form 990 schedule b can be filled in with ease. Simply open FormsPal PDF editing tool to complete the job right away. Our tool is constantly evolving to provide the very best user experience achievable, and that is thanks to our commitment to constant enhancement and listening closely to comments from users. This is what you'll need to do to get started:

Step 1: Click on the "Get Form" button above. It is going to open our pdf editor so you can begin filling in your form.

Step 2: After you start the editor, you will notice the document all set to be completed. In addition to filling out various blanks, you may also perform other actions with the file, such as adding your own textual content, editing the initial textual content, inserting illustrations or photos, placing your signature to the document, and much more.

Completing this form calls for thoroughness. Ensure that every blank field is filled out properly.

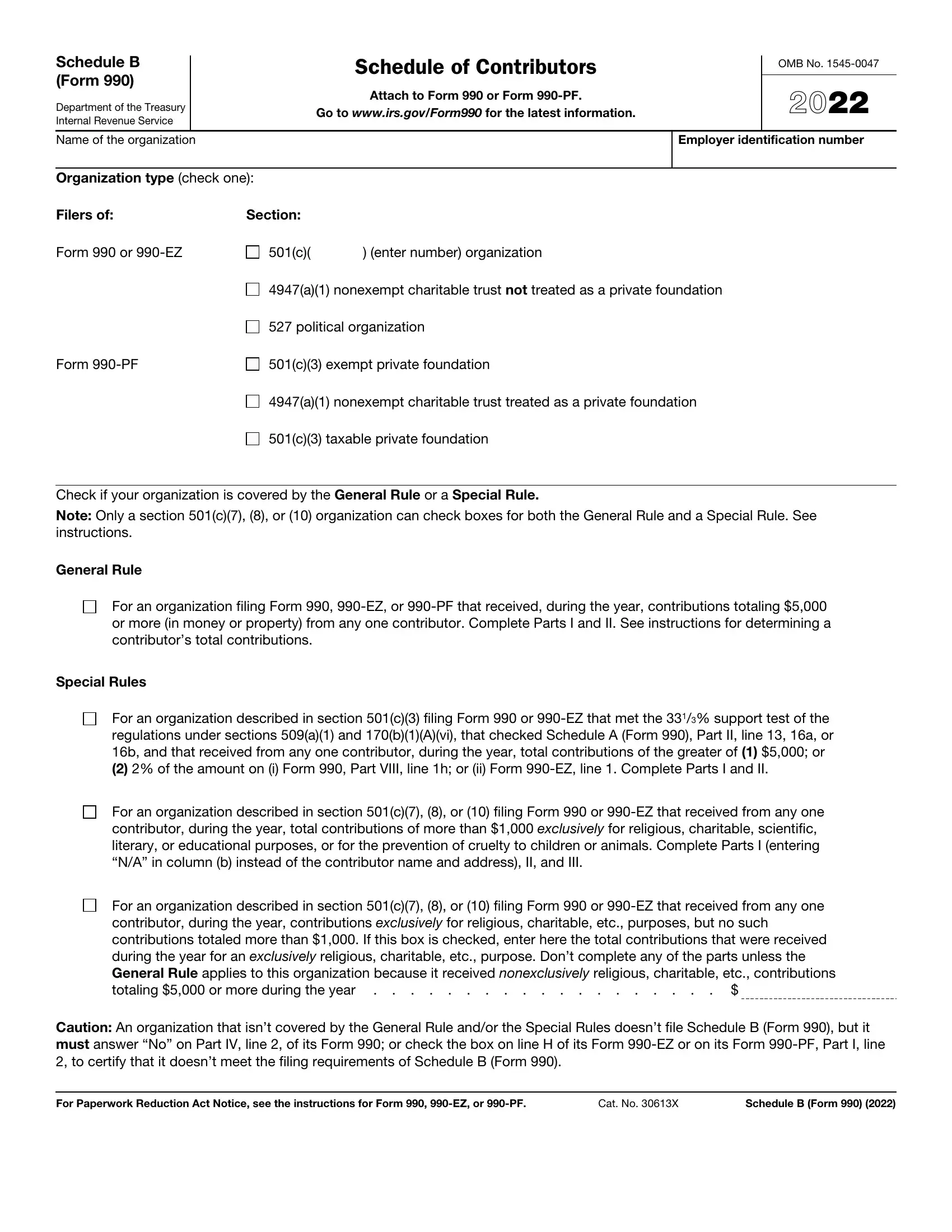

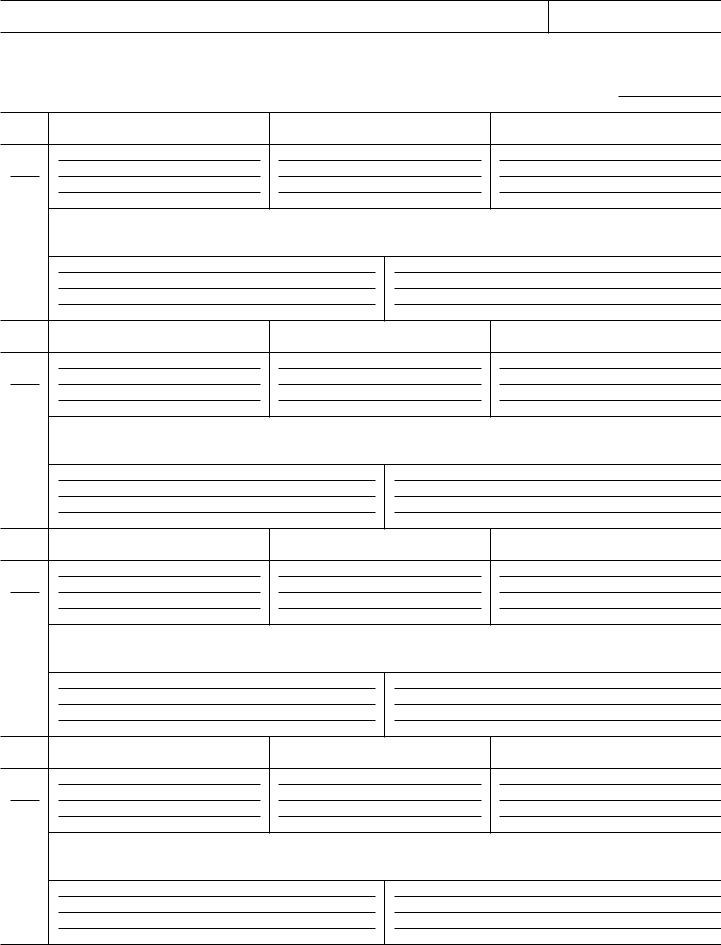

1. It's very important to fill out the form 990 schedule b properly, therefore be attentive while filling out the segments that contain all of these blanks:

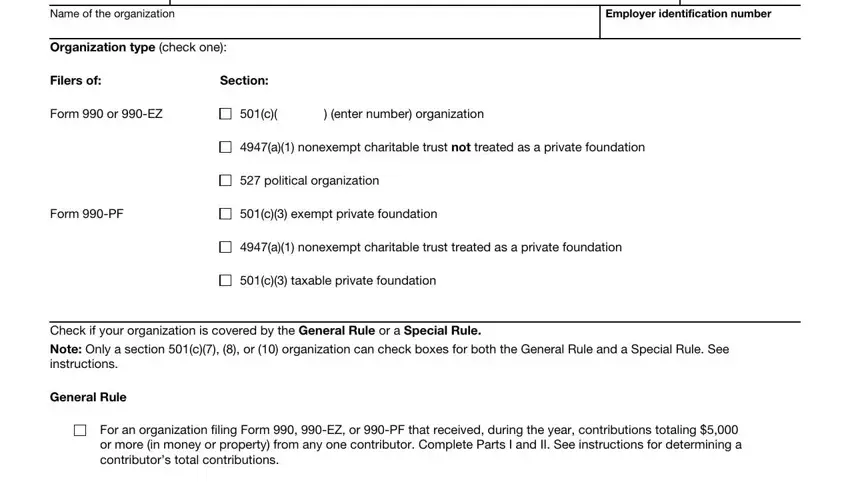

2. Now that the previous section is done, you should put in the required details in For an organization described in, For an organization described in, For an organization described in, and Caution An organization that isnt so you're able to move on to the next part.

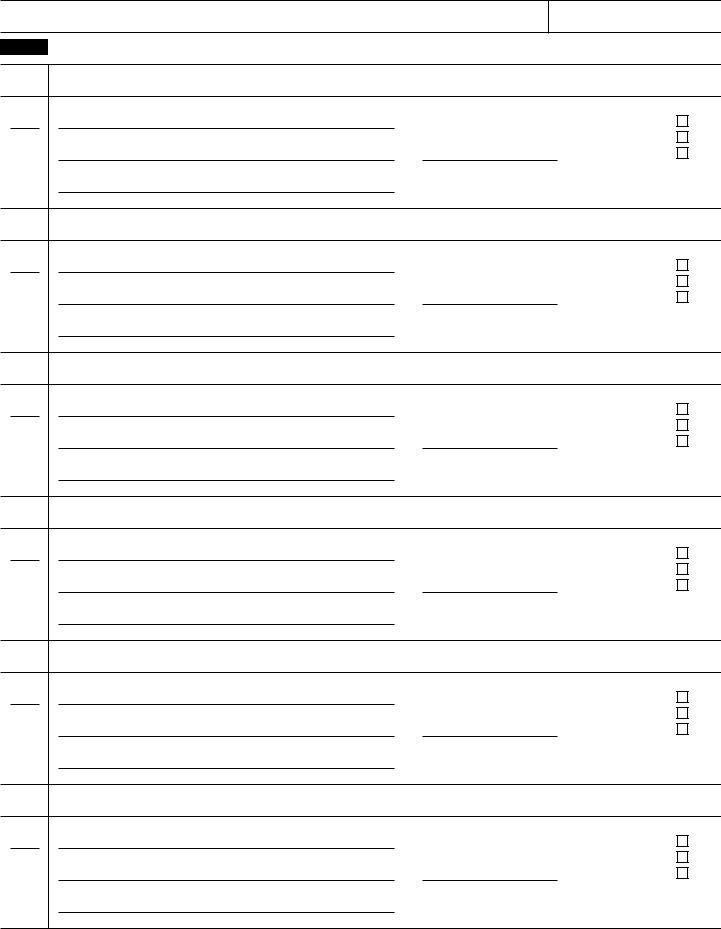

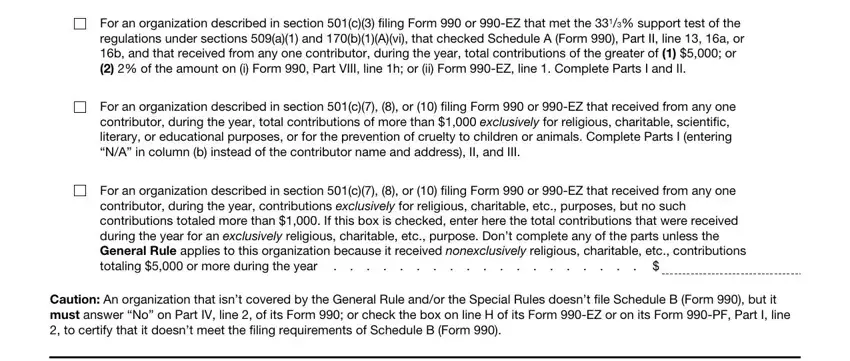

3. In this part, review Schedule B Form, Name of organization, Employer identification number, Page, Part I, Contributors see instructions Use, a No, a No, a No, Name address and ZIP, Total contributions, Type of contribution, Name address and ZIP, Name address and ZIP, and Person Payroll Noncash. All these need to be filled in with utmost precision.

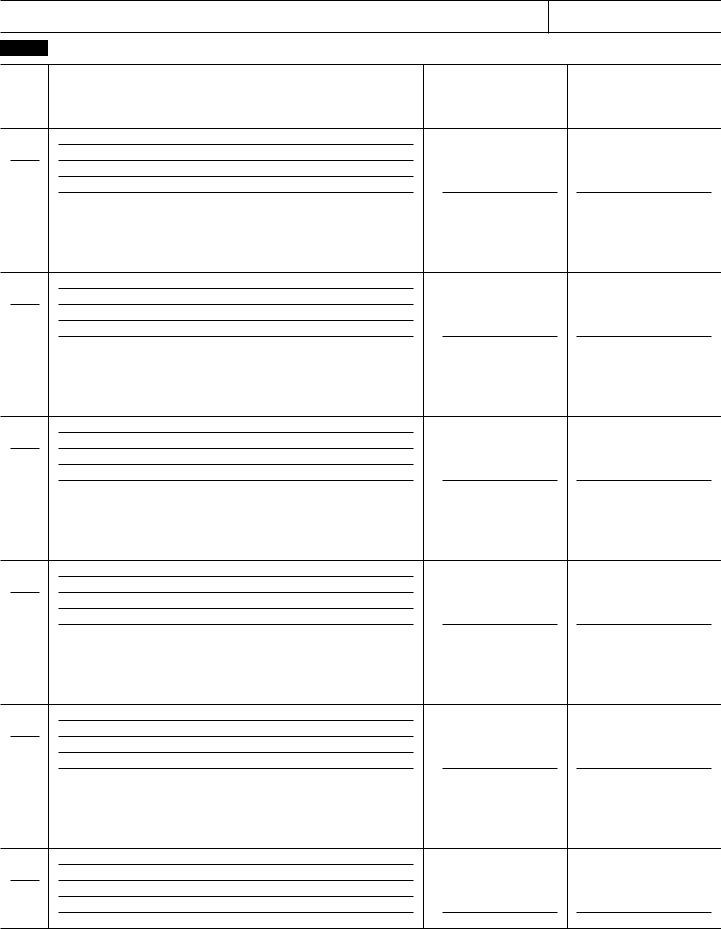

4. Completing a No, a No, a No, Name address and ZIP, Name address and ZIP, Name address and ZIP, Person Payroll Noncash, Complete Part II for noncash, Total contributions, Type of contribution, Person Payroll Noncash, Complete Part II for noncash, Total contributions, Type of contribution, and Person Payroll Noncash is essential in this fourth part - make sure to spend some time and fill out every single blank!

5. The pdf must be finalized with this particular section. Further you will see a comprehensive listing of blank fields that require accurate information in order for your form submission to be accomplished: Person Payroll Noncash, Complete Part II for noncash, and Schedule B Form.

As to Schedule B Form and Complete Part II for noncash, make sure that you get them right in this current part. Both these are certainly the most significant fields in this document.

Step 3: Just after looking through your filled out blanks, click "Done" and you are good to go! Join us today and instantly get access to form 990 schedule b, set for download. All adjustments you make are saved , meaning you can change the pdf later on when necessary. FormsPal is invested in the confidentiality of all our users; we make sure that all personal information used in our editor is kept confidential.