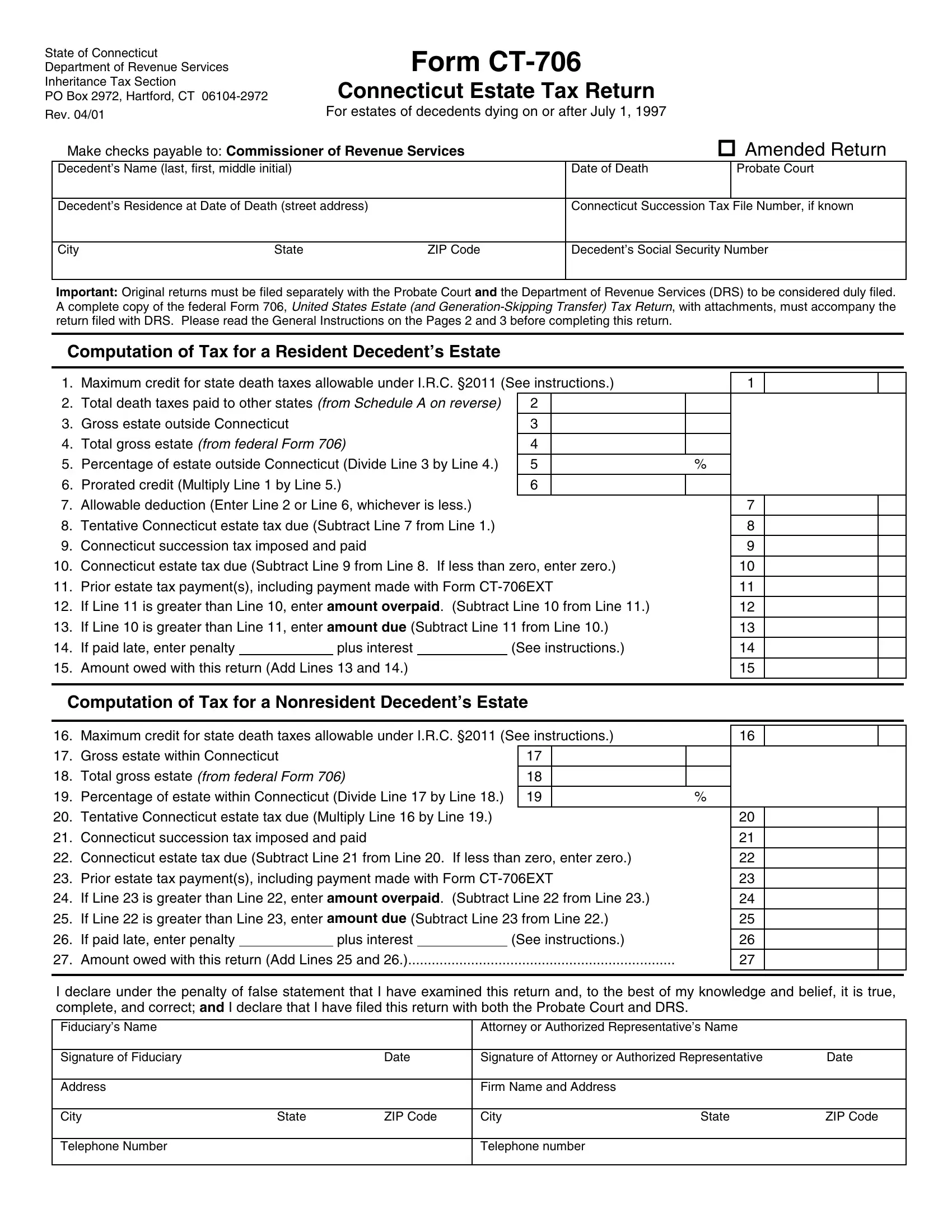

When handling the estate of a loved one who has passed away, dealing with taxes can seem overwhelming during an already difficult time. The Connecticut Estate Tax Return, Form CT-706, is a document that executors or administrators of estates need to familiarize themselves with if the deceased was a Connecticut resident or owned real or tangible personal property within Connecticut at the time of their death. This form is critical for calculating the state estate tax due, taking into account the federal estate tax parameters and any credits for taxes paid to other states or for the value of certain donated artworks. Whether dealing with a resident or nonresident decedent's estate, specific sections of the form allow for the determination of the estate's tax responsibilities, including deductions, exemptions, and potential penalties for late filings. Complete and accurate completion of Form CT-706, along with the necessary attachments and any applicable schedules for real property or taxes paid to other states, serves as the basis for ensuring that the estate is in compliance with Connecticut's estate taxation requirements. This introduction aims to provide a foundational understanding of the purpose and major components of Form CT-706, aiding executors and administrators in navigating through their tax obligations with greater confidence.

| Question | Answer |

|---|---|

| Form Name | Form Ct 706 |

| Form Length | 4 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 1 min |

| Other names | ct 706 state of ct 706 federal form 706 |

State of Connecticut |

|

Form |

|

||

Department of Revenue Services |

|

|

|||

Inheritance Tax Section |

|

Connecticut Estate Tax Return |

|

||

PO Box 2972, Hartford, CT |

|

|

|||

Rev. 04/01 |

|

For estates of decedents dying on or after July 1, 1997 |

|

||

|

Make checks payable to: Commissioner of Revenue Services |

|

Amended Return |

||

|

Decedent’s Name (last, first, middle initial) |

|

Date of Death |

Probate Court |

|

|

|

|

|

||

|

Decedent’s Residence at Date of Death (street address) |

Connecticut Succession Tax File Number, if known |

|||

|

|

|

|

|

|

|

City |

State |

ZIP Code |

Decedent’s Social Security Number |

|

|

|

|

|

|

|

Important: Original returns must be filed separately with the Probate Court and the Department of Revenue Services (DRS) to be considered duly filed. A complete copy of the federal Form 706, United States Estate (and

Computation of Tax for a Resident Decedent’s Estate

1. |

Maximum credit for state death taxes allowable under I.R.C. §2011 (See instructions.) |

|

1 |

|

|

||||||

2. |

Total death taxes paid to other states (from Schedule A on reverse) |

|

2 |

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

3. |

Gross estate outside Connecticut |

|

|

|

3 |

|

|

|

|

|

|

4. |

Total gross estate (from federal Form 706) |

|

4 |

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

5. |

Percentage of estate outside Connecticut (Divide Line 3 by Line 4.) |

|

5 |

|

% |

|

|

|

|||

6. |

Prorated credit (Multiply Line 1 by Line 5.) |

|

6 |

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

7. |

Allowable deduction (Enter Line 2 or Line 6, whichever is less.) |

|

|

|

|

7 |

|

|

|||

8. |

Tentative Connecticut estate tax due (Subtract Line 7 from Line 1.) |

|

|

|

|

8 |

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

9. |

Connecticut succession tax imposed and paid |

|

|

|

|

9 |

|

|

|||

10. |

Connecticut estate tax due (Subtract Line 9 from Line 8. If less than zero, enter zero.) |

|

10 |

|

|

||||||

11. |

Prior estate tax payment(s), including payment made with Form |

|

11 |

|

|

||||||

12. |

If Line 11 is greater than Line 10, enter amount overpaid. (Subtract Line 10 from Line 11.) |

|

|

|

|

||||||

|

12 |

|

|

||||||||

13. |

If Line 10 is greater than Line 11, enter amount due (Subtract Line 11 from Line 10.) |

|

13 |

|

|

||||||

|

|

|

|

|

|

|

|

||||

14. |

If paid late, enter penalty |

|

plus interest |

|

(See instructions.) |

|

14 |

|

|

||

|

|

|

|

|

|

|

|

|

|||

15. |

Amount owed with this return (Add Lines 13 and 14.) |

|

|

|

|

15 |

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Computation of Tax for a Nonresident Decedent’s Estate

16. |

Maximum credit for state death taxes allowable under I.R.C. §2011 (See instructions.) |

|

16 |

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

17. |

Gross estate within Connecticut |

|

|

|

17 |

|

|

|

|

|

|

18. |

Total gross estate (from federal Form 706) |

|

18 |

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

19. |

Percentage of estate within Connecticut (Divide Line 17 by Line 18.) |

|

19 |

|

% |

|

|

|

|||

20. |

Tentative Connecticut estate tax due (Multiply Line 16 by Line 19.) |

|

|

|

|

20 |

|

|

|||

21. |

Connecticut succession tax imposed and paid |

|

|

|

|

21 |

|

|

|||

|

|

|

|

|

|

|

|

||||

22. |

Connecticut estate tax due (Subtract Line 21 from Line 20. If less than zero, enter zero.) |

|

22 |

|

|

||||||

|

|

|

|

|

|

|

|

||||

23. |

Prior estate tax payment(s), including payment made with Form |

|

23 |

|

|

||||||

24. |

If Line 23 is greater than Line 22, enter amount overpaid. (Subtract Line 22 from Line 23.) |

|

24 |

|

|

||||||

25. |

If Line 22 is greater than Line 23, enter amount due (Subtract Line 23 from Line 22.) |

|

25 |

|

|

||||||

|

|

|

|

|

|

|

|

||||

26. |

If paid late, enter penalty |

|

plus interest |

|

(See instructions.) |

|

26 |

|

|

||

|

|

|

|

|

|

||||||

27. |

Amount owed with this return (Add Lines 25 and 26.) |

|

27 |

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

I declare under the penalty of false statement that I have examined this return and, to the best of my knowledge and belief, it is true, complete, and correct; and I declare that I have filed this return with both the Probate Court and DRS.

Fiduciary’s Name |

|

|

Attorney or Authorized Representative’s Name |

|

|

|

|

|

|

|

|

Signature of Fiduciary |

|

Date |

Signature of Attorney or Authorized Representative |

Date |

|

|

|

|

|

|

|

Address |

|

|

Firm Name and Address |

|

|

|

|

|

|

|

|

City |

State |

ZIP Code |

City |

State |

ZIP Code |

|

|

|

|

|

|

Telephone Number |

|

|

Telephone number |

|

|

|

|

|

|

|

|

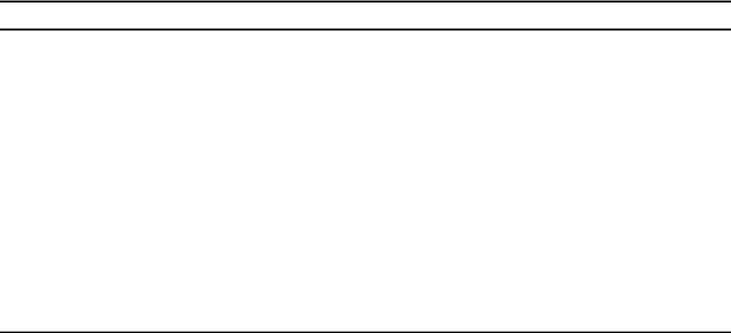

SCHEDULE A — CREDIT FOR DEATH TAXES PAID TO OTHER STATES (Resident Estates Only)

Instructions: Enter on Lines 28 to 30 the amount of estate, inheritance, legacy, or succession taxes paid to any state of the United States (other than the State of Connecticut) or the District of Columbia for which the state tax credit is allowable under I.R.C. §2011 to the estate. The Department of Revenue Services (DRS) will disallow this credit if you fail to complete this schedule or provide adequate proof of the credit claimed. Adequate proof of payment includes a copy of the canceled check and either a signed copy of the death tax return filed with the other state(s) or the District of Columbia or a closing letter from the other state(s) or the District of Columbia certifying the amount of death tax paid. Use a continuation sheet if necessary.

|

Column A |

Column B |

Column C |

Column D |

|

State to Which Death Tax Was Paid |

Proof Submitted |

Date Paid |

Amount of Tax Paid |

28. |

|

|

|

|

29. |

|

|

|

|

|

|

|

|

|

30. |

|

|

|

|

31. |

Total Death Taxes Paid to Other States (Add amounts in Column D) Enter here and on Line 2 |

|

||

|

|

|

|

|

SCHEDULE B — REAL PROPERTY IN CONNECTICUT

Instructions: List real property located in Connecticut in which the decedent had an interest. Use a continuation sheet if necessary.

Address |

Decedent’s Interest |

Assessed Value |

Fair Market Value |

a.

b.

c.

d.

e.

Form |

Page 2 of 4 |

Instructions for Form

General Instructions

The Connecticut estate tax is a transfer tax which absorbs the credit allowable for state death taxes on federal Form 706, United States Estate (and Generation Skipping Transfer) Tax Return, thereby shifting a portion of the federal estate tax to Connecticut by picking up the credit allowed for state death taxes under the Internal Revenue Code (I.R.C.). If you have any questions, please call the Inheritance Tax Section at

Who Must File: Whenever an estate is required to file federal Form 706, the estate must file Form

When and Where to File: Form

Make the check or money order payable to: Commissioner of Revenue Services. Write the decedent’s name, Social Security Number, Connecticut succession tax file number, if known, and “Form

Department of Revenue Services

Inheritance Tax Section

PO Box 2972

Hartford CT

Supporting Documentation: Unless previously submitted with the estate’s Connecticut succession tax return, a complete copy, including all attachments, of federal Form

706must accompany the filing of Form

Extension for Filing or Payment: To request an extension to file or pay the Connecticut estate tax, please file a Form

Amended Returns: An estate must file an amended Form

•The estate files an amended federal Form 706 with the Internal Revenue Service (IRS). The estate must file an amended Form

•The amount of federal estate tax reported on the estate’s federal Form 706 is changed or corrected by the IRS. The estate must file an amended Form

•The estate is a resident estate and has claimed a credit against the Connecticut estate tax for death tax paid to a state of the United States (other than the State of Connecticut) or to the District of Columbia and, as a direct result of the estate filing an amended estate tax return with the other state or District of Columbia, the amount of death tax that the estate is finally required to pay to that state or the District of Columbia is different than the amount used to determine the credit against Connecticut estate tax. The estate must file an amended Form

•The estate is a resident estate and has claimed a credit against the Connecticut estate tax for death tax paid to a state of the United States (other than the state of Connecticut) or to the District of Columbia and, as a direct result of a change or correction to the estate tax return filed with the other state or the District of Columbia by the tax officers or other competent authority of the jurisdiction, the amount of death tax that the estate is finally required to pay to that state or the District of Columbia is different than the amount used to determine the credit against Connecticut estate tax. The estate must file an amended Form

Connecticut

Form |

Page 3 of 4 |

Line Instructions

Line 1: The starting point in computing the Connecticut estate tax is the maximum credit for state death taxes allowable to the estate under I.R.C. §2011. This is the amount that must be entered on Line 1 even if the estate claims no state death tax credit on federal Form 706 or claims a state death tax credit that is less than the maximum credit for state death taxes that is allowable to the estate under I.R.C. §2011. No Connecticut estate tax is due from an estate if the amount of the unified credit allowed to the estate under I.R.C. §2010 exceeds the amount of the federal estate tax that is imposed by I.R.C. §2001.

Line 2: Total death taxes means the total amount of estate, inheritance, legacy, or succession taxes (excluding interest) paid to any state of the United States (other than the State of Connecticut) or to the District of Columbia for which the state tax credit is allowable to the estate under I.R.C. §2011. Payment of these taxes is reported on Lines 28 to 30 on Schedule A. The amount entered on Line 31 of Schedule A is the amount that must be entered on Line 2.

Line 3: Gross estate outside Connecticut means the estate’s real or tangible personal property located outside of Connecticut as properly valued for federal estate tax purposes.

Line 4: Total gross estate means the gross estate as properly valued for federal estate tax purposes.

Line 9: Connecticut succession tax imposed and paid means the amount of succession tax that is imposed under Chapter 216 of the Connecticut General Statutes and that is actually paid to the State of Connecticut. Any credit that an estate claims against the succession tax (such as the credit under Conn. Gen. Stat.

Example: An estate claimed a credit of $3,000 against its succession tax liability for Connecticut gift tax of $3,000 imposed and paid on a gift includable in the donor’s gross taxable estate for succession tax purposes. If the estate’s succession tax liability, but for the credit under Conn. Gen. Stat.

Line 14: The penalty for late payment or underpayment of estate tax is 10% (.10) of the amount due. If no tax is due, the Commissioner of Revenue Services may impose a $50 penalty for the late filing of any return that is required by law to be filed. Interest of 1% (.01) per month or fraction of a month accrues on a late payment or

underpayment of estate tax from the due date of the return until the tax is paid.

Line 16: The starting point in computing the Connecticut estate tax is the maximum state death tax credit allowable to the estate under I.R.C. §2011. This is the amount that must be entered on Line 16 even if the estate claims no state death tax credit on federal Form 706 or claims a state death tax credit that is less than the maximum credit for state death taxes that is allowable to the estate under I.R.C. §2011. No Connecticut estate tax is due from an estate if the amount of the unified credit allowed to the estate under I.R.C. §2010 exceeds the amount of the federal estate tax that is imposed by I.R.C. §2001.

Line 17: Gross estate within Connecticut means the estate’s real or tangible personal property located within Connecticut as properly valued for federal estate tax purposes.

Line 18: Total gross estate means the gross estate as properly valued for federal estate tax purposes.

Line 21: Connecticut succession tax imposed and paid means the amount of succession tax that is imposed under Chapter 216 of the Connecticut General Statutes and that is actually paid to the State of Connecticut. Any credit that an estate claims against the succession tax (such as the credit under Conn. Gen. Stat.

Example: An estate claimed a credit of $3,000 against its succession tax liability for Connecticut gift tax of $3,000 imposed and paid on a gift includable in the donor’s gross taxable estate for succession tax purposes. If the estate’s succession tax liability, but for the credit under Conn. Gen. Stat.

Line 26: The penalty for late payment or underpayment of estate tax is 10% (.10) of the amount due. If no tax is due, the Commissioner of Revenue Services may impose a $50 penalty for the late filing of any return that is required by law to be filed. Interest of 1% (.01) per month or fraction of a month accrues on a late payment or underpayment of estate tax from the due date of the return until the tax is paid.

Form |

Page 4 of 4 |