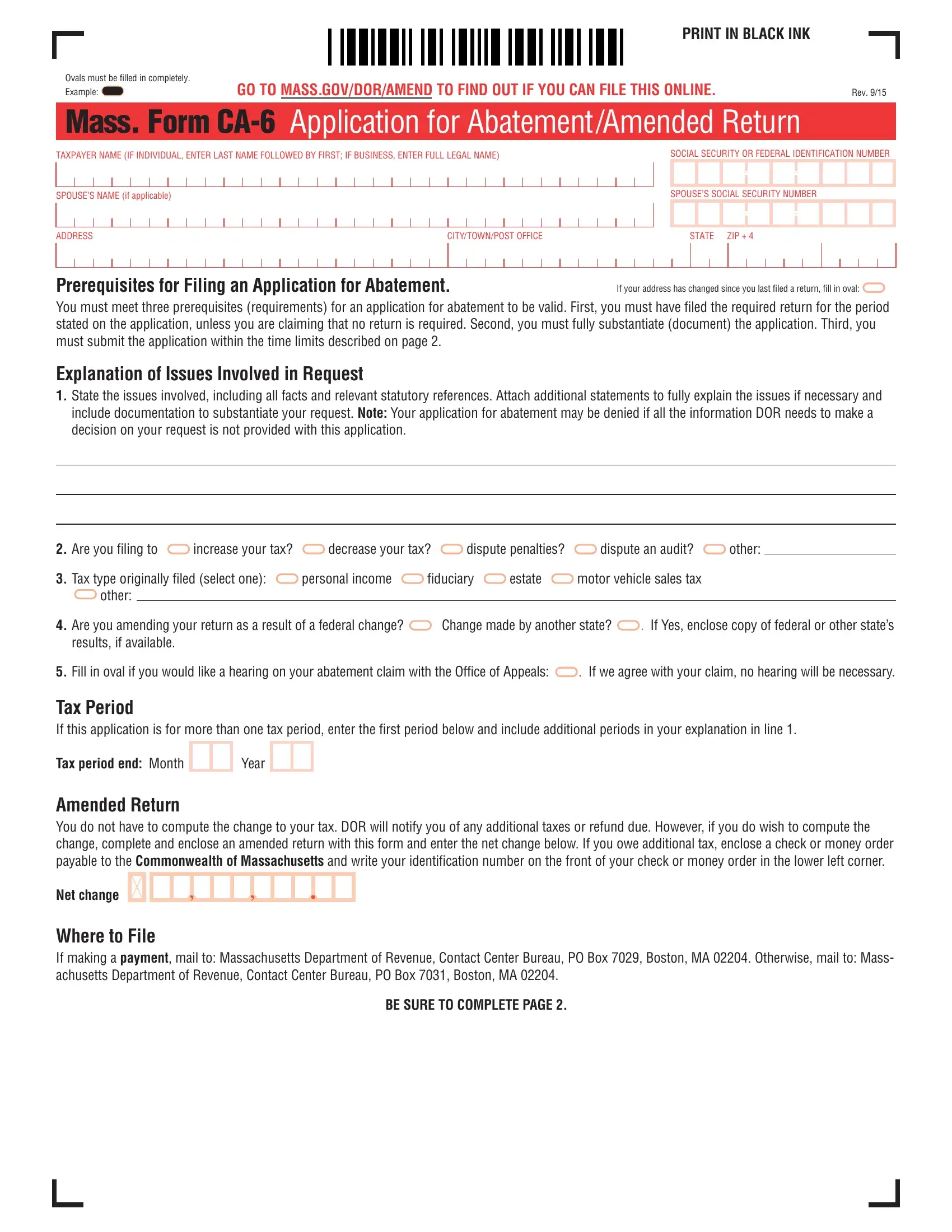

When taxpayers in Massachusetts face the need to correct or challenge their tax liabilities, the Mass. Form CA-6, known officially as the Application for Abatement/Amended Return, serves as their primary tool. This document, designed for clarity and efficiency, requires use of black ink for its completion, and emphasizes full oval shading for selections, a small but important detail aimed at ensuring accuracy in processing. Through detailed sections, it guides users—from individuals to businesses—through the intricate process of requesting a tax review, whether for increasing or decreasing tax burdens, disputing penalties, or addressing audit outcomes. It stresses the necessity of timely filing, adherence to documentation requirements, and clear communication of the issues at hand. Moreover, the form offers the choice of a hearing on the abatement claim, underscoring the state's commitment to due process. With explicit instructions for mailing, accompanied by a rigorous set of prerequisites, the form delineates a path for taxpayers to amend their returns or seek abatements within specific time frames stipulated by Massachusetts law. This process, while complex, is streamlined through the structured guidance provided on the form, encouraging accuracy and thoroughness in submission. Additionally, the form allows for the naming of a representative through a Power of Attorney section, illustrating its comprehensive approach to catering to varied taxpayer circumstances and reinforcing the importance of authorized, accurate representation in financial matters.

| Question | Answer |

|---|---|

| Form Name | Form Mass Ca 6 |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | form ca mass 6, form 6 application, massachusetts ma 6, mass forms |