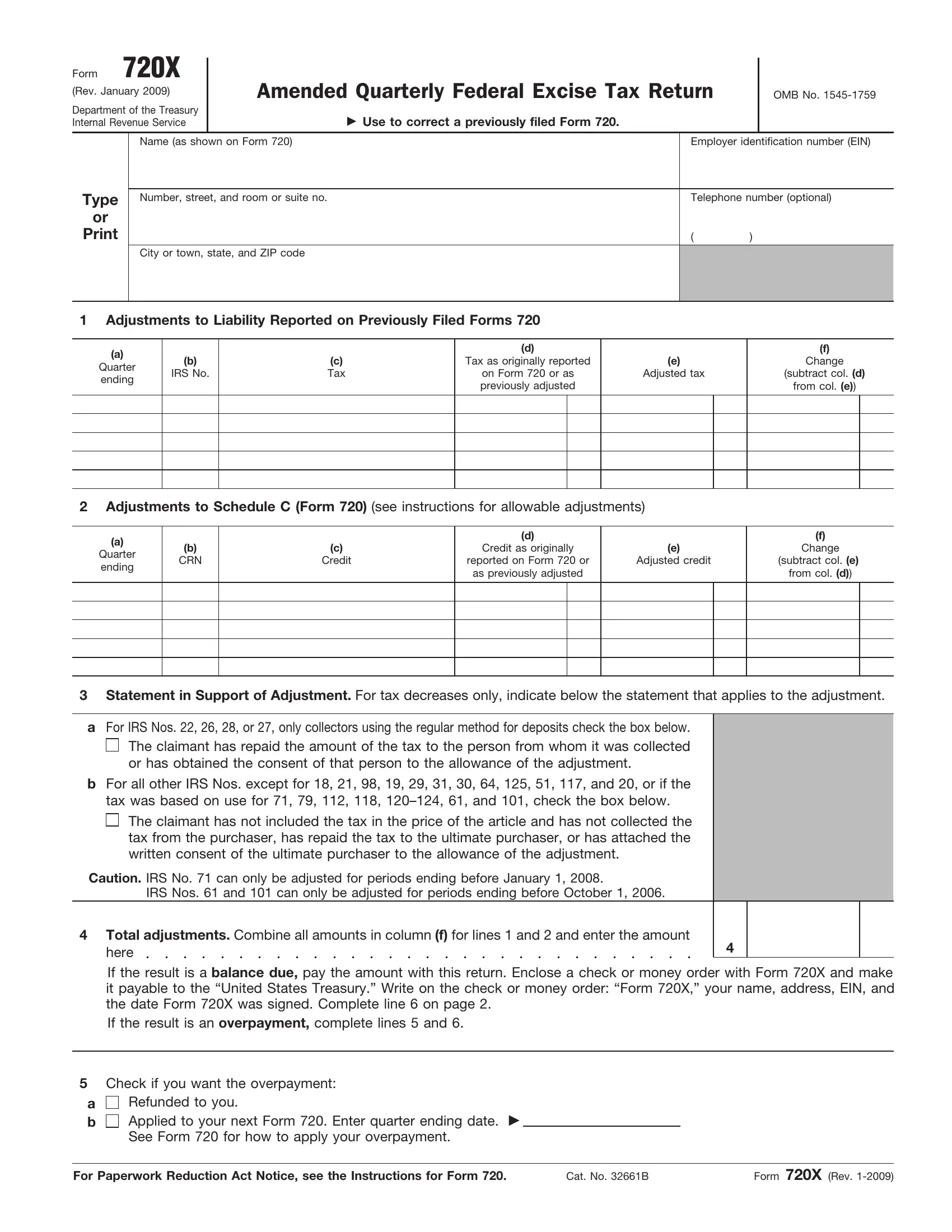

The 720X form, revised in January 2009 by the Department of the Treasury and the Internal Revenue Service, serves as a pivotal tool for entities looking to correct previously filed Form 720s, which report federal excise tax liabilities. This form is integral for making adjustments to liabilities or claims initially reported, ensuring accuracy and compliance with the United States tax code. It caters to corrections that either decrease or increase previously reported tax liabilities, facilitating a mechanism for entities to rectify past reporting errors or oversights efficiently. Taxpayers can also employ Form 720X to adjust credits related to specific excise taxes, albeit with certain restrictions, further emphasizing its role in refining tax liability assessments. Accompanied by a comprehensive set of instructions, the form demands detailed information about the adjustments being made, including quarter ending dates, original and adjusted tax or credit amounts, and pertinent IRS numbers, thereby ensuring clarity and precision in the correction process. Additionally, it provides options for how taxpayers wish to handle any resulting overpayments, whether they prefer refunds or applying these amounts towards future tax liabilities, reflecting the form's adaptability to various taxpayer needs. Integral to the process is the requirement for a declaration under penalties of perjury, underscoring the seriousness and legal implications of the information provided on the form. Through this framework, Form 720X embodies a critical corrective instrument within the federal tax system, balancing the necessity for accuracy with the practicalities of taxpayer error and compliance adjustments.

| Question | Answer |

|---|---|

| Form Name | Form 720X |

| Form Length | 3 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 45 sec |

| Other names | 720x, claimant, preparer, agri |