General Instructions

Section references are to the Internal Revenue Code unless otherwise noted.

Note: This form is open to public inspection.

Future Developments

For the latest information about developments related to Form 5578 and its instructions, such as legislation enacted after they were published, go to www.irs.gov/Form5578.

What’s New

Rev. Proc. 2019-22; 2019-22 C.B. 1260, available at www.irs.gov/irb/2019-22_IRB, modified Rev. Proc. 75-50; 1975-2 C.B. 587, available at www.irs.gov/pub/irs-tege/ rp1975-50.pdf, to provide a third method for a private school to satisfy the publicity requirement in section 4.03. In general, an organization will meet the requirement if the organization has publicized its racially nondiscriminatory policy on its primary publicly accessible Internet homepage at all times during its taxable year in a manner reasonably expected to be noticed by visitors on the homepage. See paragraph 1(c) under “Section 4.03, Publicity” below for more details.

Purpose of Form

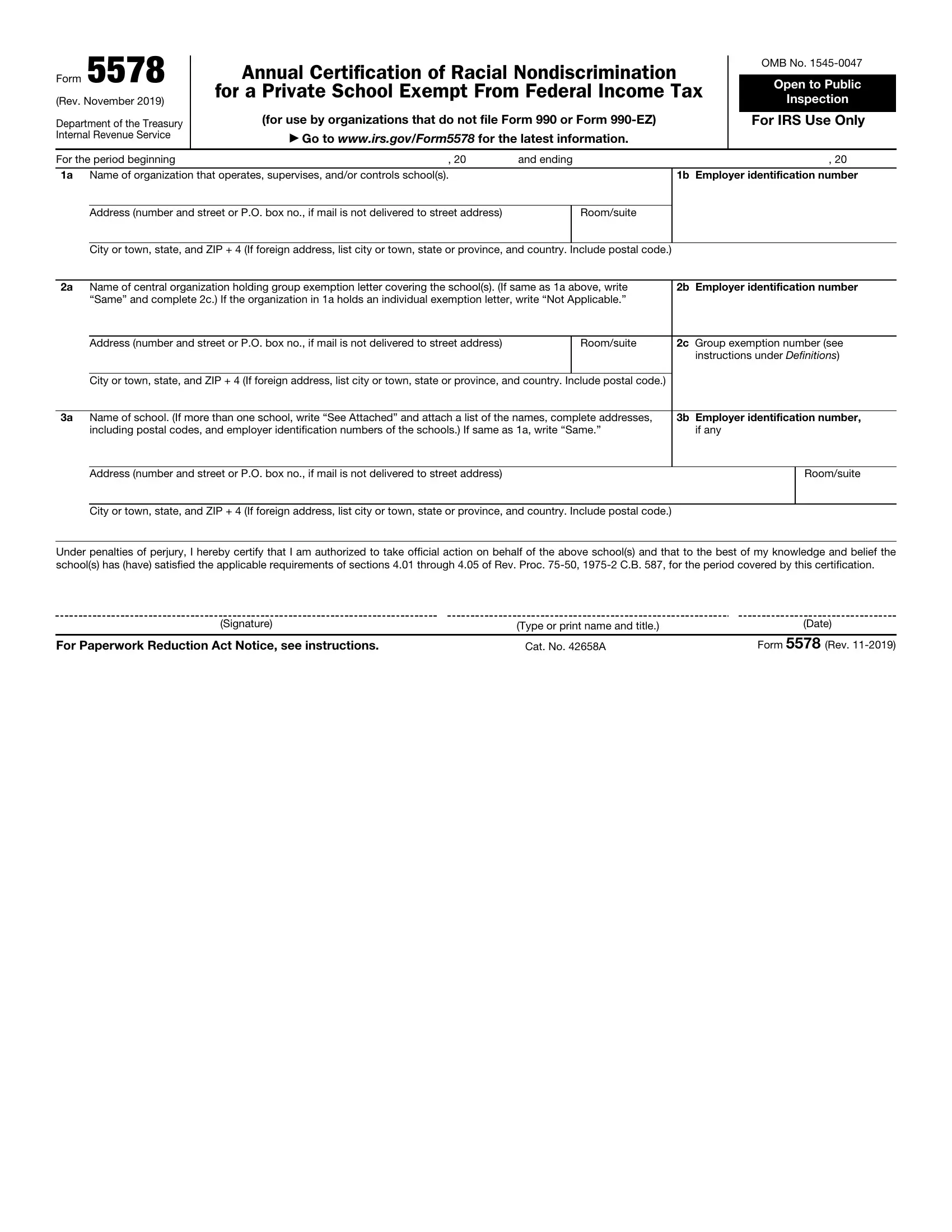

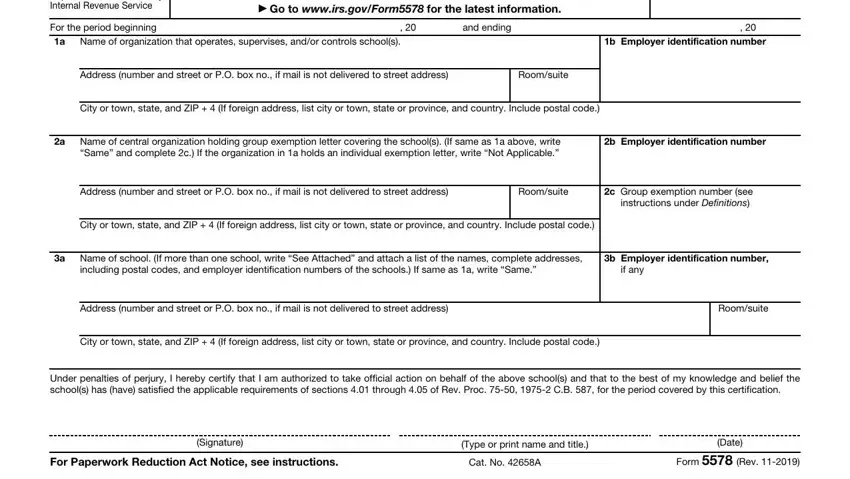

Form 5578 may be used by organizations that operate tax-exempt private schools to provide the Internal Revenue Service with the annual certification of racial nondiscrimination required by Rev. Proc.

75-50 (the relevant part of which is reproduced in these instructions). Rev. Proc. 2019-22 modified Rev. Proc. 75-50 to provide a third method for a private school to satisfy the requirement in Section 4.03.

Who Must File

Every organization that claims exemption from federal income tax under section 501(c)(3) of the Internal Revenue Code and that operates, supervises, or controls a private school(s) must file a certification of racial nondiscrimination. If an organization is required to file Form 990, Return of Organization Exempt From Income Tax, or Form 990-EZ, Short Form Return of Organization Exempt From Income Tax, either as a separate return or as part of a group return, the certification must be made on Schedule E (Form 990 or 990-EZ), Schools, rather than on this form.

An authorized official of a central organization may file one form to certify for the school activities of subordinate organizations that would otherwise be required to file on an individual basis, but only if the central organization has enough control over the schools listed on the form to ensure that the schools maintain a racially nondiscriminatory policy as to students.

Definitions

A racially nondiscriminatory policy as to students means that the school admits the students of any race to all the rights,

privileges, programs, and activities generally accorded or made available to students at that school and that the school does not discriminate on the basis of race in the administration of its educational policies, admissions policies, scholarship and loan programs, and athletic and other school-administered programs.

The IRS considers discrimination on the basis of race to include discrimination on the basis of color or national or ethnic origin.

A school is an educational organization that normally maintains a regular faculty and curriculum and normally has a regularly enrolled body of pupils or students in attendance at the place where its educational activities are regularly carried on. The term includes primary, secondary, preparatory, or high schools and colleges and universities, whether operated as a separate legal entity or as an activity of a church or other organization described in section 501(c)(3). The term also includes preschools and any other organization that is a school as defined in section 170(b)(1)(A)(ii).

A central organization is an organization that has one or more subordinates under its general supervision or control. A subordinate is a chapter, local, post, or other unit of a central organization. A central organization may also be a subordinate, as in the case of a state organization that has subordinate units and is itself affiliated with a national organization.

The group exemption number (GEN) is a four-digit number issued to a central organization by the IRS. It identifies a central organization that has received a ruling from the IRS recognizing on a group basis the exemption from federal income tax of the central organization and its covered subordinates.

When To File

Under Rev. Proc. 75-50, a certification of racial nondiscrimination must be filed annually by the 15th day of the 5th month after the organization’s accounting period ends (May 15th for a calendar-year filer). If the due date falls on a Saturday, Sunday, or legal holiday, file on the next business day. A business day is any day that isn’t a Saturday, Sunday, or legal holiday.

Where To File

Mail Form 5578 to:

Department of the Treasury

Internal Revenue Service Center

Ogden, UT 84201-0027

Certification Requirement

Section 4.06 of Rev. Proc. 75-50 requires an individual authorized to take official action on behalf of a school that claims to be racially nondiscriminatory as to students to certify annually, under penalties of perjury, that to the best of his or her knowledge and belief the school has satisfied the applicable requirements of sections 4.01 through 4.05 of the Revenue Procedure, reproduced below:

Rev. Proc. 75-50

Section 4.01, Organizational Requirements. A school must include a statement in its charter, bylaws, or other governing instrument, or in a resolution of its governing body, that it has a racially nondiscriminatory policy as to students and therefore does not discriminate against applicants and students on the basis of race, color, and national or ethnic origin.

Section 4.02, Statement of Policy. Every school must include a statement of its racially nondiscriminatory policy as to students in all its brochures and catalogues dealing with student admissions, programs, and scholarships. A statement substantially similar to the Notice described in paragraph (a) of subsection 1 of section 4.03, infra, will be acceptable for this purpose. Further, every school must include a reference to its racially nondiscriminatory policy in other written advertising that it uses as a means of informing prospective students of its programs. The following references will be acceptable:

The (name) school admits students of

any race, color, and national or ethnic origin.

Section 4.03, Publicity. The school must make its racially nondiscriminatory policy known to all segments of the general community served by the school.

1.The school must use one of the following three methods to satisfy this requirement:

(a)The school may publish a notice of its racially nondiscriminatory policy in a newspaper of general circulation that serves all racial segments of the community. This publication must be repeated at least once annually during the period of the school’s solicitation for students or, in the absence of a solicitation program, during the school’s registration period. Where more than one community is served by a school, the school may publish its notice in those newspapers that are reasonably likely to be read by all racial segments of the communities that it serves. The notice must appear in a section of the newspaper likely to be read by prospective students and their families and it must occupy at least three column inches. It must be captioned in at least 12 point boldface type as a notice of nondiscriminatory policy as to students, and its text must be printed in at least 8 point type. The following notice will be acceptable:

Notice Of Nondiscriminatory Policy As To Students

The (name) school admits students of any race, color, national, and ethnic origin to all the rights, privileges, programs, and activities generally accorded or made available to students at the school. It does not discriminate on the basis of race, color, national and ethnic origin in administration of its educational policies, admissions policies, scholarship and loan programs, and athletic and other school-administered programs.