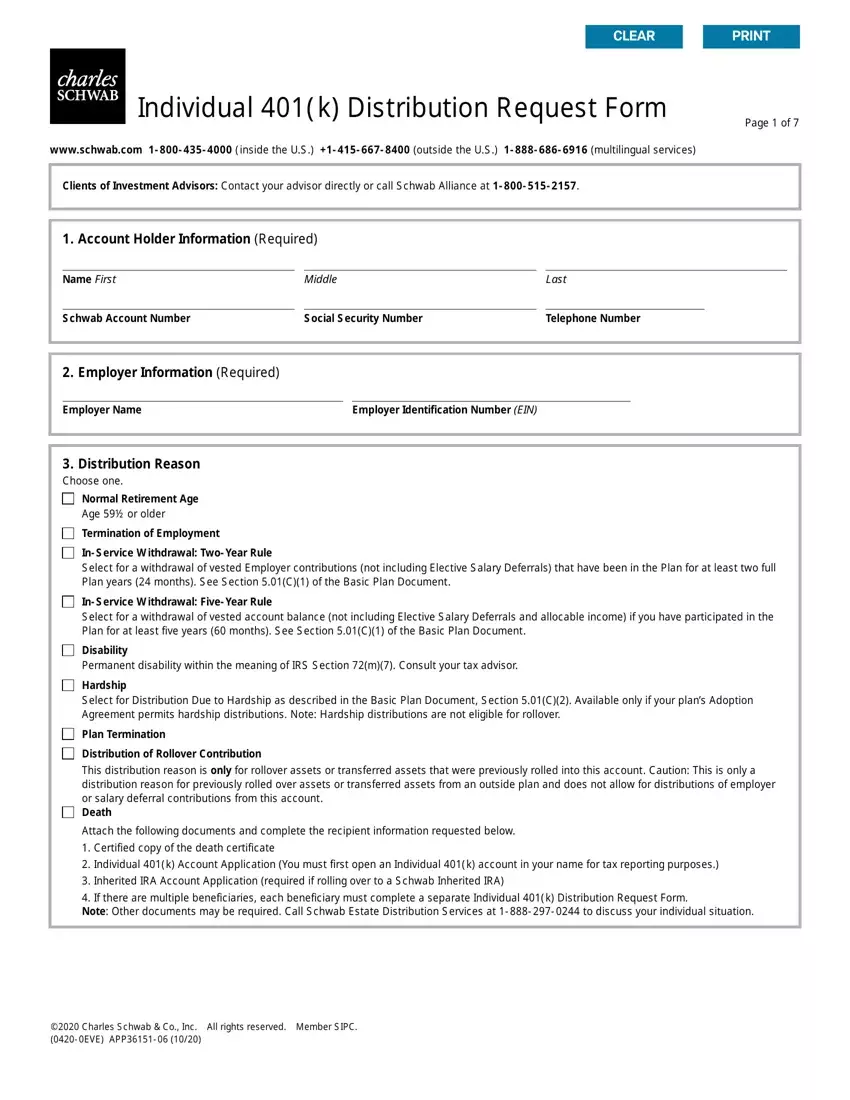

The Schwab Individual 401(k) Distribution Request Form is used to process withdrawals, rollovers, and distributions from a Charles Schwab i401k Plan. The form covers Account Holder Information, Employer Information, and the specific qualifying event for each request.

Who Needs This Form

Self-employed individuals, sole proprietors, and small business owners with a Schwab Individual 401(k) Plan submit this form when they need to withdraw funds. Beneficiaries and non-spouse beneficiaries also use it to request inherited account payouts or rollovers.

Qualifying Distribution Reasons

The form accepts these events: Normal Retirement Age (59.5 or older), Termination of Employment, In-Service Withdrawal under the Two-Year or Five-Year Rule, Permanent Disability, Hardship, Plan Termination, Rollover, and Qualified Domestic Relations Order (QDRO). Each reason has specific eligibility criteria, so choose the category that matches your situation.

Payment and Delivery Options

Account holders may choose a lump-sum payout, partial withdrawal, or periodic payments. Funds are delivered by direct deposit, mailed check, or rollover to a Schwab IRA, non-Schwab IRA, or qualified retirement plan. Non-spouse beneficiaries may roll over to a Schwab Inherited IRA or convert to a Roth IRA.

Investment Advisor and Self-Directed Instructions

Separate instructions apply for investment advisors and self-directed clients. Advisors must specify sale instructions for securities before funds are sent as cash. Clients without advisors follow a streamlined process for the same request.

Excess Deferrals and QDRO Requests

Dedicated sections cover excess deferral corrections and QDRO requests. Supporting documentation must be attached before submitting. These sections ensure IRS compliance for both standard withdrawals and court-ordered scenarios.

Processing Timeline

Once submitted, processing typically takes 3 to 5 business days for standard requests. Direct rollovers to another IRA or retirement plan may take 7 to 10 business days. Hardship and QDRO requests may require additional review time. Ensure all required fields and attachments are complete to avoid delays.

| Question | Answer |

|---|---|

| Form Name | Charles 401K Distribution Form |

| Issued By | Charles Schwab & Co., Inc. |

| Plan Type | Individual 401(k) / Schwab i401k |

| Form Length | 11 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 2 min 45 sec |

| Common Uses | Retirement payouts, rollovers, hardship withdrawals, QDRO |

| Other names | charles withdrawal form, charles schwab 401k distribution request form, schwab i401k distribution form, charles schwab 401k withdrawal |