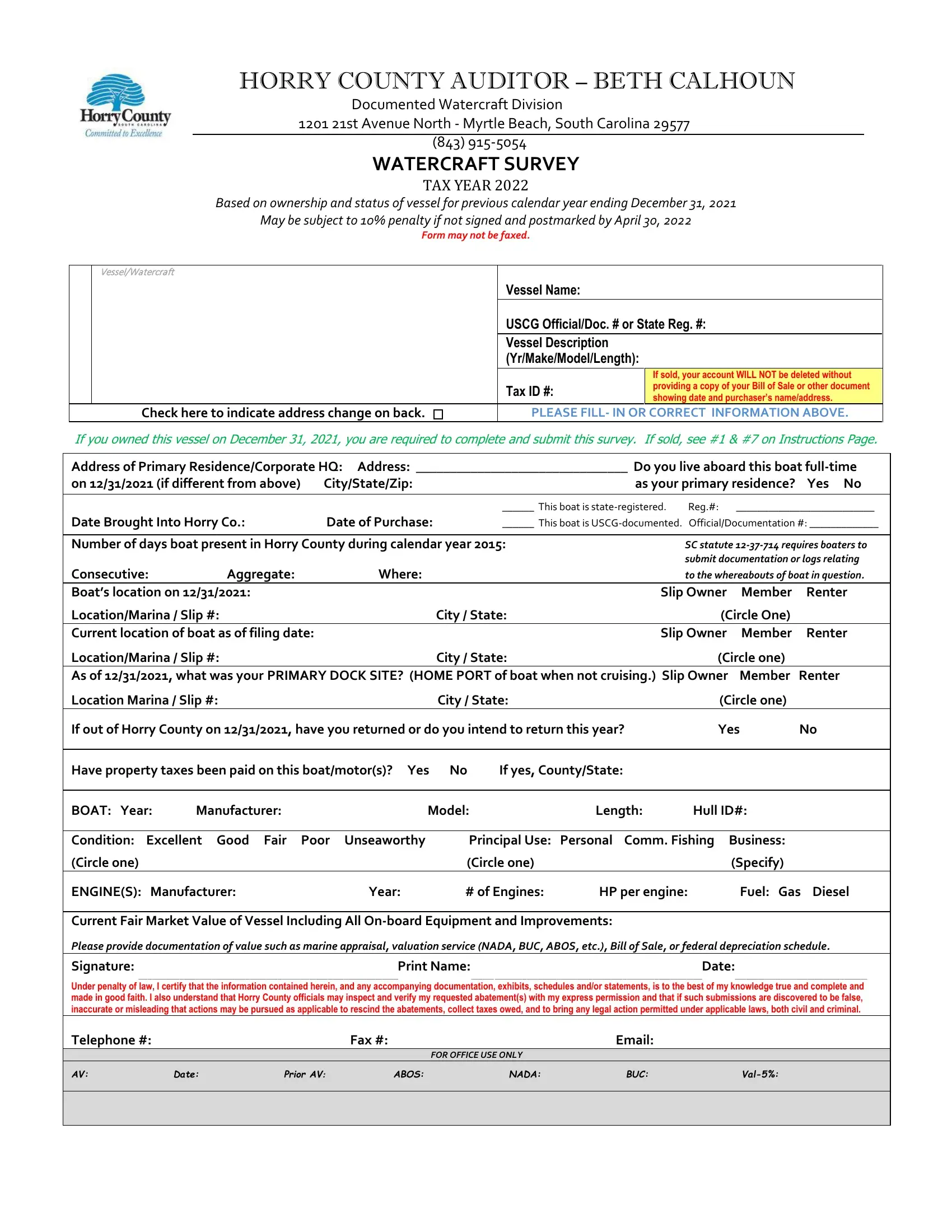

The intricacies of the Horry County Watercraft Survey for the tax year 2021 underscore the meticulous process required for boat owners in Myrtle Beach, South Carolina, to navigate their tax obligations effectively. This comprehensive form, diligently overseen by Horry County Auditor Beth Calhoun, serves a dual purpose: assessing the tax responsibilities based on the watercraft's status as of December 31, 2020, and identifying boats for possible tax exemptions or penalties. Boat owners must accurately disclose details such as the vessel's description, including year, make, model, and length, along with the boat’s usage and domicile specifics at the year’s end to ensure proper tax evaluation. Additionally, the survey delves into the current market value of the vessel, requiring documentation to support the declared value. It's pivotal for owners to submit this survey by April 30, 2021, to avoid a 10% penalty, reflective of Horry County's rigorous stance on compliance. The ordinance also addresses transient boaters, highlighting the county's method in differentiating between various types of watercraft presences and establishing a clear mandate on documentation and tax liability. Through this form, Horry County articulates a structured approach to watercraft taxation, aiming to balance fair assessment with strict enforcement to encapsulate both resident and transient boating activities within its jurisdiction.

| Question | Answer |

|---|---|

| Form Name | Form Horry County |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | Auditor - Horry County GovernmentAuditor - Horry County GovernmentAuditor - Horry County GovernmentHorry County Government - Home |

HORRY COUNTY AUDITOR – BETH CALHOUN

Documented Watercraft Division

1201 21st Avenue North - Myrtle Beach, South Carolina 29577

(843)

WATERCRAFT SURVEY

TAX YEAR 2021

Based on ownership and status of vessel for previous calendar year ending December 31, 2020

May be subject to 10% penalty if not signed and postmarked by April 30, 2021

Form may not be faxed.

|

VESSEL/WATERCRAFT |

|

|

|

|

|

|

Vessel Name: |

|

|

|

|

|

USCG Official/Doc. # or State Reg. #: |

|||

|

|

|

|

|

|

|

|

Vessel Description |

|

|

|

|

|

(Yr/Make/Model/Length): |

|

|

|

|

|

|

|

If sold, your account WILL NOT be deleted without |

|

|

|

Tax ID #: |

|

providing a copy of your Bill of Sale or other document |

|

|

|

|

showing date and purchaser’s name/address. |

|

|

|

Check here to indicate address change on back. |

PLEASE FILL- IN OR CORRECT INFORMATION ABOVE. |

|||

If you owned this vessel on December 31, 2020, you are required to complete and submit this survey. If sold, see #1 & #7 on Instructions Page.

Address of Primary Residence/Corporate HQ: Address: _______________________________ Do you live aboard this boat

on 12/31/2020 (if different from above) |

City/State/Zip: |

as your primary residence? Yes No |

Date Brought Into Horry Co.: |

Date of Purchase: |

______ |

This boat is |

Reg.#: |

__________________________ |

______ |

This boat is |

Official/Documentation #: _____________ |

|

Number of days boat present in Horry County during calendar year 2015:

SC statute

Consecutive: |

Aggregate: |

Where: |

|

|

|

to the whereabouts of boat in question. |

||

Boat’s location on 12/31/2020: |

|

|

|

|

Slip Owner |

Member |

Renter |

|

Location/Marina / Slip #: |

|

City / State: |

|

(Circle One) |

|

|||

Current location of boat as of filing date: |

|

|

|

|

Slip Owner |

Member |

Renter |

|

Location/Marina / Slip #: |

|

City / State: |

|

(Circle one) |

|

|||

As of 12/31/2020, what was your PRIMARY DOCK SITE? (HOME PORT of boat when not cruising.) Slip Owner |

Member |

Renter |

||||||

Location Marina / Slip #: |

|

City / State: |

|

(Circle one) |

|

|||

If out of Horry County on 12/31/2020, have you returned or do you intend to return this year? |

Yes |

No |

||||||

|

|

|

|

|

||||

Have property taxes been paid on this boat/motor(s)? Yes No |

If yes, County/State: |

|

|

|

||||

|

|

|

|

|

|

|

|

|

BOAT: Year: |

Manufacturer: |

|

Model: |

|

Length: |

Hull ID#: |

|

|

|

|

|

|

|

||||

Condition: Excellent Good Fair Poor Unseaworthy |

Principal Use: |

Personal Comm. Fishing |

Business: |

|

||||

(Circle one) |

|

|

(Circle one) |

|

|

(Specify) |

|

|

ENGINE(S): Manufacturer: |

Year: |

# of Engines: |

HP per engine: |

Fuel: Gas Diesel |

||||

Current Fair Market Value of Vessel Including All

Please provide documentation of value such as marine appraisal, valuation service (NADA, BUC, ABOS, etc.), Bill of Sale, or federal depreciation schedule.

Signature: |

Print Name: |

Date: |

|

|

__________________________________________________________________________________________________________________ |

__________ ___________________________________________________________________________________________ |

__________________________________________________________ |

Under penalty of law, I certify that the information contained herein, and any accompanying documentation, exhibits, schedules and/or statements, is to the best of my knowledge true and complete and made in good faith. I also understand that Horry County officials may inspect and verify my requested abatement(s) with my express permission and that if such submissions are discovered to be false, inaccurate or misleading that actions may be pursued as applicable to rescind the abatements, collect taxes owed, and to bring any legal action permitted under applicable laws, both civil and criminal.

Telephone #: |

|

|

Fax #: |

|

Email: |

|

|

|

|

|

FOR OFFICE USE ONLY |

|

|

AV: |

DATE: |

PRIOR AV: |

ABOS: |

NADA: |

BUC: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

FOR MAILING ADDRESS CHANGES ONLY

Name:

Address:

City/State/Zip:

Please read the following information and instructions carefully before submitting this Watercraft Survey.

1.If you owned this vessel on December 31, 2020, you must complete and submit this Survey with postmark by April 30, 2021. The Survey must be completed in its entirety. Failure to do so may result in a tax notice issued with an estimated tax value plus penalty. Unsigned and late Surveys are subject to a 10% penalty.

2.This is only a survey. It is not a tax bill nor does it indicate that your watercraft will be taxed in Horry County. It is intended to distinguish between taxable and exempt watercraft in Horry County.

3.The current state statute allows for, and Horry County Ordinance

4.ATTENTION TRANSIENT BOATERS!!! Under Horry County Ordinance

5.This Watercraft Survey has been mailed to you based on one of the following criteria:

Your official documentation shows an Horry County mailing address.

Your official documentation shows an Horry County hailing port.

Your name was included on an annual list submitted by a local marina.

Your boat was seen in Horry County for an extended period of time.

You are a legal resident of Horry County.

6.South Carolina Code of Laws, Section

(1)All the tangible personal property in the State owned or controlled by him;

(2)All the tangible property owned by him or by any other resident of this State and under his control which may be temporarily out of the State but is intended to be brought into the State;

(3)All tangible personal property owned or controlled by him which may have been sent out of the State for sale and not yet sold.”

7.In cases where a taxable vessel has been sold after the December 31 assessment date, taxes are not automatically prorated by Horry County. The December 31 owner will be billed for the full year’s tax. Section

8.South Carolina Code of Laws, Section

9.South Carolina Code of Laws, Sections

An Attorney General’s opinion on this section states, (for example) “The owner of personal property on December 31, 1979 is required to make a return to the county auditor listing all property owned by him on that date notwithstanding the fact that some property is sold by him in January 1980…a (taxpayer) is liable for the ad valorem tax on all tangible personal property possessed and used by him as of December 31 next preceding the taxable year.”

10.Watercraft considered “temporarily out of the state” on December 31st may still be subject to tax under the SC Code of Laws.

11. |

An Attorney General’s Opinion on SECTION |

|

situated. A pleasure boat owned by an individual(s) and located in South Carolina is to be taxed where the owner thereof shall reside at the |

|

time of the listing. |