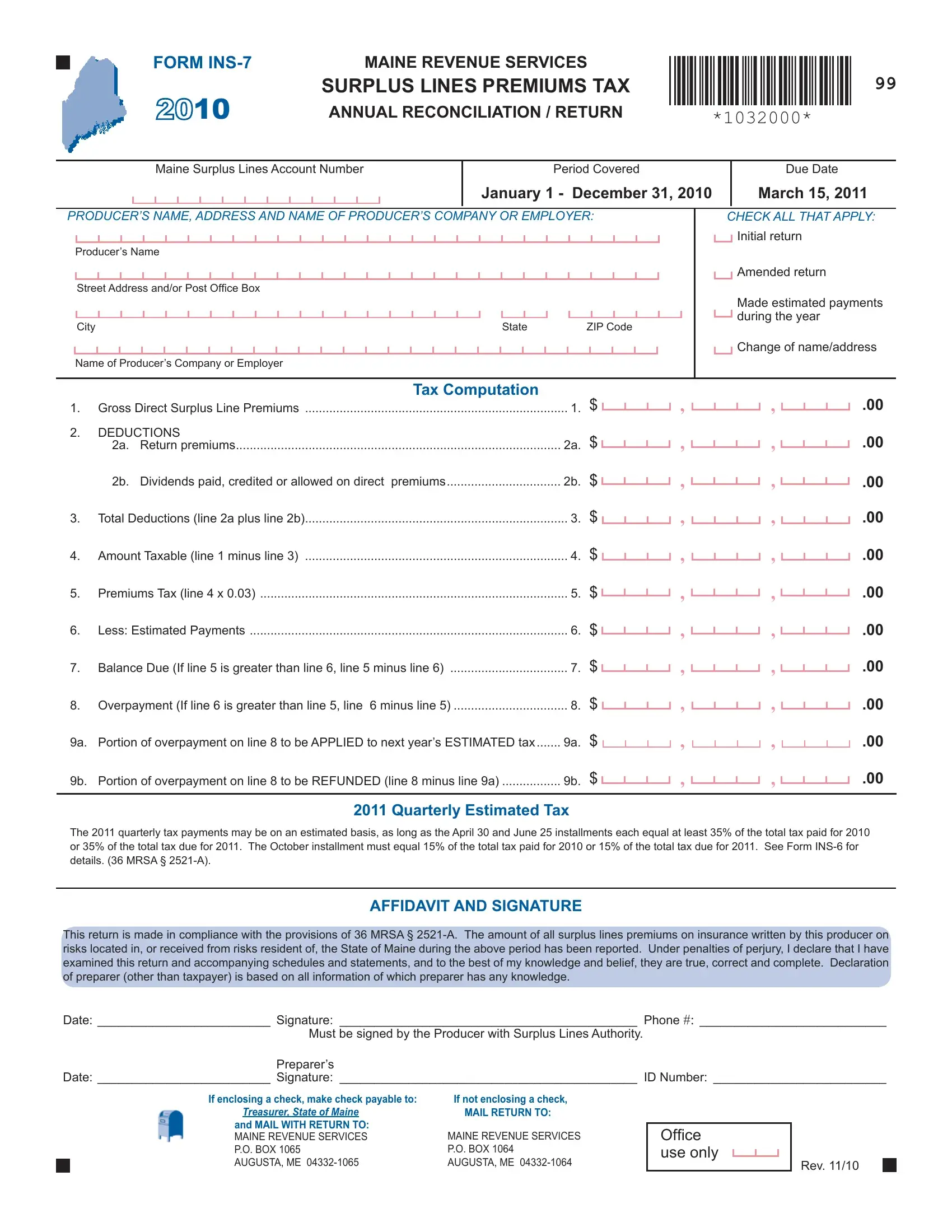

The Form INS-7 is a critical document for licensed producers with surplus lines authority in Maine, necessitating a detailed annual reconciliation and return of surplus lines premiums tax for the specified period, specifically January 1 to December 31, 2010, with a due date of March 15, 2011. This form encompasses various sections including the producer's information, tax computation, estimated payments for the subsequent year, and declarations to ensure compliance under the 36 MRSA § 2521-A. Producers must report gross direct surplus line premiums, along with deductions such as return premiums and dividends, to calculate the taxable amount and determine the balance due or overpayment. The form also outlines the option for agencies to report on behalf of their employee producers and stipulates the necessity for estimated tax payments for insurers, pegged to specific percentages of the tax liabilities from the previous or current year. Additionally, the document sets forth the interest and penalties for late filings or payments, the importance of reporting in whole dollar amounts, and the imperative of maintaining supporting records accessible for at least six years. With provisions for electronic payments for taxpayers with large annual tax liabilities, the Form INS-7 plays a pivotal role in ensuring producers accurately fulfill their tax obligations, underpinning the tax framework for surplus lines in Maine.

| Question | Answer |

|---|---|

| Form Name | Form Ins 7 |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | preparer, Insurers, 2010, 2011 |