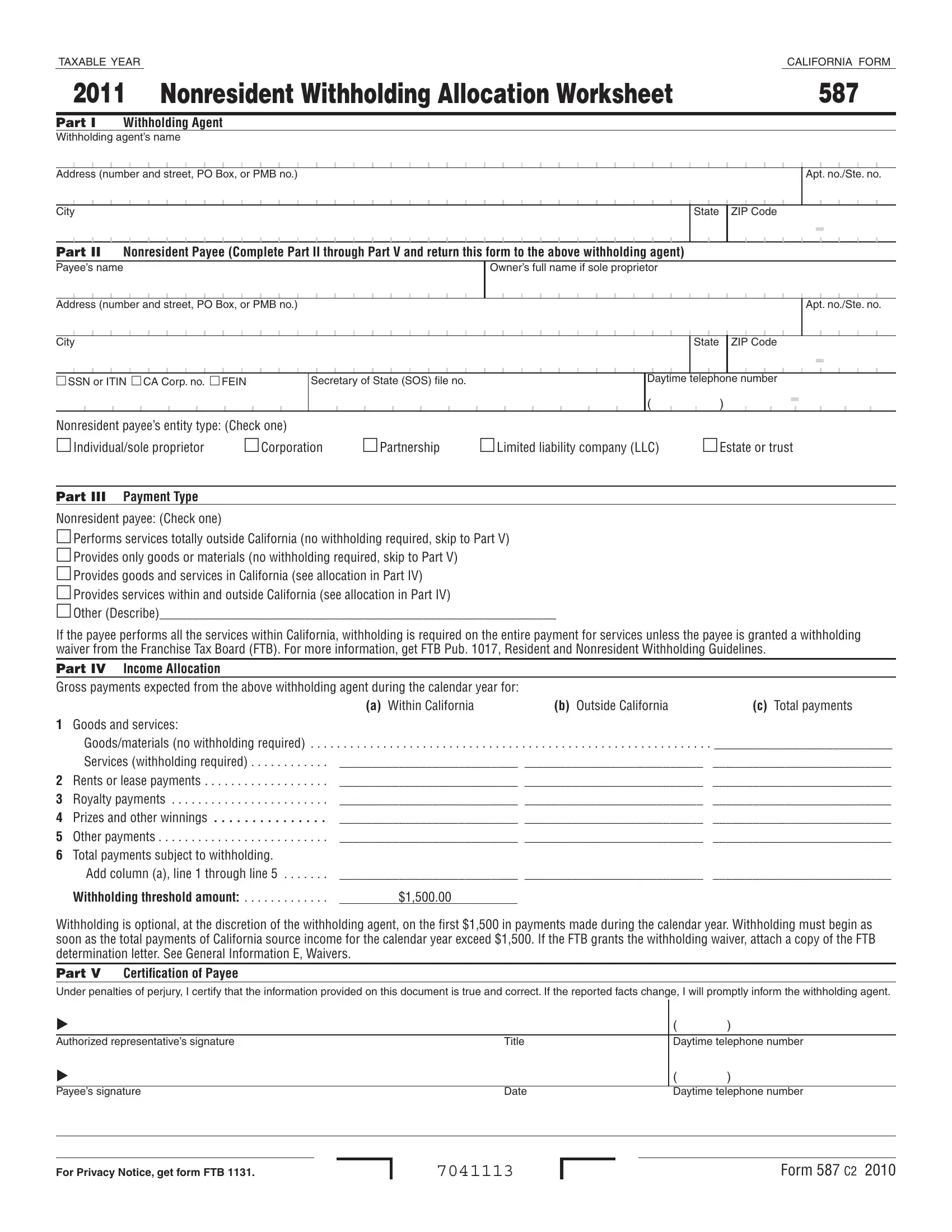

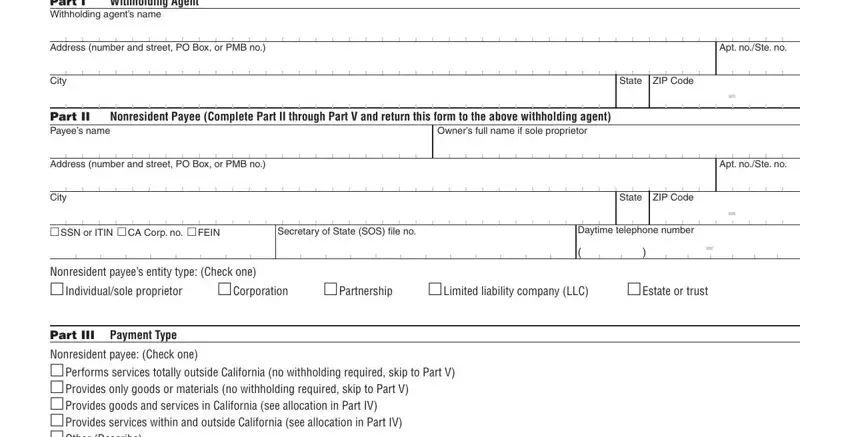

Who Needs to Complete California Form 587

California Form 587 is completed by nonresident payees before receiving California-source income from a withholding agent. If you are an individual, corporation, LLC, partnership, estate, or trust earning income from California but without a permanent California business location, your withholding agent will request this form. Return the signed form to your withholding agent before the first payment is made. The withholding agent keeps the form on file for at least five years to comply with California tax law.

How to Fill Out California Form 587 Online

ca form 587 fillable can be filled out online very easily. Just make use of FormsPal PDF editing tool to accomplish the job in a timely fashion. FormsPal team is aimed at making sure you have the ideal experience with our tool by constantly presenting new capabilities and enhancements. Our tool has become a lot more useful thanks to the latest updates! Now, filling out PDF documents is a lot easier and faster than ever before. With just a few easy steps, it is possible to start your PDF journey:

Step 1: First, access the pdf editor by pressing the "Get Form Button" at the top of this site.

Step 2: After you access the editor, you will get the form ready to be filled in. In addition to filling in different fields, you may as well do many other actions with the file, such as writing your own text, changing the original textual content, adding illustrations or photos, signing the form, and a lot more.

This document requires specific details. To ensure accuracy and reliability, remember to take note of the guidelines below:

1. It is crucial to complete the ca form 587 fillable accurately, hence be careful when filling out the parts that contain these blank fields:

2. Once your current task is complete, take the next step and fill out all of these fields - Nonresident payee Check one, Services withholding required, Goods/materials no withholding, Add column a line through line, b Outside California, a Within California, c Total payments, Withholding threshold amount, Withholding is optional at the, Certification of Payee, Authorized representatives, Payees signature, Title, Date, and Daytime telephone number with their corresponding information. Make sure to double check that everything has been entered correctly before continuing!

You can potentially make errors when filling out your Authorized representatives field, so make sure to reread it before you finalize the form.

Step 3: You should make sure your details are correct and then press "Done" to finish the process. Join FormsPal today and instantly access ca form 587 fillable, prepared for download. All alterations made by you are kept, allowing you to modify the document at a later point when required. FormsPal offers risk-free document editing devoid of personal data recording or distributing. Rest assured that your data is safe here!

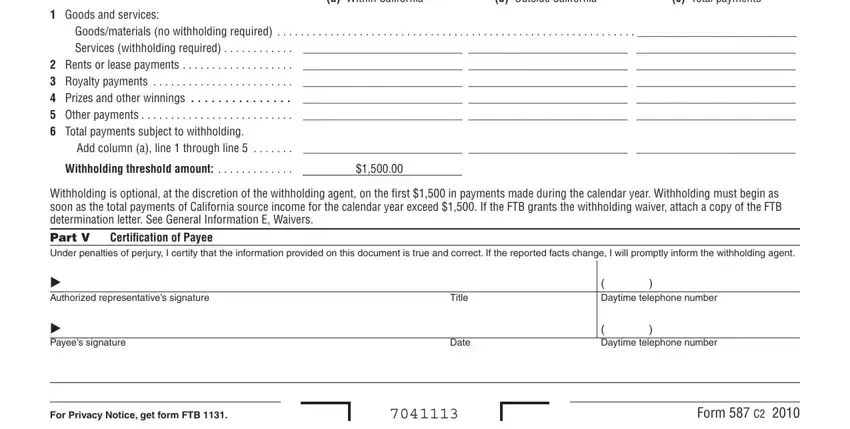

Key Fields on California Form 587

Form 587 is divided into four main parts: income allocation for services, income allocation for goods and materials, withholding calculation, and payee certification. In the income allocation part, you break down each payment type and identify how much relates to California versus non-California activity. The withholding calculation section uses your allocation to determine the required tax amount. Finally, the payee or an authorized representative signs the certification, confirming the accuracy of all information provided to the withholding agent.

Common Mistakes to Avoid on Form 587

One of the most frequent errors on California Form 587 is failing to separate California-source income from non-California income. Another common mistake is applying the wrong withholding rate. Individuals and partnerships should use the 7% rate, while corporations use 8.84%. S corporations are subject to the higher 13.8% rate. Always verify that the correct entity type and rate are entered before submitting the form to your California withholding agent.

Frequently Asked Questions About California Form 587

What is the purpose of California Form 587?

California Form 587 is used to allocate a nonresident payee's income between California and non-California sources so the withholding agent applies the correct tax withholding rate to only the California-source portion of the payment.

Who is a withholding agent?

A withholding agent is any person or entity that pays California-source income to a nonresident payee. Withholding agents include businesses, government agencies, and individuals who make such payments. They are responsible for obtaining Form 587 and remitting the required withholding tax to the California Franchise Tax Board.

How long does a withholding agent keep Form 587?

California withholding agents must keep completed Forms 587 for a minimum of five years after the end of the calendar year in which the withholding was paid. This record retention requirement supports compliance with California tax law and allows for audit verification.

Can nonresidents get a waiver from California withholding?

Yes. Nonresident payees who believe withholding should not apply may request a withholding waiver from the California FTB. Qualifying grounds include prior-year California net operating losses or active participation in a registered California business. The approved waiver allows the withholding agent to reduce or eliminate withholding on eligible payments.

Related California Tax and Withholding Forms

If you work with California nonresident withholding, you may also need the California Form 590-P (Withholding Exemption Certificate), the California Form 592-B (Nonresident Withholding Tax Statement), or the Income Withholding Form. These documents work alongside California Form 587 to ensure accurate tax withholding and reporting for all nonresident payees receiving California-source income.