disability: |

|

|

|

|

|

|

|

|

|

|

||

403(b) Annuity |

• |

• Your |

• Your voluntary |

|||

(“TSA”) |

|

but not their earnings. |

before 1989 and their |

|||

|

• Your |

• You and your employer’s |

• Your |

|||

|

|

and their earnings; and |

and their |

result of an |

irrevocable election |

or as |

|

• |

Amounts you or your employer contributed |

transferred to the TSA under Revenue Ruling |

a condition |

of employment and |

their |

|

earnings; |

|

|

|||

|

|

to a 403(b)(7) custodial account and that |

|

|

||

|

|

|

|

|

|

|

|

|

you later directly transferred under Revenue |

|

• Your |

||

|

|

Ruling |

|

earnings; |

|

|

|

|

|

|

• Your employer’s contributions and their |

||

|

|

|

|

earnings. |

|

|

|

|

|

|

• Above amounts that were directly |

||

|

|

|

|

transferred to your TSA from another TSA |

||

|

|

|

|

(other than a section 403(b)(7) custodial |

||

|

|

|

|

account); and |

|

|

|

|

|

|

• Eligible rollover distribution amounts |

||

|

|

|

|

you rolled to your TSA from another |

||

|

|

|

|

TSA, a 403(b)(7) custodial account, an |

||

|

|

|

|

IRA, a Section 401(a) or 403(a) plan, a |

||

|

|

|

|

governmental Section 457(b) plan, and |

||

|

|

|

|

their earnings. |

|

|

|

|

|

|

|

|

|

403(b)(7) |

• |

All amounts. |

• Your |

No amounts. |

|

|

Custodial |

|

|

but not their earnings; and |

|

|

|

Account |

|

|

• You and your employer’s |

|

|

|

|

|

|

and their |

|

|

|

|

|

|

|

|

|

|

Page 5 of 12 |

eF |