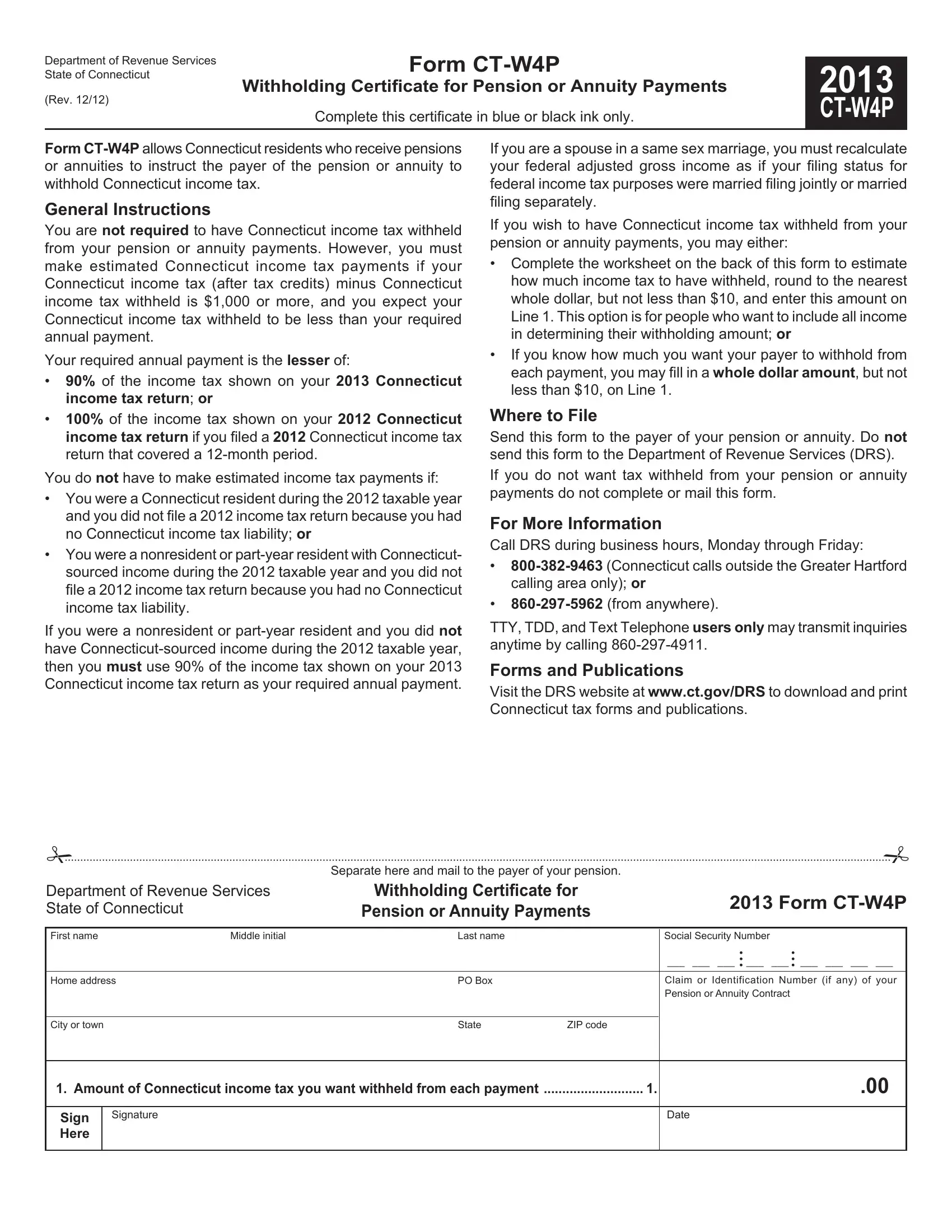

Understanding the CT-W4P Form is crucial for Connecticut residents who receive pensions or annuities and wish to manage their state income tax withholding effectively. This form, updated in December 2012 for the year 2013, serves as a guide for individuals to instruct their pension or annuity payer on how much Connecticut state income tax to withhold from their payments. Importantly, it provides a choice: recipients are not obligated to have taxes withheld, yet they must be aware that if their expected tax dues, after credits and withholdings, exceed $1,000, estimated tax payments are necessary. The form offers detailed instructions for calculating the appropriate withholding amount, accommodating various individual circumstances, including residency status and the intricacies related to same-sex marriages. Additionally, it is equipped with worksheets to assist in the estimation of federal adjusted gross income and subsequent tax liabilities. Filing this form with the pension or annuity payer (not with the Department of Revenue Services) and understanding its components can significantly influence one’s tax management and compliance with Connecticut tax laws. Furthermore, the form emphasizes the importance of accurate estimation of tax liabilities to avoid underpayment penalties, showcasing its role not just as a procedural document but as a critical tool for financial planning.

| Question | Answer |

|---|---|

| Form Name | Ct W4P Form |

| Form Length | 6 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 1 min 30 sec |

| Other names | print ct w4p, 6a, fs j7n150672221, fillable ct w4p |

Department of Revenue Services State of Connecticut

(Rev. 12/12)

Form

Withholding Certifi cate for Pension or Annuity Payments

Complete this certifi cate in blue or black ink only.

2013

Form

General Instructions

You are not required to have Connecticut income tax withheld from your pension or annuity payments. However, you must make estimated Connecticut income tax payments if your Connecticut income tax (after tax credits) minus Connecticut income tax withheld is $1,000 or more, and you expect your Connecticut income tax withheld to be less than your required annual payment.

Your required annual payment is the lesser of:

•90% of the income tax shown on your 2013 Connecticut income tax return; or

•100% of the income tax shown on your 2012 Connecticut income tax return if you filed a 2012 Connecticut income tax return that covered a

You do not have to make estimated income tax payments if:

•You were a Connecticut resident during the 2012 taxable year and you did not file a 2012 income tax return because you had no Connecticut income tax liability; or

•You were a nonresident or

If you were a nonresident or

If you are a spouse in a same sex marriage, you must recalculate your federal adjusted gross income as if your filing status for federal income tax purposes were married filing jointly or married filing separately.

If you wish to have Connecticut income tax withheld from your pension or annuity payments, you may either:

•Complete the worksheet on the back of this form to estimate how much income tax to have withheld, round to the nearest whole dollar, but not less than $10, and enter this amount on Line 1. This option is for people who want to include all income in determining their withholding amount; or

•If you know how much you want your payer to withhold from each payment, you may fill in a whole dollar amount, but not less than $10, on Line 1.

Where to File

Send this form to the payer of your pension or annuity. Do not send this form to the Department of Revenue Services (DRS). If you do not want tax withheld from your pension or annuity payments do not complete or mail this form.

For More Information

Call DRS during business hours, Monday through Friday:

•

•

TTY, TDD, and Text Telephone users only may transmit inquiries anytime by calling

Forms and Publications

Visit the DRS website at www.ct.gov/DRS to download and print Connecticut tax forms and publications.

Separate here and mail to the payer of your pension.

Department of Revenue Services |

Withholding Certificate for |

2013 Form |

|||||

State of Connecticut |

Pension or Annuity Payments |

||||||

|

|

||||||

|

|

|

|

|

|

|

|

First name |

Middle initial |

Last name |

|

Social Security Number |

|

||

|

|

|

|

|

• |

• |

|

|

|

|

|

|

___ ___ ___ •• ___ |

___ •• ___ ___ ___ ___ |

|

Home address |

PO Box |

|

Claim or Identification Number (if any) of your |

||||

|

|

|

|

|

Pension or Annuity Contract |

||

|

|

|

|

|

|

|

|

City or town |

|

State |

ZIP code |

|

|

||

|

|

|

|

||||

1. Amount of Connecticut income tax you want withheld from each payment ........................... 1. |

|

.00 |

|||||

|

|

|

|

|

|

|

|

Sign |

|

Signature |

|

|

Date |

|

|

Here |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Page 1 of 6

|

2013 Form |

||

|

Use this worksheet if you wish to include all 2013 estimated income in determining withholding amount. |

||

|

|

|

|

1. |

Federal adjusted gross income you expect in the 2013 taxable year (from 2013 |

|

|

|

federal Form 1040ES, 2013 Estimated Tax Worksheet, Line 1) |

1. |

_______________________ |

2. |

Allowable Connecticut modifi cations: See subtractions or additions below |

2. |

_______________________ |

3. |

Connecticut adjusted gross income: Combine Line 1 and Line 2 |

3. |

_______________________ |

|

Nonresidents and |

|

|

|

than your Connecticut adjusted gross income. |

|

|

4. |

Connecticut income tax: Complete the Tax Calculation Schedule below |

4. |

_______________________ |

5. |

Apportionment factor: Connecticut residents enter 1.0000. Nonresidents and |

|

|

|

residents, see instructions on Page 3 |

5. |

• |

6. |

Multiply Line 5 by Line 4 |

6. |

_______________________ |

7. |

Credit for income taxes paid to qualifying jurisdictions: See instructions on Page 3 |

7. |

_______________________ |

8. |

Subtract Line 7 from Line 6 |

8. |

_______________________ |

9. |

Estimated Connecticut alternative minimum tax: See instructions on Page 3 |

9. |

_______________________ |

10. |

Add Line 8 and Line 9 |

10. |

_______________________ |

11. |

Estimated allowable credits from Schedule |

11. |

_______________________ |

12. |

Total estimated income tax: Subtract Line 11 from Line 10 |

12. |

_______________________ |

13. |

Connecticut income tax withheld or expected to be withheld during the 2013 taxable year |

|

|

|

on income other than this pension or annuity |

13. |

_______________________ |

14. |

Subtract Line 13 from Line 12. If this amount is less than $1,000, no estimated payment |

|

|

|

is required |

14. |

_______________________ |

15. |

Amount to be withheld from each payment: Divide Line 14 by the number of payments |

|

|

|

you will receive in 2013. Round to the nearest whole dollar but not less than $10 |

15. |

_______________________ |

|

|

|

|

2013 Tax Calculation Schedule

1. Enter the amount from Line 3 above. |

1. |

|

00 |

|

|

|

|

|

|

2. |

Enter exemption from Table A - Personal EXemptions, If zero, enter “0.” |

2. |

|

00 |

|

|

|

|

|

3. |

Connecticut taxable income: Subtract Line 2 from Line 1. If less than zero, enter “0.” |

3. |

|

00 |

|

|

|

|

|

4. |

Tax calculation: See Table B - Withholding Tax Calculation. |

4. |

|

00 |

|

|

|

|

|

5. |

Enter the amount from Table C - 3% Tax Rate |

5. |

|

00 |

|

|

|

|

|

6. |

Enter the amount from Table D - Tax Recapture. If zero, enter “0.” |

6. |

|

00 |

|

|

|

|

|

7. |

Connecticut income tax: Add Line 4, Line 5, and Line 6. |

7. |

|

00 |

|

|

|

|

|

8. |

Enter decimal amount from Table E - Personal Tax Credits. If zero, enter “0.” |

8. |

0. |

|

|

|

|

|

|

9. |

Multiply the amount on Line 7 by the decimal amount on Line 8. |

9. |

|

00 |

|

|

|

|

|

10. |

Connecticut Income Tax: Subtract Line 9 from Line 7. Enter this amount on Line 4 of 2013 |

|

|

|

|

Form |

10. |

|

00 |

|

|

|

|

|

Caution: If you expect to owe $1,000 or more in Connecticut income tax after subtracting Connecticut income tax withheld, you may be required to make estimated payments. Generally, if you do not prepay (through timely estimated tax payments or withholding, or both) the lesser of 100% of the income tax shown on your 2012 Connecticut income tax return or 90% of the income tax shown on your 2013 Connecticut income tax return, you may owe interest at the rate of 1% per month or fraction of a month.

2013 Form

Any reference in these instructions to filing jointly includes filing jointly for federal and Connecticut and filing jointly for Connecticut only. Likewise, filing separately includes filing separately for federal and Connecticut and filing separately for Connecticut only.

Line 1: Your estimated federal adjusted gross income.

Adjusted gross income means wages, interest, dividends, alimony received, and all income minus certain adjustments to income such as alimony paid and qualified contributions to an IRA.

Line 2: Enter the total of your estimated allowable Connecticut modifications.

Subtractions include any items included in federal adjusted gross income that are not taxable under Connecticut law.

Additions include items taxable under Connecticut law but not included in federal adjusted gross income.

See Form

2013 Form

Page 2 of 6

Social Security Benefit Adjustment Worksheet

Enter the amount you expect to enter on Form |

___________________ |

||

If your fi ling status is single or filing separately, is the amount on Line 1 |

$50,000 or more? |

|

|

Yes |

Complete this worksheet. |

|

|

No |

Do not complete this worksheet.* |

|

|

If your filing status is filing jointly, qualifying widow(er) with dependent child, or head of household, is the amount on Line 1 $60,000 or more? Yes Complete this worksheet.

No Do not complete this worksheet.*

*Enter the amount of federally taxable Social Security benefits you expect to report on federal Form 1040, Line 20b, or federal Form 1040A, Line 14b, on the 2013 Form

A.Enter the amount you reported on federal Publication 505, Tax Withholding and Estimated Tax, Worksheet

|

|

2013 Estimated Tax |

A. |

|

|

|

|

If Line A is zero or less, stop here. Otherwise, go to Line B. |

|

|

|

|

B. Enter the amount you reported on federal Publication 505, Worksheet |

B. |

|

||

|

|

If Line B is zero or less, stop here. Otherwise, go to Line C. |

|

|

|

|

|

|

|

|

|

|

C. |

Enter the lesser of Line A or Line B. |

C. |

|

|

|

|

|

|

|

|

|

D. |

Multiply Line C by 25% (.25). |

D. |

|

|

|

|

|

|

|

|

|

E. Expected taxable amount of Social Security benefi ts you reported on federal Publication 505*, |

E. |

|

||

|

|

Worksheet |

|

|

|

|

|

|

|

|

|

|

F. |

Social Security Benefit Adjustment: Subtract Line D from Line E. Enter the amount here |

F. |

|

|

|

|

and as a subtraction on the 2013 Form |

|

|

|

|

|

Line E, enter “0.” |

|

|

|

*You may obtain federal Publication 505 by visiting the IRS website at www.irs.gov or by calling the Internal Revenue Service (IRS) at

Line 2 (continued)

Social Security Benefit Adjustment: If you file a federal income tax return as single or married filing separately and you expect your 2013 federal adjusted gross income will be less than $50,000, enter as a subtraction the amount of federally taxable Social Security benefits you expect to report on your 2013 federal Form 1040, Line 20b, or federal Form 1040A, Line 14b.

If you will file a federal income tax return as married filing jointly, qualifying widow(er) with dependent child, or head of household and you expect your 2013 federal adjusted gross income will be less than $60,000, enter as a subtraction the amount of federally taxable Social Security benefits you expect to report on your 2013 federal Form 1040, Line 20b, or federal Form 1040A, Line 14b.

If you expect your federal adjusted gross income will be above the threshold for your filing status, complete the Social Security Benefit Adjustment Worksheet above. Enter the Line F amount as a subtraction on Line 2.

Military Pensions: If you are a retired member of the U.S. armed forces or the National Guard, enter as a subtraction 50% of the amount of federally taxable military retirement pay you expect to report on your 2013 federal income tax return.

Line 3 - Nonresidents and

Line 5 - Nonresidents and

adjusted gross income, complete the following calculation and enter the result on Line 5.

= Line 5

Connecticut Adjusted Gross Income (Line 3)

Do not enter a number less than zero or greater than 1. If the result is less than zero, enter “0”; if greater than 1, enter 1.0000. Round to four decimal places.

Line 7 - Resident and

-Credit for Income Taxes Paid to Qualifying Jurisdictions of Form

Line 9: If you expect to owe federal alternative minimum tax for the 2013 taxable year, you may also owe Connecticut alternative minimum tax. Enter your estimated Connecticut alternative minimum tax liability. See instructions for Form

Line 11: Enter estimated allowable Connecticut income tax credit(s). Enter “0” if you are not entitled to a credit. (Credit for a prior year alternative minimum tax is not allowed if you entered an amount on Line 9.) See the instructions for Schedule

Line 15: Divide the amount on Line 14 by the number of pension or annuity payments you will receive in 2013. Round to nearest whole dollar but not less than $10. Enter this amount on Line 1 of the certifi cate on the front of this form.

2013 Form

Page 3 of 6

Table A - Personal exemptions for 2013 Taxable Year

Use the filing status you expect to report on your 2013 tax return and your Connecticut AGI *** (from Tax Calculation Schedule, Line 1) to determine your exemption.

|

|

Single |

|

|

|

Filing Jointly or |

|

|

Filing Separately |

|

|

Head of Household |

|||||||

|

|

|

|

|

Qualified Widow(er) |

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

Connecticut AGI *** |

Exemption |

Connecticut AGI *** |

Exemption |

Connecticut AGI *** |

Exemption |

Connecticut AGI *** |

Exemption |

||||||||||||

More Than |

Less Than |

|

|

More Than |

Less Than |

|

|

More Than |

Less Than |

|

|

More Than |

Less Than |

|

|

||||

|

|

or Equal To |

|

|

|

|

or Equal To |

|

|

|

|

or Equal To |

|

|

|

|

or Equal To |

|

|

$ |

0 |

$28,000 |

$ |

14,000 |

$ |

0 |

$48,000 |

$ |

24,000 |

$ |

0 |

$24,000 |

$ |

12,000 |

$ |

0 |

$38,000 |

$ |

19,000 |

$ |

28,000 |

$29,000 |

$ |

13,000 |

$ |

48,000 |

$49,000 |

$ |

23,000 |

$ |

24,000 |

$25,000 |

$ |

11,000 |

$ |

38,000 |

$39,000 |

$ |

18,000 |

$ |

29,000 |

$30,000 |

$ |

12,000 |

$ |

49,000 |

$50,000 |

$ |

22,000 |

$ |

25,000 |

$26,000 |

$ |

10,000 |

$ |

39,000 |

$40,000 |

$ |

17,000 |

$ |

30,000 |

$31,000 |

$ |

11,000 |

$ |

50,000 |

$51,000 |

$ |

21,000 |

$ |

26,000 |

$27,000 |

$ |

9,000 |

$ |

40,000 |

$41,000 |

$ |

16,000 |

$ |

31,000 |

$32,000 |

$ |

10,000 |

$ |

51,000 |

$52,000 |

$ |

20,000 |

$ |

27,000 |

$28,000 |

$ |

8,000 |

$ |

41,000 |

$42,000 |

$ |

15,000 |

$ |

32,000 |

$33,000 |

$ |

9,000 |

$ |

52,000 |

$53,000 |

$ |

19,000 |

$ |

28,000 |

$29,000 |

$ |

7,000 |

$ |

42,000 |

$43,000 |

$ |

14,000 |

$ |

33,000 |

$34,000 |

$ |

8,000 |

$ |

53,000 |

$54,000 |

$ |

18,000 |

$ |

29,000 |

$30,000 |

$ |

6,000 |

$ |

43,000 |

$44,000 |

$ |

13,000 |

$ |

34,000 |

$35,000 |

$ |

7,000 |

$ |

54,000 |

$55,000 |

$ |

17,000 |

$ |

30,000 |

$31,000 |

$ |

5,000 |

$ |

44,000 |

$45,000 |

$ |

12,000 |

$ |

35,000 |

$36,000 |

$ |

6,000 |

$ |

55,000 |

$56,000 |

$ |

16,000 |

$ |

31,000 |

$32,000 |

$ |

4,000 |

$ |

45,000 |

$46,000 |

$ |

11,000 |

$ |

36,000 |

$37,000 |

$ |

5,000 |

$ |

56,000 |

$57,000 |

$ |

15,000 |

$ |

32,000 |

$33,000 |

$ |

3,000 |

$ |

46,000 |

$47,000 |

$ |

10,000 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

$ |

37,000 |

$38,000 |

$ |

4,000 |

$ |

57,000 |

$58,000 |

$ |

14,000 |

$ |

33,000 |

$34,000 |

$ |

2,000 |

$ |

47,000 |

$48,000 |

$ |

9,000 |

$ |

38,000 |

$39,000 |

$ |

3,000 |

$ |

58,000 |

$59,000 |

$ |

13,000 |

$ |

34,000 |

$35,000 |

$ |

1,000 |

$ |

48,000 |

$49,000 |

$ |

8,000 |

$ |

39,000 |

$40,000 |

$ |

2,000 |

$ |

59,000 |

$60,000 |

$ |

12,000 |

$ |

35,000 |

and up |

$ |

0 |

$ |

49,000 |

$50,000 |

$ |

7,000 |

$ |

40,000 |

$41,000 |

$ |

1,000 |

$ |

60,000 |

$61,000 |

$ |

11,000 |

|

|

|

|

|

$ |

50,000 |

$51,000 |

$ |

6,000 |

$ |

41,000 |

and up |

$ |

0 |

$ |

61,000 |

$62,000 |

$ |

10,000 |

|

|

|

|

|

$ |

51,000 |

$52,000 |

$ |

5,000 |

|

|

|

|

|

$ |

62,000 |

$63,000 |

$ |

9,000 |

|

|

|

|

|

$ |

52,000 |

$53,000 |

$ |

4,000 |

|

|

|

|

|

$ |

63,000 |

$64,000 |

$ |

8,000 |

|

|

|

|

|

$ |

53,000 |

$54,000 |

$ |

3,000 |

|

|

|

|

|

$ |

64,000 |

$65,000 |

$ |

7,000 |

|

|

|

|

|

$ |

54,000 |

$55,000 |

$ |

2,000 |

|

|

|

|

|

$ |

65,000 |

$66,000 |

$ |

6,000 |

|

|

|

|

|

$ |

55,000 |

$56,000 |

$ |

1,000 |

|

|

|

|

|

$ |

66,000 |

$67,000 |

$ |

5,000 |

|

|

|

|

|

$ |

56,000 |

and up |

$ |

0 |

|

|

|

|

|

$ |

67,000 |

$68,000 |

$ |

4,000 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

$ |

68,000 |

$69,000 |

$ |

3,000 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

$ |

69,000 |

$70,000 |

$ |

2,000 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

$ |

70,000 |

$71,000 |

$ |

01,000 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

$ |

71,000 |

and up |

$ |

,00000 |

|

|

|

|

|

|

|

|

|

|

*** Form

Table B - Tax Calculation for 2013 Taxable Year

Use the filing status you expect to report on your 2013 tax return. This initial tax calculation does not include personal tax credits, 3% tax rate

Single or Filing Separately - If the amount on the Tax Calculation Schedule, Line 3 is:

Less than or equal to: |

$ 10,000 |

3.00% |

|

|

||

More than $10,000, but less than or equal to |

$ 50,000 |

$300 plus 5.0% of the excess over $10,000 |

||||

More than $50,000, but less than or equal to |

$100,000 |

$2,300 plus 5.5% of the excess over $50,000 |

||||

More than $100,000, but less than or equal to |

$200,000 |

$5,050 plus 6.0% of the excess over $100,000 |

||||

More than $200,000, but less than or equal to |

$250,000 |

$11,050 plus 6.5% of the excess over $200,000 |

||||

More than $250,000 |

|

|

$14,300 plus 6.7% of the excess over $250,000 |

|||

|

|

|

|

|

||

|

Single or Filing Separately Examples: |

|

|

|||

Line 3 is $13,000, Line 4 is $450 |

|

|

|

Line 3 is $525,000, Line 4 is $32,725 |

|

|

$13,000 - $10,000 |

= |

$3,000 |

|

$525,000 - $250,000 |

= |

$275,000 |

$3,000 X .05 |

= |

$150 |

|

$275,000 x .067 |

= |

$18,425 |

$300 + $150 |

= |

$450 |

|

$14,300 + $18,425 |

= |

$32,725 |

Filing Jointly/Qualifying Widow(er) - If the amount on the Tax Calculation Schedule, Line 3 is: |

|

|

||||

Less than or equal to: |

$ 20,000 |

3.00% |

|

|

||

More than $20,000, but less than or equal to |

$100,000 |

$600 plus 5.0% of the excess over $20,000 |

||||

More than $100,000, but less than or equal to |

$200,000 |

$4,600 plus 5.5% of the excess over $100,000 |

||||

More than $200,000, but less than or equal to |

$400,000 |

$10,100 plus 6.0% of the excess over $200,000 |

||||

More than $400,000, but less than or equal to |

$500,000 |

$22,100 plus 6.5% of the excess over $400,000 |

||||

More than $500,000 |

|

|

$28,600 plus 6.7% of the excess over $500,000 |

|||

|

|

|

|

|

||

|

Filing Jointly/Qualifying Widow(er) Examples: |

|

|

|||

Line 3 is $22,500, Line 4 is $725 |

|

|

|

Line 3 is $1,100,000, Line 4 is $68,800 |

|

|

$22,500 - $20,000 |

= |

$2,500 |

|

$1,100,000 - $500,000 |

= |

$600,000 |

$2,500 x .05 |

= |

$125 |

|

$600,000 x .067 |

= |

$40,200 |

$600 + $125 |

= |

$725 |

|

$28,600 + $40,200 |

= |

$68,800 |

Head of Household - If the amount on the Tax Calculation Schedule, Line 3 is: |

|

|

||||

Less than or equal to: |

$ 16,000 |

3.00% |

|

|

||

More than $16,000, but less than or equal to |

$ 80,000 |

$480 plus 5.0% of the excess over $16,000 |

||||

More than $80,000, but less than or equal to |

$160,000 |

$3,680 plus 5.5% of the excess over $80,000 |

||||

More than $160,000, but less than or equal to |

$320,000 |

$8,080 plus 6.0% of the excess over $160,000 |

||||

More than $320,000, but less than or equal to |

$400,000 |

$17,680 plus 6.5% of the excess over $320,000 |

||||

More than $400,000 |

|

|

$22,880 plus 6.7% of the excess over $400,000 |

|||

|

|

|

|

|

|

|

|

|

Head of Household Examples: |

|

|

||

Line 3 is $20,000, Line 4 is $680 |

|

|

|

Line 3 is $825,000, Line 4 is $51,355 |

|

|

$20,000 - $16,000 |

= |

$4,000 |

|

$825,000 - $400,000 |

= |

$425,000 |

$4,000 x .05 |

= |

$200 |

|

$425,000 x .067 |

= |

$28,475 |

$480 + $200 |

= |

$680 |

|

$22,880 + $28,475 |

= |

$51,355 |

*Form

Page 4 of 6

Table C - 3% Tax Rate

Use the filing status you expect to report on your 2013 tax return and your Connecticut AGI * (Tax Calculation Schedule, Line 1) to determine your

|

|

Single |

|

|

|

Filing Jointly or |

|

|

|

Filing Separately |

|

Head of Household |

|||||||||||

|

|

|

|

|

Qualified Widow(er) |

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

Connecticut AGI* |

|

3% |

Connecticut AGI* |

|

3% |

Connecticut AGI* |

3% |

Connecticut AGI* |

|

3% |

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

More Than |

Less Than |

|

More Than |

Less Than |

|

More Than |

Less Than |

More Than |

Less Than |

|

|||||||||||||

|

|

or Equal To |

|

|

|

or Equal To |

|

|

|

|

or Equal To |

|

|

or Equal To |

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

$ |

0 |

$ 56,500 |

|

$ |

0 |

$ |

0 |

$100,500 |

$ |

0 |

$ |

0 |

$50,250 |

$ |

0 |

$ |

0 |

$ 78,500 |

|

$ |

0 |

||

$ |

56,500 |

$ 61,500 |

|

$ |

20 |

$100,500 |

$105,500 |

$ |

40 |

$ |

50,250 |

$52,750 |

$ |

20 |

$ |

78,500 |

$ 82,500 |

|

$ |

32 |

|||

$ |

61,500 |

$ 66,500 |

|

$ |

40 |

$105,500 |

$110,500 |

$ |

80 |

$ |

52,750 |

$55,250 |

$ |

40 |

$ |

82,500 |

$ 86,500 |

|

$ |

64 |

|||

$ |

66,500 |

$ 71,500 |

|

$ |

60 |

$110,500 |

$115,500 |

$ |

120 |

$ |

55,250 |

$57,750 |

$ |

60 |

$ |

86,500 |

$ 90,500 |

|

$ |

96 |

|||

$ |

71,500 |

$ 76,500 |

|

$ |

80 |

$115,500 |

$120,500 |

$ |

160 |

$ |

57,750 |

$60,250 |

$ |

80 |

$ |

90,500 |

$ 94,500 |

|

$ |

128 |

|||

$ |

76,500 |

$ 81,500 |

|

$ |

100 |

$120,500 |

$125,500 |

$ |

200 |

$ |

60,250 |

$62,750 |

$ |

100 |

$ |

94,500 |

$ 98,500 |

|

$ |

160 |

|||

$ |

81,500 |

$ 86,500 |

|

$ |

120 |

$125,500 |

$130,500 |

$ |

240 |

$ |

62,750 |

$65,250 |

$ |

120 |

$ |

98,500 |

$102,500 |

$ |

192 |

||||

$ |

86,500 |

$ 91,500 |

|

$ |

140 |

$130,500 |

$135,500 |

$ |

280 |

$ |

65,250 |

$67,750 |

$ |

140 |

$102,500 |

$106,500 |

$ |

224 |

|||||

$ |

91,500 |

$ 96,500 |

|

$ |

160 |

$135,500 |

$140,500 |

$ |

320 |

$ |

67,750 |

$70,250 |

$ |

160 |

$106,500 |

$110,500 |

$ |

256 |

|||||

$ |

96,500 |

$101,500 |

$ |

180 |

$140,500 |

$145,500 |

$ |

360 |

$ |

70,250 |

$72,750 |

$ |

180 |

$110,500 |

$114,500 |

$ |

288 |

||||||

$101,500 |

and up |

$ |

200 |

$145,500 |

and up |

$ |

400 |

$ |

72,750 |

|

and up |

$ |

200 |

$114,500 |

and up |

$ |

320 |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

*Form

Table D - Tax Recapture

Use the filing status you expect to report on your 2013 tax return and your Connecticut AGI * (Tax Calculation Schedule, Line 1) to determine your recapture amount.

|

Single or Filing Separately |

|

Filing Jointly or |

|

|

|

Head of Household |

|

|||||||

|

Qualified Widow(er) |

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

Connecticut AGI* |

Recapture |

Connecticut AGI* |

|

Recapture |

Connecticut AGI* |

Recapture |

||||||||

More Than |

Less Than |

Amount |

More Than |

|

Less Than |

|

Amount |

More Than |

|

Less Than |

Amount |

||||

|

|

or Equal To |

|

|

|

|

or Equal To |

|

|

|

|

|

or Equal To |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

$ |

0 |

$200,000 |

$ |

0 |

$ 0 |

$400,000 |

|

$ |

0 |

$ 0 |

$320,000 |

$ |

0 |

||

$ |

200,000 |

$205,000 |

$ |

75 |

$400,000 |

$410,000 |

|

$ |

150 |

$320,000 |

$328,000 |

$ |

120 |

||

$ |

205,000 |

$210,000 |

$ |

150 |

$410,000 |

$420,000 |

|

$ |

300 |

$328,000 |

$336,000 |

$ |

240 |

||

$ |

210,000 |

$215,000 |

$ |

225 |

$420,000 |

$430,000 |

|

$ |

450 |

$336,000 |

$344,000 |

$ |

360 |

||

$ |

215,000 |

$220,000 |

$ |

300 |

$430,000 |

$440,000 |

|

$ |

600 |

$344,000 |

$352,000 |

$ |

480 |

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

$ |

220,000 |

$225,000 |

$ |

375 |

$440,000 |

$450,000 |

|

$ |

750 |

$352,000 |

$360,000 |

$ |

600 |

||

$ |

225,000 |

$230,000 |

$ |

450 |

$450,000 |

$460,000 |

|

$ |

900 |

$360,000 |

$368,000 |

$ |

720 |

||

$ |

230,000 |

$235,000 |

$ |

525 |

$460,000 |

$470,000 |

|

$ |

1,050 |

$368,000 |

$376,000 |

$ |

840 |

||

$ |

235,000 |

$240,000 |

$ |

600 |

$470,000 |

$480,000 |

|

$ |

1,200 |

$376,000 |

$384,000 |

$ |

960 |

||

$ |

240,000 |

$245,000 |

$ |

675 |

$480,000 |

$490,000 |

|

$ |

1,350 |

$384,000 |

$392,000 |

$ |

1,080 |

||

$ |

245,000 |

$250,000 |

$ |

750 |

$490,000 |

$500,000 |

|

$ |

1,500 |

$392,000 |

$400,000 |

$ |

1,200 |

||

$ |

250,000 |

$255,000 |

$ |

825 |

$500,000 |

$510,000 |

|

$ |

1,650 |

$400,000 |

$408,000 |

$ |

1,320 |

||

$ |

255,000 |

$260,000 |

$ |

900 |

$510,000 |

$520,000 |

|

$ |

1,800 |

$408,000 |

$416,000 |

$ |

1,440 |

||

$ |

260,000 |

$265,000 |

$ |

975 |

$520,000 |

$530,000 |

|

$ |

1,950 |

$416,000 |

$424,000 |

$ |

1,560 |

||

$ |

265,000 |

$270,000 |

$ |

1,050 |

$530,000 |

$540,000 |

|

$ |

2,100 |

$424,000 |

$432,000 |

$ |

1,680 |

||

$ |

270,000 |

$275,000 |

$ |

1,125 |

$540,000 |

$550,000 |

|

$ |

2,250 |

$432,000 |

$440,000 |

$ |

1,800 |

||

$ |

275,000 |

$280,000 |

$ |

1,200 |

$550,000 |

$560,000 |

|

$ |

2,400 |

$440,000 |

$448,000 |

$ |

1,920 |

||

$ |

280,000 |

$285,000 |

$ |

1,275 |

$560,000 |

$570,000 |

|

$ |

2,550 |

$448,000 |

$456,000 |

$ |

2,040 |

||

$ |

285,000 |

$290,000 |

$ |

1,350 |

$570,000 |

$580,000 |

|

$ |

2,700 |

$456,000 |

$464,000 |

$ |

2,160 |

||

$ |

290,000 |

$295,000 |

$ |

1,425 |

$580,000 |

$590,000 |

|

$ |

2,850 |

$464,000 |

$472,000 |

$ |

2,280 |

||

$ |

295,000 |

$300,000 |

$ |

1,500 |

$590,000 |

$600,000 |

|

$ |

3,000 |

$472,000 |

$480,000 |

$ |

2,400 |

||

$ |

300,000 |

$305,000 |

$ |

1,575 |

$600,000 |

$610,000 |

|

$ |

3,150 |

$480,000 |

$488,000 |

$ |

2,520 |

||

$ |

305,000 |

$310,000 |

$ |

1,650 |

$610,000 |

$620,000 |

|

$ |

3,300 |

$488,000 |

$496,000 |

$ |

2,640 |

||

$ |

310,000 |

$315,000 |

$ |

1,725 |

$620,000 |

$630,000 |

|

$ |

3,450 |

$496,000 |

$504,000 |

$ |

2,760 |

||

$ |

315,000 |

$320,000 |

$ |

1,800 |

$630,000 |

$640,000 |

|

$ |

3,600 |

$504,000 |

$512,000 |

$ |

2,880 |

||

$ |

320,000 |

$325,000 |

$ |

1,875 |

$640,000 |

$650,000 |

|

$ |

3,750 |

$512,000 |

$520,000 |

$ |

3,000 |

||

$ |

325,000 |

$330,000 |

$ |

1,950 |

$650,000 |

$660,000 |

|

$ |

3,900 |

$520,000 |

$528,000 |

$ |

3,120 |

||

$ |

330,000 |

$335,000 |

$ |

2,025 |

$660,000 |

$670,000 |

|

$ |

4,050 |

$528,000 |

$536,000 |

$ |

3,240 |

||

$ |

335,000 |

$340,000 |

$ |

2,100 |

$670,000 |

$680,000 |

|

$ |

4,200 |

$536,000 |

$544,000 |

$ |

3,360 |

||

$ |

340,000 |

$345,000 |

$ |

2,175 |

$680,000 |

$690,000 |

|

$ |

4,350 |

$544,000 |

$552,000 |

$ |

3,480 |

||

$ |

345,000 |

and up |

$ |

2,250 |

$690,000 |

|

and up |

$ |

4,500 |

$552,000 |

|

and up |

$ |

3,600 |

|

2013 Form

Page 5 of 6

Table E - Personal Tax Credits for 2013 Taxable Year

Use the filing status you expect to report on your 2013 tax return and your Connecticut AGI * (Tax Calculation Schedule, Line 1) to determine your decimal amount.

|

Single |

|

Filing Jointly or |

Filing Separately |

Head of Household |

||||||

|

|

Qualified Widow(er) |

|||||||||

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

Connecticut AGI* |

Decimal |

Connecticut AGI* |

Decimal |

Connecticut AGI* |

Decimal |

Connecticut AGI* |

Decimal |

||||

|

|

|

|

|

|

|

|

||||

More Than |

Less Than |

Amount |

More Than |

Less Than |

Amount |

More Than |

Less Than |

Amount |

More Than |

Less Than |

Amount |

|

or Equal To |

|

|

or Equal To |

|

|

or Equal To |

|

|

or Equal To |

|

$14,000 |

$17,500 |

.75 |

$24,000 |

$30,000 |

.75 |

$12,000 |

$15,000 |

.75 |

$19,000 |

$24,000 |

.75 |

$17,500 |

$18,000 |

.70 |

$30,000 |

$30,500 |

.70 |

$15,000 |

$15,500 |

.70 |

$24,000 |

$24,500 |

.70 |

$18,000 |

$18,500 |

.65 |

$30,500 |

$31,000 |

.65 |

$15,500 |

$16,000 |

.65 |

$24,500 |

$25,000 |

.65 |

$18,500 |

$19,000 |

.60 |

$31,000 |

$31,500 |

.60 |

$16,000 |

$16,500 |

.60 |

$25,000 |

$25,500 |

.60 |

$19,000 |

$19,500 |

.55 |

$31,500 |

$32,000 |

.55 |

$16,500 |

$17,000 |

.55 |

$25,500 |

$26,000 |

.55 |

$19,500 |

$20,000 |

.50 |

$32,000 |

$32,500 |

.50 |

$17,000 |

$17,500 |

.50 |

$26,000 |

$26,500 |

.50 |

$20,000 |

$20,500 |

.45 |

$32,500 |

$33,000 |

.45 |

$17,500 |

$18,000 |

.45 |

$26,500 |

$27,000 |

.45 |

$20,500 |

$21,000 |

.40 |

$33,000 |

$33,500 |

.40 |

$18,000 |

$18,500 |

.40 |

$27,000 |

$27,500 |

.40 |

$21,000 |

$23,300 |

.35 |

$33,500 |

$40,000 |

.35 |

$18,500 |

$20,000 |

.35 |

$27,500 |

$34,000 |

.35 |

$23,300 |

$23,800 |

.30 |

$40,000 |

$40,500 |

.30 |

$20,000 |

$20,500 |

.30 |

$34,000 |

$34,500 |

.30 |

$23,800 |

$24,300 |

.25 |

$40,500 |

$41,000 |

.25 |

$20,500 |

$21,000 |

.25 |

$34,500 |

$35,000 |

.25 |

$24,300 |

$24,800 |

.20 |

$41,000 |

$41,500 |

.20 |

$21,000 |

$21,500 |

.20 |

$35,000 |

$35,500 |

.20 |

$24,800 |

$29,200 |

.15 |

$41,500 |

$50,000 |

.15 |

$21,500 |

$25,000 |

.15 |

$35,500 |

$44,000 |

.15 |

$29,200 |

$29,700 |

.14 |

$50,000 |

$50,500 |

.14 |

$25,000 |

$25,500 |

.14 |

$44,000 |

$44,500 |

.14 |

$29,700 |

$30,200 |

.13 |

$50,500 |

$51,000 |

.13 |

$25,500 |

$26,000 |

.13 |

$44,500 |

$45,000 |

.13 |

$30,200 |

$30,700 |

.12 |

$51,000 |

$51,500 |

.12 |

$26,000 |

$26,500 |

.12 |

$45,000 |

$45,500 |

.12 |

$30,700 |

$31,200 |

.11 |

$51,500 |

$52,000 |

.11 |

$26,500 |

$27,000 |

.11 |

$45,500 |

$46,000 |

.11 |

$31,200 |

$56,000 |

.10 |

$52,000 |

$96,000 |

.10 |

$27,000 |

$48,000 |

.10 |

$46,000 |

$74,000 |

.10 |

$56,000 |

$56,500 |

.09 |

$96,000 |

$96,500 |

.09 |

$48,000 |

$48,500 |

.09 |

$74,000 |

$74,500 |

.09 |

$56,500 |

$57,000 |

.08 |

$96,500 |

$97,000 |

.08 |

$48,500 |

$49,000 |

.08 |

$74,500 |

$75,000 |

.08 |

$57,000 |

$57,500 |

.07 |

$97,000 |

$97,500 |

.07 |

$49,000 |

$49,500 |

.07 |

$75,000 |

$75,500 |

.07 |

$57,500 |

$58,000 |

.06 |

$97,500 |

$98,000 |

.06 |

$49,500 |

$50,000 |

.06 |

$75,500 |

$76,000 |

.06 |

$58,000 |

$58,500 |

.05 |

$98,000 |

$98,500 |

.05 |

$50,000 |

$50,500 |

.05 |

$76,000 |

$76,500 |

.05 |

$58,500 |

$59,000 |

.04 |

$98,500 |

$99,000 |

.04 |

$50,500 |

$51,000 |

.04 |

$76,500 |

$77,000 |

.04 |

$59,000 |

$59,500 |

.03 |

$99,000 |

$99,500 |

.03 |

$51,000 |

$51,500 |

.03 |

$77,000 |

$77,500 |

.03 |

$59,500 |

$60,000 |

.02 |

$99,500 |

$100,000 |

.02 |

$51,500 |

$52,000 |

.02 |

$77,500 |

$78,000 |

.02 |

$60,000 |

$60,500 |

.01 |

$100,000 |

$100,500 |

.01 |

$52,000 |

$52,500 |

.01 |

$78,000 |

$78,500 |

.01 |

$60,500 |

and up |

.00 |

$100,500 |

and up |

.00 |

$52,500 |

and up |

.00 |

$78,500 |

and up |

.00 |

*Form

2013 Form

Page 6 of 6