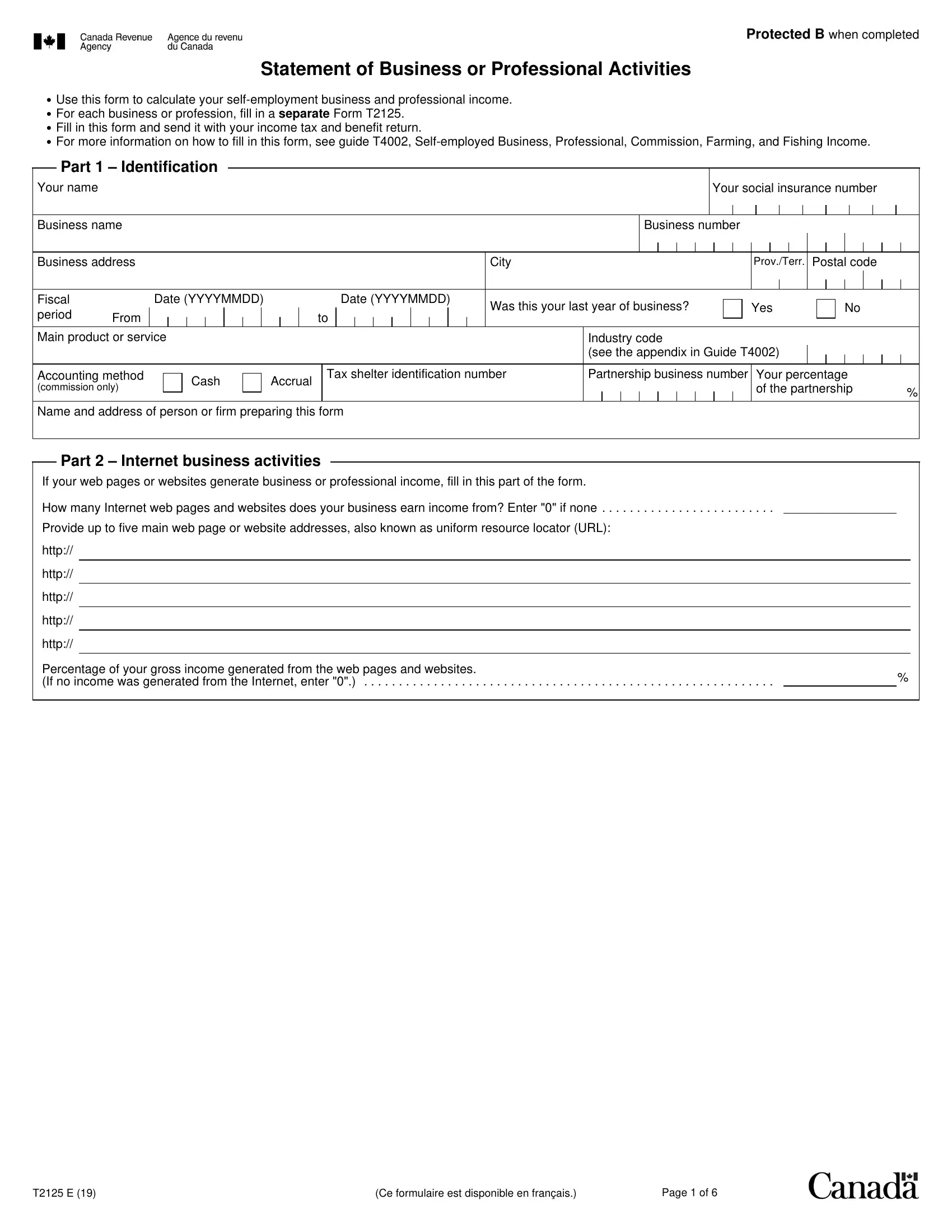

For those navigating the waters of self-employment, the CRA T2125 form is an essential piece of documentation that demands attention. When you're running your own business or offering professional services independently, understanding and accurately filling out this form becomes crucial in calculating your business and professional income for tax purposes. This form is designed to accommodate the unique aspects of self-employment income, asking for detailed information about your business or professional activities. It's important that for each business or profession you operate, a separate form T2125 needs to be filled out. This inclusivity captures a broad range of self-employment endeavors, from freelance operations to professional services, ensuring each avenue of income is reported and taxed accordingly. The form also delves into specifics such as the method of accounting you use, whether cash or accrual, and requires details about internet business activities if applicable. Another aspect it covers is the reporting of gross business or professional income and allows for deductions like GST/HST and business-use-of-home expenses. With a section dedicated to calculating net income before and after adjustments, it plays a pivotal role in the tax filing process for the self-employed. By comprehensively understanding and meticulously filling out the CRA T2125, self-employed individuals can ensure they meet their tax obligations and potentially optimize their tax situation.

| Question | Answer |

|---|---|

| Form Name | Cra Form T2125 |

| Form Length | 6 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 1 min 30 sec |

| Other names | statement form t2125, form t2125, t2125 file, t2125 form pdf |

Protected B when completed

Statement of Business or Professional Activities

•Use this form to calculate your

•For each business or profession, fill in a separate Form T2125.

•Fill in this form and send it with your income tax and benefit return.

•For more information on how to fill in this form, see guide T4002,

|

Part 1 – Identification |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

Your name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Your social insurance number |

|

|

|

||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Business name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Business number |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Business address |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City |

|

|

|

|

|

|

|

|

|

|

|

|

Prov./Terr. |

Postal code |

|

|

|

||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Fiscal |

|

Date (YYYYMMDD) |

|

|

|

|

|

|

Date (YYYYMMDD) |

|

|

Was this your last year of business? |

|

|

|

Yes |

|

|

|

|

|

|

|

|

No |

|

|

|

||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||

period |

From |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

to |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

Main product or service |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Industry code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(see the appendix in Guide T4002) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

Accounting method |

|

|

|

|

|

|

Cash |

|

|

Accrual |

Tax shelter identification number |

|

Partnership business number |

|

Your percentage |

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||

(commission only) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

of the partnership |

% |

||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Name and address of person or firm preparing this form |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||

|

Part 2 – Internet business activities |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||

If your web pages or websites generate business or professional income, fill in this part of the form. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||

How many Internet web pages and websites does your business earn income from? Enter "0" if none |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||

Provide up to five main web page or website addresses, also known as uniform resource locator (URL): |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||

http:// |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

http:// |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

http:// |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

http:// |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

http:// |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Percentage of your gross income generated from the web pages and websites. |

|

% |

(If no income was generated from the Internet, enter "0".) |

T2125 E (19) |

(Ce formulaire est disponible en français.) |

Page 1 of 6 |

Protected B when completed

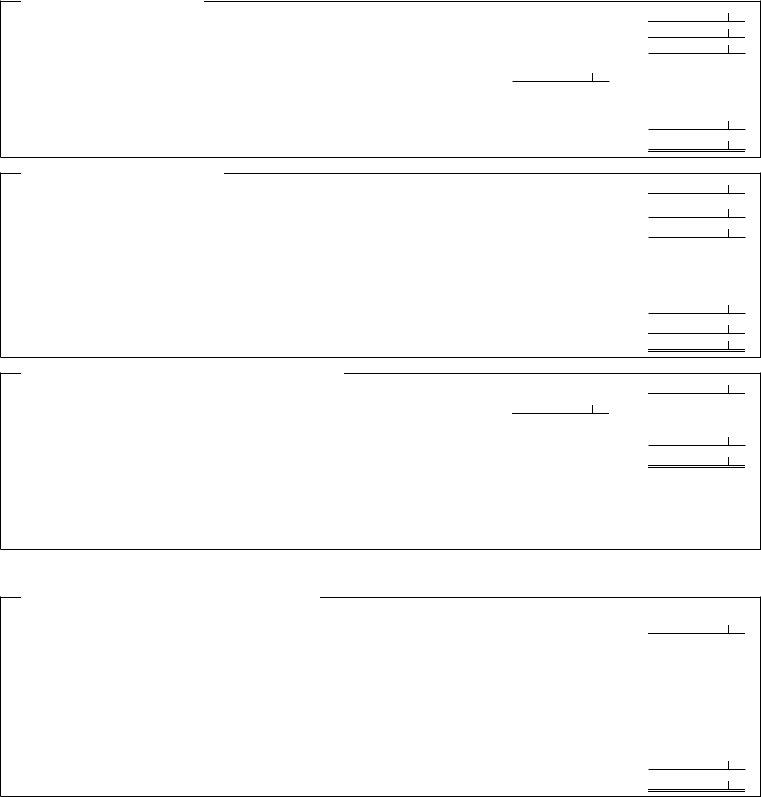

Part 3A – Business income

Fill in this part only if you have business income. If you have professional income, leave this part blank and fill in Part 3B. If you have both business and professional income, you have to fill out a separate Form T2125 for each.

Part 3B – Professional income

Fill in this part only if you have professional income. If you have business income, leave this part blank and fill in Part 3A. If you have both business and professional income, you have to fill out a separate Form T2125 for each.

Note: New rules allow you to include your work in progress (WIP) progressively if you elected to use billed basis accounting for the last tax year that started before March 22, 2017. Generally, for the first tax year that starts after March 21, 2017, you must include 20% of the lesser of the cost and the fair market value of WIP. The inclusion rate increases to 40% in the second tax year that starts after March 21, 2017, 60% in the third year, 80% in the fourth year, and 100% in the fifth and all subsequent tax years. For more information, see chapter 2 of guide T4002.

Part 3A – Business income

Gross sales, commissions, or fees (include GST/HST collected or collectible) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

GST/HST, provincial sales tax, returns, allowances, discounts, and GST/HST adjustments (included in amount 3A) . . . . . . . . . . . . . . .

Subtotal: Amount 3A minus amount 3B

If you are using the quick method for GST/HST – Government assistance calculated as follows: |

3D |

GST/HST collected or collectible on sales, commissions and fees eligible for the quick method |

GST/HST remitted, (sales, commissions, and fees eligible for the quick method plus

GST/HST collected or collectible) multiplied by the applicable quick method remittance rate |

|

|

3E |

|

|

||

Subtotal: Amount 3D minus amount 3E |

|||

Adjusted gross sales: Amount 3C plus amount 3F (enter on line 8000 of Part 3C) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

3A

3B

3C

3F

3G

Part 3B – Professional income

Gross professional fees including

GST/HST, provincial sales tax, returns, allowances, discounts, and GST/HST adjustments (included in amount 3H) and any WIP at the end of the year you elected to exclude . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Subtotal: Amount 3H minus amount 3I

If you are using the quick method for GST/HST – Government assistance calculated as follows:

GST/HST collected or collectible on professional fees eligible for the quick method . . . . . . . . . . . . . . . 3K GST/HST remitted, (professional fees eligible for the quick method plus GST/HST collected or

collectible) multiplied by the applicable quick method remittance rate |

|

|

|

3L |

|

|

|

||

. . . . . . . . . |

|

|

|

|

|

Subtotal: Amount 3K minus amount 3L |

|||

Adjusted professional fees: Amount 3J plus amount 3M plus amount 3N (enter on line 8000 of Part 3C) . . . . . . . . . . . . . . . . . . . . . .

Part 3C – Gross business or professional income

Adjusted gross sales (amount 3G) or adjusted professional fees (amount 3O) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8000 Reserves deducted last year . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8290

Other income |

8230 |

|

|

|

► |

Subtotal. . . . . . . .: .Line. . . 8290. . . . .plus. . . .line. 8230 |

|

|

|

||

|

|

|

|

||

|

|

|

|

||

|

|

|

|

|

|

Gross business or professional income: Line 8000 plus amount 3P |

8299 |

|

|

Report the gross business or professional income from line 8299 on the applicable line of your income tax and benefit return |

|

as indicated below: |

|

•business income on line 13499

•professional income on line 13699

•commission income on line 13899

For Parts 3D, 4, and 5, if GST/HST has been remitted or an input tax credit has been claimed, do not include GST/HST when you calculate the cost of goods sold, expenses, or net income (loss).

Part 3D – Cost of goods sold and gross profit

If you have business income, fill in this part. Enter only the business part of the costs.

Gross business income (line 8299 of Part 3C). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Opening inventory (include raw materials, goods in process, and finished goods) |

8300 |

|

|

|

|

3R |

|

|

|

|

|||

|

|

|

|

|

3S |

|

Purchases during the year (net of returns, allowances, and discounts) |

8320 |

|

|

|

|

|

|

|

|

|

|||

8340 |

|

|

|

|

3T |

|

Direct wage costs |

|

|

|

|

||

|

|

|

|

|||

|

|

|

|

|

3U |

|

Subcontracts |

8360 |

|

|

|

|

|

|

|

|

|

|||

8450 |

|

|

|

|

3V |

|

Other costs |

|

|

|

|

||

|

|

|

|

|||

|

|

|

|

|

3W |

|

Subtotal: Add amounts 3R to 3V |

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Closing inventory (include raw materials, goods in process, and finished goods) |

8500 |

|

|

|

|

► |

|

|

|

|

|||

8518 |

|

|

|

|

||

Cost of goods sold: Amount 3W minus line 8500 |

|

|

|

|

||

|

|

|

|

|||

|

|

|

|

|

||

|

|

|

|

|

|

|

Gross profit (or loss): Amount 3Q minus line 8518 |

8519 |

|

3H

3I

3J

3M

3N

3O

3P

3Q

Page 2 of 6