For more information, go to ftb.ca.gov and search for electronic 592-B requirements. A broker can provide Form 592-B as a composite statement. For more information, go to ftb. ca.gov and search for composite 592-B.

Do not use Form 592-B to allocate or distribute withholding to each payee, use Form 592, Form 592-PTE, or Form 592-F.

Pass-through entities withheld upon by another entity use:

•Form 592-PTE to pass through the withholding to domestic nonresident partners in a partnership, members of a limited liability company (LLC), estate or trust beneficiaries, and S corporation shareholders.

•Form 592-F to pass through the withholding to foreign (non-U.S.) partners or members.

B Helpful Hints

•Get taxpayer identification numbers (TINs) from all payees.

•Complete all applicable fields.

•Complete all forms timely to avoid penalties.

C Who Must Complete

Form 592-B must be completed by the withholding agent, including any person or entity who:

•Has withheld on payments to residents or nonresidents.

•Has withheld backup withholding on payments to residents or nonresidents.

•Was withheld upon and must pass through the withholding credit to their pass-through entity owners.

Record Keeping

The withholding agent retains the proof of withholding for a minimum of five years and must provide it to the FTB upon request.

D When To Complete

Form 592-B must be completed and provided to each payee by:

•January 31st following the close of the calendar year for residents or nonresidents.

•February 15th following the close of the calendar year for brokers as stated in Internal Revenue Code (IRC) Section 6045.

Form 592-B must be provided to each foreign (non-U.S.) partner or member by:

•The 15th day of the 3rd month following the close of the partnership's or LLC's taxable year.

•The 15th day of the 6th month following the close of the partnership's or LLC's taxable year, if all the partners in the partnership or members in the LLC are foreign.

10-Day Notification – When making a payment of withholding tax to the IRS under IRC Section 1446, a partnership must notify all foreign partners of their allocable shares of any IRC Section 1446 tax paid to the IRS

by the partnership. The partners use this information to adjust the amount of estimated tax that they must otherwise pay to the IRS. The notification to the foreign partners must be provided within 10 days of the payment due date, or, if paid later, the date the withholding payment is made. See Treas. Reg. Section 1.1446-3(d)(1)(i) for information that must be included in the notification and for exceptions to the notification requirement. For California withholding purposes, withholding agents should make a similar notification. No particular form is required for this notification, and it is commonly done on the statement accompanying the distribution or payment. However, the withholding agent may choose to report the tax withheld to the payee on a Form 592-B.

E Amending Form 592-B

If an error is discovered after the withholding agent provides Form 592-B to the payee, then the withholding agent must follow

the amending instructions for Form 592, Form 592-PTE, or Form 592-F and follow the steps below:

•Complete a new Form 592-B using the same taxable year form as originally provided to the payee.

•Check the Amended box at the top left corner of the form.

•Provide the amended copy of Form 592-B to the payee.

F Penalties

The withholding agent must furnish complete and correct copies of Form(s) 592-B to the payee by the due date.

If the withholding agent fails to provide complete, correct, and timely Form(s) 592-B to the payee, the penalty per Form 592-B is:

•Up to $270 for each payee statement not provided by the due date.

•$550 or 10% of the amount required to be reported (whichever is greater), if the failure is due to intentional disregard of the requirement.

Specific Instructions

Instructions for Withholding Agent

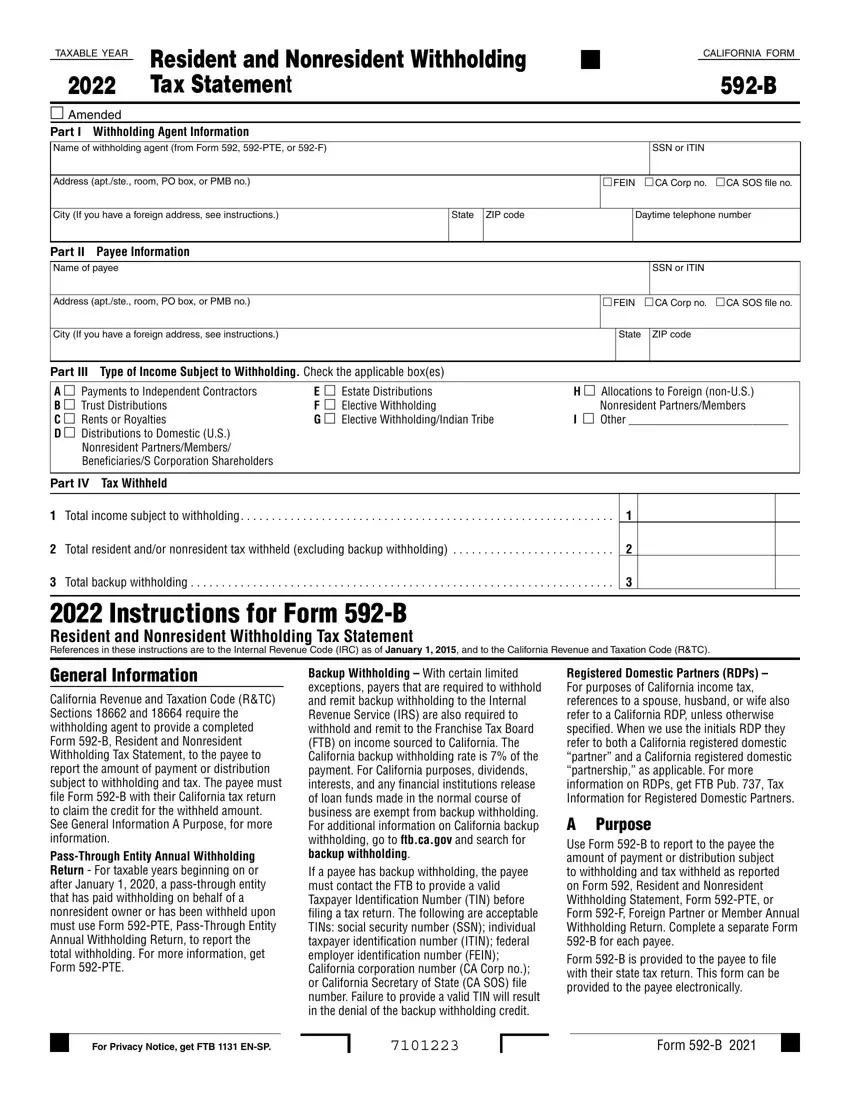

Year – The year at the top left corner of Form 592-B represents the calendar year in which the withholding took place.

For foreign partners or foreign members, match the year at the top left corner of Form 592-B to the year that the partnership’s or LLC’s taxable year ended. For example, if the partnership’s or LLC’s taxable year ended December 31, 2021, use the 2021 Form 592-B.

Private Mail Box (PMB) – Include the PMB in the address field. Write “PMB” first, then the box number. Example: 111 Main Street PMB 123.

Foreign Address – Follow the country's practice for entering the city, county, province, state, country, and postal code, as applicable, in the appropriate boxes. Do not abbreviate the country name.

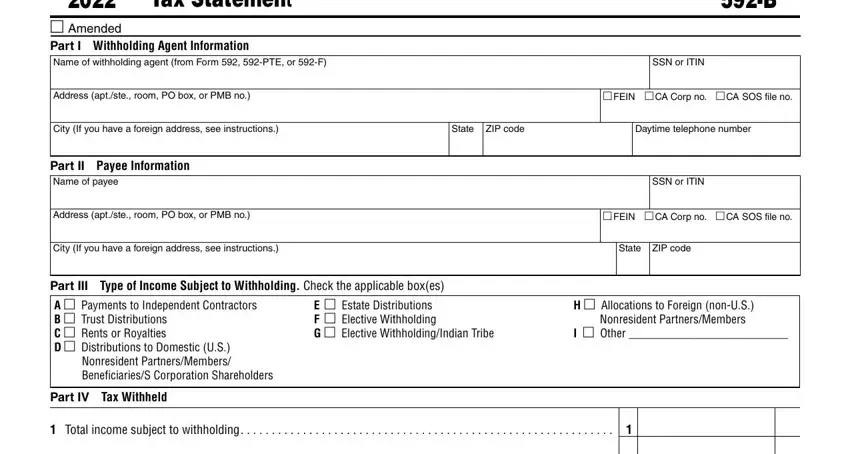

Part I – Withholding Agent Information

Enter the withholding agent’s name, TIN, address, and telephone number.

Part II – Payee Information

Enter the payee's name, TIN, and address.

If the payee is a grantor trust, enter the individual name and SSN or ITIN of the grantor that is required to file a tax return and report the income. Do not enter the name of the trust or trustee information. (For tax purposes, grantor trusts are transparent. The individual grantor must report the income and claim the withholding on the individual’s California tax return.)

If the payee is a nongrantor trust, enter the name of the trust and the trust’s FEIN. Do not enter trustee information.

If the trust has applied for a FEIN, but it has not been received, enter "applied for" in the space for the trust’s FEIN and attach a copy of the federal application to the back of Form 592-B. After the FEIN is received, amend Form 592-B to submit the assigned FEIN.

If the payees are married/RDP, enter only the name and SSN or ITIN of the primary spouse/RDP. However, if the payees intend to file separate California tax returns, the withholding agent should split the withholding and complete a separate Form 592-B for each spouse/RDP.

Part III – Type of Income Subject to Withholding

Check the box(es) for the type of income subject to withholding.

Part IV – Tax Withheld

Line 1

Enter the total income subject to withholding.

Line 2

Enter the total resident and/or nonresident tax withheld (excluding backup withholding). The amount of tax to be withheld is computed by applying a rate of 7% on items of income subject to withholding. For foreign partners, the rate is 8.84% for corporations, 10.84% for banks and financial institutions, and 12.3% for all others.

For pass-through entities, the amount withheld is allocated to partners, members, S corporation shareholders, or beneficiaries, whether they are residents or nonresidents of California, in proportion to their ownership or beneficial interest.

Line 3

Enter the total backup withholding, if applicable.