You can complete the Canada TD1 form online at FormsPal without installing any software. The process takes only a few minutes and produces a completed PDF ready to give to your employer or payer.

Who Needs to File a Canada TD1 Form?

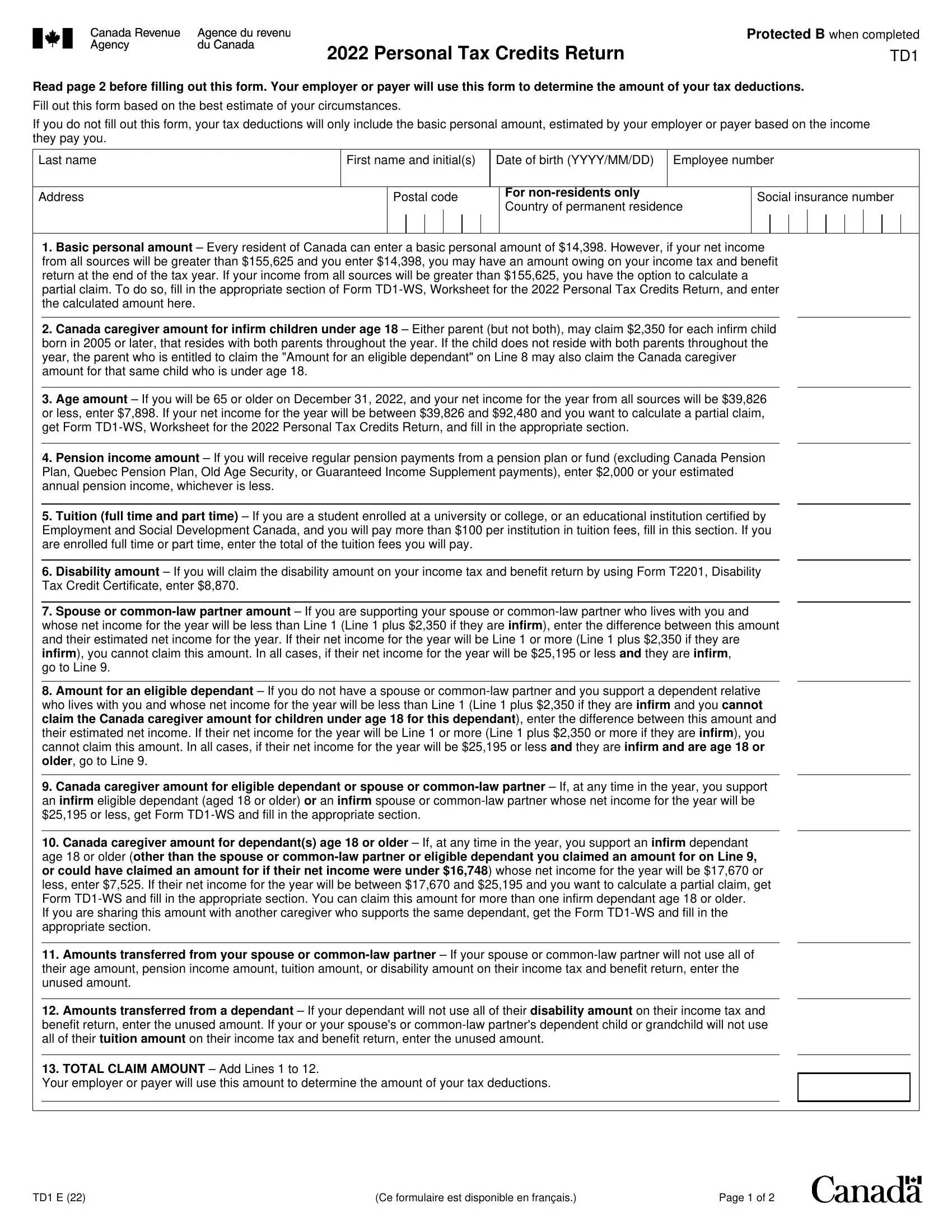

Every new employee in Canada must give a completed TD1 to their employer before their first paycheck. You also need to file a new TD1 when your tax credits change, such as after getting married, having a child, turning 65, or being approved for a disability amount. Both the federal TD1 and your provincial or territorial TD1 form must be completed.

How to Fill Out the TD1 Form Step by Step

Open the form using the button at the top of this page. Enter your full name and social insurance number in the identification section. Work through each numbered line to see which tax credits apply to you, then enter the dollar amount for each one you qualify for. Add your total claim amount on line 13. Sign and date the employee certification. Download the completed PDF and give it to your employer.

Frequently Asked Questions About the Canada TD1

What is the basic personal amount on a TD1 form?

The basic personal amount is a tax credit all Canadian taxpayers can claim. It is listed on line 1 of the TD1 and reduces the amount of income tax your employer withholds from your paycheck each period.

Do I need to submit a new TD1 form every year?

You only need to submit a new TD1 when your personal tax credits change. If your situation stays the same from year to year, your employer continues using the TD1 already on file.

What happens if I do not submit a TD1 form?

If you do not provide a completed TD1, your employer must withhold income tax based only on the basic personal amount credit. Submitting your TD1 form ensures you receive credit for all the deductions you qualify for.

Related Canadian Tax Forms

If you are completing employment tax paperwork in Canada, you may also need these forms available on FormsPal:

- Payroll Check Template for employers calculating TD1 deductions

- Canada T2 Corporate Tax Form for business income tax returns

- Canada T2220-E RRSP Transfer Form for retirement savings contributions