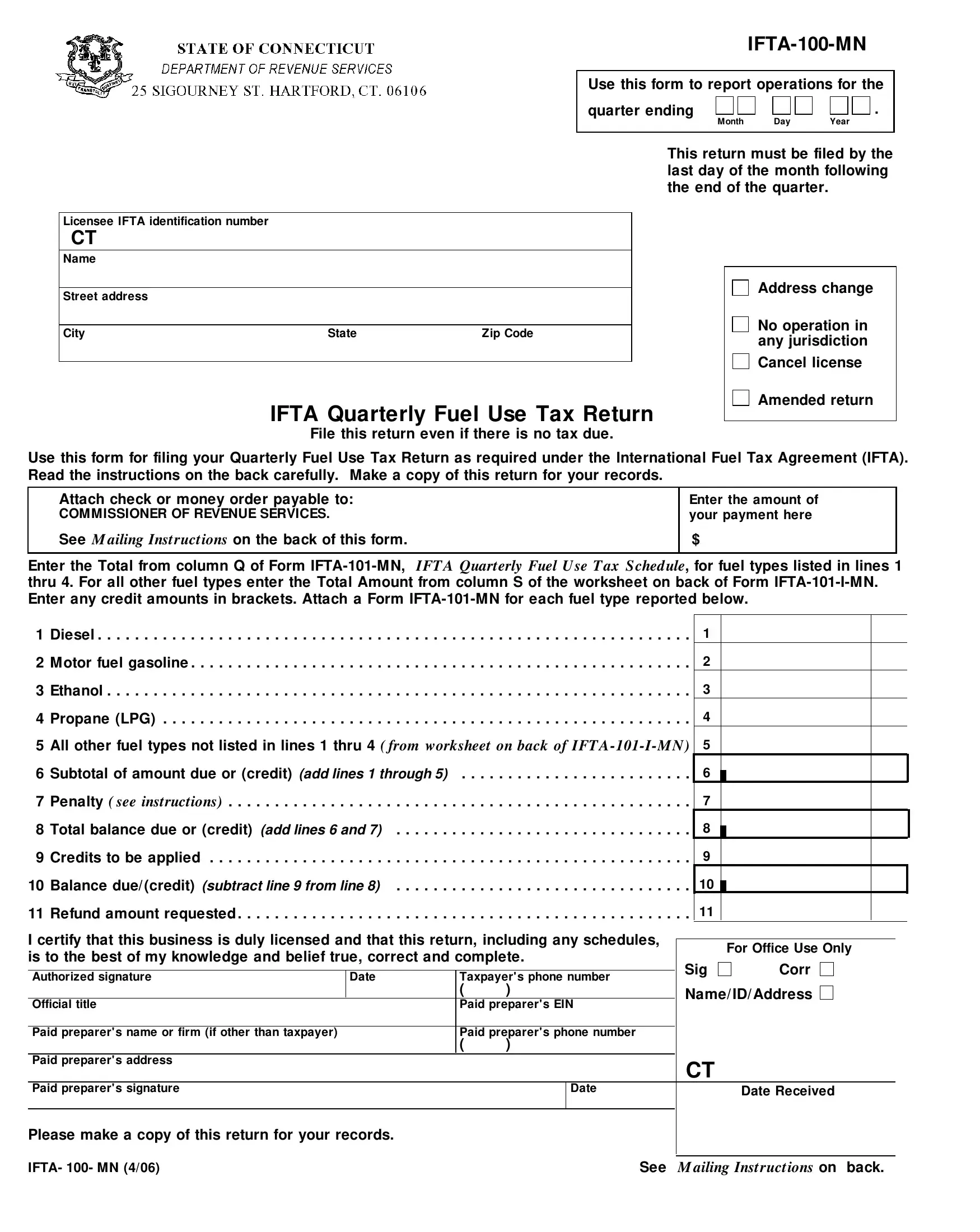

For commercial vehicle operators traversing multiple jurisdictions, the completion of the IFTA-100-MN form is a mandatory quarterly task, as established under the International Fuel Tax Agreement (IFTA). This form, which must be filed by the last day of the month following each quarter’s end, serves as a comprehensive report detailing the amount of fuel used, the taxes owed, or credits to be claimed for different fuel types including diesel, motor fuel gasoline, ethanol, propane, and others not specifically listed. Beyond merely a tax report, the IFTA-100-MN encompasses a variety of operations such as address changes, license cancellations, or amending previous returns, reinforcing its significance to licensees. The form mandates the inclusion of identifying information, thorough tax calculations based on fuel types as itemized in lines 1 through 5, and any resultant penalties. Ensuring accuracy is paramount; thus, attaching the corresponding IFTA-101-MN form for each reported fuel type is required. Furthermore, the form elucidates instructions on penalties for late or incorrect filings, the process for claiming credits, and the specifics on refund requests, all aimed at streamlining the tax reporting process for carriers operating across state lines. This form embodies the intricate balance between regulatory compliance and the operational realities of interstate commercial transport, noting the importance of precise record-keeping and the potential financial implications of the tax liabilities or credits reported.

| Question | Answer |

|---|---|

| Form Name | Form Ifta 100 Mn |

| Form Length | 22 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 5 min 30 sec |

| Other names | IFTA, Virginia, M-85, LNG |