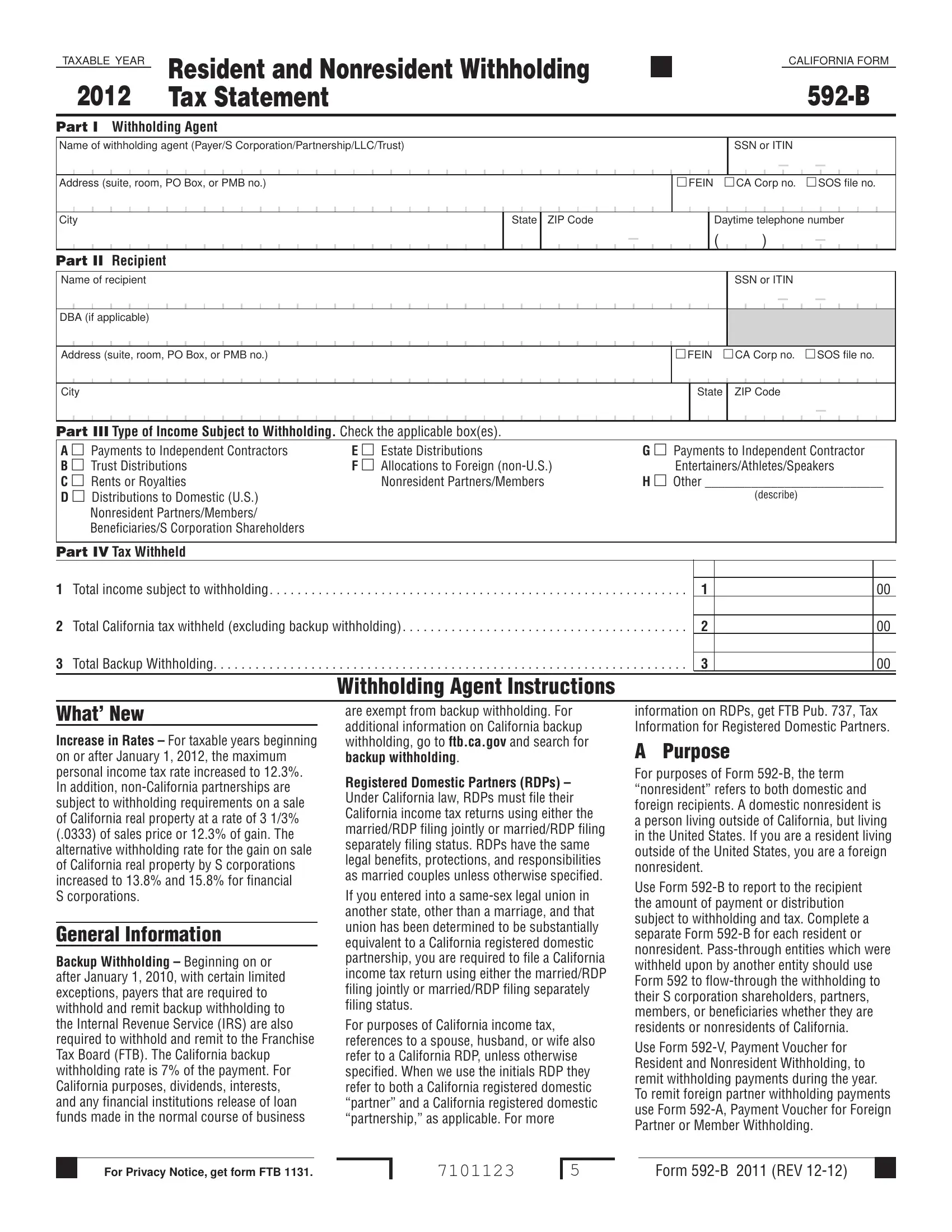

Who Needs California Form 592-B

California Form 592-B is required for any business, estate, or trust acting as a withholding agent in California. If your organization made payments to California residents and nonresidents during the calendar year, you must issue a separate Form 592-B to each payee from whom amounts were withheld. The California Franchise Tax Board (FTB) uses this statement to verify state income tax withholding compliance. Non-wage earners, independent contractors, and recipients of real property payments are among those most commonly issued this form. For related agreements, see also the independent contractor agreement and the earnings withholding order (WG-001).

How to Complete Form 592-B Online

You can fill out California Form 592-B online using the FormsPal PDF editor. Follow these steps to get started:

Step 1: Click the orange "Get Form" button above. This opens our editor so you can begin completing your form.

Step 2: Once the editor loads, you will find the form ready for input. In addition to filling in required fields, you can insert text, add a signature, or make other adjustments to the PDF.

This form requires specific information. Review the following before completing each section:

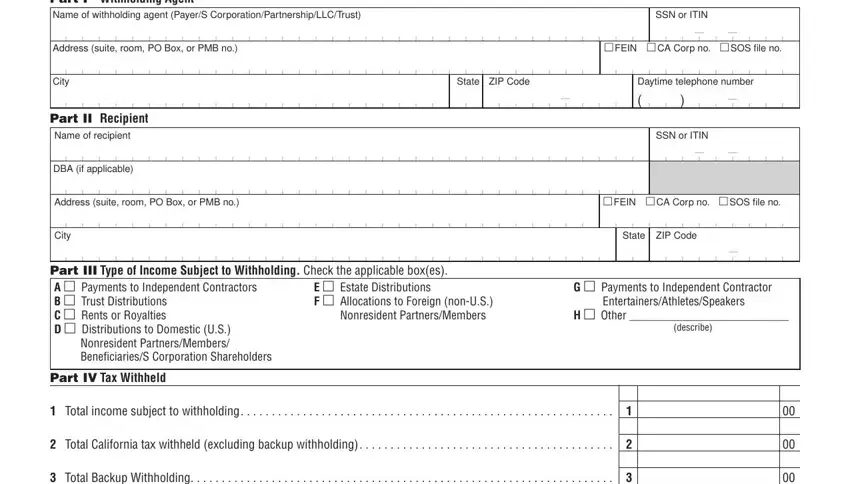

1. Start at the top of the form by entering the withholding agent's name, address, and FEIN or SSN. Gather all required information and verify that nothing is overlooked.

2. The next section requires: total income subject to withholding, total California withholding amount, total backup withholding, information on rate increases for new periods, General Information on Backup Withholding, Withholding Agent Instructions, Registered Domestic Partners (RDPs) details, and the applicable FTB Pub reference.

Take extra care with the rate increase section, as errors here may require correction before the form is accepted.

Step 3: After reviewing all entries, click "Done" to finalize your document. Create a free FormsPal account to save and download the completed PDF. Your changes are saved automatically, so you can return to edit at any time. FormsPal does not share any information you enter while completing documents.

Common Errors When Filing Form 592-B

The Franchise Tax Board identifies several frequent mistakes on this form. Withholding agents often omit the payee's ITIN or enter incorrect real property transaction amounts. Ensure the total payment amounts reported on Form 592-B match those submitted on the associated Form 592. Report backup withholding amounts separately from standard withholding. Issue a separate Form 592-B to each individual payee receiving payments subject to withholding, rather than combining multiple recipients on one form. Keeping accurate records throughout the calendar year makes it easier to complete the form accurately when it comes due on January 31.