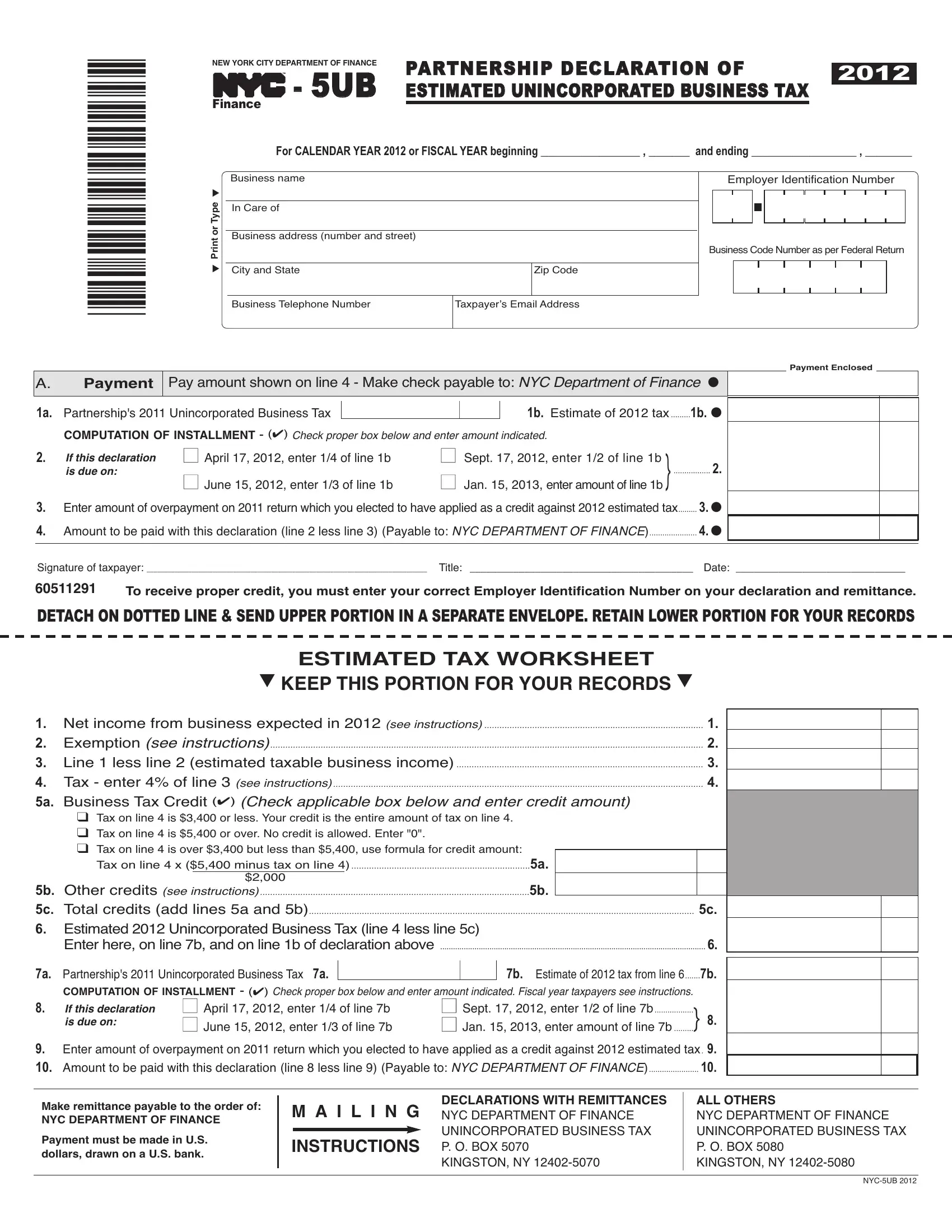

Every year, businesses operating within New York City have to navigate through a myriad of tax obligations to remain compliant with local regulations. Among these obligations is the NYC 5UB form, a critical document for partnerships and certain other business entities that are not incorporated. This form serves a dual purpose: it is both a declaration of estimated unincorporated business tax for the year ahead and a tool for settling any prior year's tax overpayments against the current year's anticipated tax liabilities. For the fiscal or calendar year 2012, partnerships had to assess their business incomes, calculate their estimated taxes due, and decide on their payment schedules, options that include but are not limited to, quarterly installments or a lump sum payment. The form, detailed in its approach, requires information on business and taxpayer identities, a computation of the installment based on the estimated tax, and a method for applying previous overpayments toward the current year's tax obligations. Furthermore, it meticulously guides taxpayers through estimating their business tax by accounting for net business income, allowable exemptions, and possible tax credits, thereby ensuring that each entity contributes its fair share to the city's finances. Such calculated contributions help fund municipal services and infrastructure, underlying the form's significance in the broader context of New York City's fiscal management and the collective responsibility of its business community.

| Question | Answer |

|---|---|

| Form Name | Form Nyc 5Ub |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | Jan, REMITTANCES, nyc 5ub, 2011 |

|

*60511291* |

▼ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

NEWYORKCITYDEPARTMENTOFFINANCE |

PARTNERSHIP DECLARATION OF |

|

|

|

|

|

|

|

2012 |

|

||||||||||||||||||

|

|

|

|

- 5UB |

ESTIMATED UNINCORPORATED BUSINESS TAX |

|

|

|

|

|

|

|

|

|||||||||||||||||

|

|

FINANCE |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

For CALENDAR YEAR 2012 or FISCAL YEAR beginning _________________ , _______ and ending __________________ , ________ |

||||||||||||||||||||||||||

|

|

|

|

Business name |

|

|

|

|

|

|

|

Employer Identification Number |

||||||||||||||||||

|

|

▼ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Typeor |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

In Care of |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Business address (number and street) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

BusinessCodeNumberasperFederalReturn |

||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City and State |

|

|

|

|

Zip Code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Business Telephone Number |

|

Taxpayerʼs Email Address |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Payment Enclosed |

|

|

|

|

|

|||||||

A. |

Payment |

Pay amount shown on line 4 - Make check payable to: NYC Department of Finance ● |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

1a. Partnership's 2011 Unincorporated Business Tax |

|

|

|

|

1b. Estimate of 2012 tax.........1b. ● |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

COMPUTATION OF INSTALLMENT - (✔) Check proper box below and enter amount indicated. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

2. |

If this declaration |

■ April 17, 2012, enter 1/4 of line 1b |

■ Sept. 17, 2012, enter 1/2 of line 1b |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

is due on: |

■ June 15, 2012, enter 1/3 of line 1b |

■ Jan. 15, 2013, enteramountofline1b}................. 2. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

3. |

Enteramountofoverpaymenton2011returnwhichyouelectedtohaveappliedasacreditagainst2012estimatedtax......... 3. ● |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

4. |

Amount to be paid with this declaration (line 2 less line 3) (Payable to: NYC DEPARTMENT OF FINANCE)...................... 4. ● |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Signature of taxpayer: _________________________________________________________________________________ Title: _________________________________________ Date: ____________________________

60511291 |

To receive proper credit, you must enter your correct Employer Identification Number on your declaration and remittance. |

DETACHONDOTTEDLINE&SENDUPPERPORTIONINASEPARATEENVELOPE.RETAINLOWERPORTIONFORYOURRECORDS

ESTIMATED TAX WORKSHEET

▼ KEEP THIS PORTION FOR YOUR RECORDS ▼

1. |

Net income from business expected in 2012 (see instructions) |

1. |

2. |

Exemption (see instructions) |

2. |

3. |

Line 1 less line 2 (estimated taxable business income) |

3. |

4. |

Tax - enter 4% of line 3 (see instructions) |

4. |

5a. |

Business Tax Credit (✔) (Check applicable box below and enter credit amount) |

|

❑Tax on line 4 is $3,400 or less. Your credit is the entire amount of tax on line 4.

❑Tax on line 4 is $5,400 or over. No credit is allowed. Enter "0".

❑Tax on line 4 is over $3,400 but less than $5,400, use formula for credit amount:

Tax on line 4 x ($5,400 minus tax on line 4) |

.......................................................................5a. |

|

$2,000 |

|

|

5b. Other credits (see instructions) |

5b. |

|

5c. Total credits (add lines 5a and 5b) |

5c. |

|

6.Estimated 2012 Unincorporated BusinessTax (line 4 less line 5c)

|

Enter here, online 7b, and on line 1bof declaration above |

............................................................................................................................ |

|

|

6. |

||

7a. |

Partnership's 2011 Unincorporated BusinessTax 7a. |

|

|

|

7b. Estimateof2012taxfromline6 |

7b. |

|

|

|

|

|||||

|

COMPUTATION OF INSTALLMENT - (✔) Check proper box below and enter amount indicated. Fiscal year taxpayers see instructions. |

|

|||||

8. |

If this declaration |

■ April 17, 2012, enter 1/4 of line 7b |

■ Sept. 17, 2012, enter 1/2 of line 7b |

} 8. |

|||

|

is due on: |

■ June 15, 2012, enter 1/3 of line 7b |

■ Jan. 15, 2013, enter amount of line 7b |

||||

9.Enter amount of overpayment on 2011 return which you elected to have applied as a credit against 2012 estimated tax. 9.

10. Amount to be paid with this declaration (line 8 less line 9) (Payable to: NYC DEPARTMENT OF FINANCE) |

10. |

Make remittance payable to the order of:

NYC DEPARTMENT OF FINANCE

Payment must be made in U.S. dollars, drawn on a U.S. bank.

M A I L I N G

INSTRUCTIONS

DECLARATIONS WITH REMITTANCES

NYC DEPARTMENT OF FINANCE UNINCORPORATED BUSINESS TAX P. O. BOX 5070

KINGSTON, NY

ALL OTHERS

NYC DEPARTMENT OF FINANCE UNINCORPORATED BUSINESS TAX P. O. BOX 5080

KINGSTON, NY

Form |

Page 2 |

|

|

NOTE

IfanyduedatefallsonSaturday,Sundayorlegalholiday,filingwillbetimelyifmade bythenextdaywhichisnotaSaturday,Sundayorholiday.

PURPOSEOFDECLARATION

ThisdeclarationformprovidesameansofpayingUnincorporatedBusinessTaxonacurrent basis for partnerships, joint ventures and similar entities (other than individuals, estates and trusts)engagedincarryingonanunincorporatedbusinessorprofession,asdefinedinSection

Everyunincorporatedbusinessmustfileanincometaxreturnafterthecloseofitstaxableyear and pay any balance of tax due. If the tax has been overpaid, adjustment will be made only after the return has been filed.

WHOMUSTMAKEADECLARATION

A2012 declaration must be made by every partnership carrying on an unincorporated busi- nessorprofessioninNewYorkCityifitsestimatedtax(line6oftaxcomputationschedule) can reasonably be expected to exceed $3,400 for the calendar year 2012 (or, in the case of a fiscal year taxpayer, for the partnership fiscal year beginning in 2012).

WHENANDWHERETOFILEDECLARATION

You must file the declaration for the calendar year 2012 on or beforeApril 17, 2012, or on the applicable later dates specified in these instructions.

- Allotherdeclarations- |

|

NYCDepartmentofFinance |

NYCDepartmentofFinance |

UnincorporatedBusinessTax |

UnincorporatedBusinessTax |

P.O.Box5070 |

P.O.Box5080 |

Fiscal year taxpayers, read instructions opposite regarding filing dates.

HOWTOESTIMATEUNINCORPORATEDBUSINESSTAX

The worksheet on the front of this form will help you in estimating the tax for 2012.

LINE1-

Theterm“netincomefrombusinessexpectedin2012”meanstheamountthepartnershipes- timatestobeitsincomefor2012computedbeforethespecificexemption.RefertoSchedule A, line 14 of the 2011 Partnership Return (Form

The amount of the allowable exemption may be determined by referring to the instructions for the 2011 Form

If you expect to receive a refund or credit in 2012 of any sales or compensating use tax for which a credit was claimed in a prior year underAdministrative Code Sections

Enter on line 5b the amount estimated to be the sum of any credits allowable for 2012 under

DECLARATION

Online1aofthedeclaration(line7aoftheEstimatedTaxWorksheet),entertheamountthe partnership reported on line 25 of its 2011 Form

PAYMENTOFESTIMATEDTAX

Exceptasspecifiedelsewhereintheseinstructions,theestimatedtaxonline1bofthedeclaration ispayableinequalinstallmentsonorbeforeApril17,2012,June15,2012,September17,2012 andJanuary15,2013. Thefirstinstallmentpaymentmustaccompanythedeclaration.However, theestimatedtaxmaybepaidinfullwiththedeclaration.

Iftherewasanoverpaymentonthe2011PartnershipTaxReturnandonline32boftheNYC- 204 or line 13 of the

Make remittance payable to NYC DEPARTMENT OF FINANCE. All remittances must be

payableinU.S.dollarsdrawnonaU.S.bank. Checksdrawnonforeignbankswillberejected and returned.Aseparate check for the declaration will expedite processing of the payment.

AMENDEDDECLARATION

If,afteradeclarationisfiled,theestimatedtaxincreasesordecreasesbecauseofachangein income, deductions, or allocation, you should file an amended declaration on or before the next date for payment of an installment of estimated tax. This is done by completing the

CHARGEFORUNDERPAYMENTOFINSTALLMENTSOFESTIMATEDTAX

Acharge is imposed for underpayment of an installment of estimated tax for 2012. For in- formationregardinginterestrates,call311. IfcallingfromoutsideofthefiveNYCboroughs, please call

PENALTIES

The law imposes penalties for failure to make a declaration or pay estimated tax due or for making a false or fraudulent declaration or certification.

FISCALYEARTAXPAYERS

InthecaseofapartnershipthatfilesitsUnincorporatedBusinessTaxReturnonafiscalyear basis,substitutethecorrespondingfiscalyearmonthsforthemonthsspecifiedintheinstruc- tions. For example, if the fiscal year begins onApril 1, 2012, the Declaration of Estimated Unincorporated Business Tax will be due on July 16, 2012, together with payment of first quarterestimatedtax.Inthiscase,equalinstallmentswillbedueonorbeforeSeptember17, 2012, December 17, 2012, andApril 16, 2013.

CHANGESININCOME

EventhoughonApril17,2012,apartnershipdoesnotexpectitsunincorporatedbusinesstax toexceed$3,400,achangeinincome,allocationorexemptionmayrequirethatadeclaration be filed later. In this event the requirements are as follows:

|

|

File |

Amountof |

|

Installment |

Ifrequirementforfilingoccurs: |

declaration |

estimated |

|

payment |

|

|

|

by: |

taxdue |

|

dates |

AFTER |

BUT BEFORE |

|

|

|

|

|

|

|

|

|

|

April 1, 2012 |

June 2, 2012 |

June 15, 2012 |

1/3 |

(1) |

June 15, 2012 |

....................................... |

|

|

|

(2) |

Sept. 17, 2012 |

....................................... |

|

|

|

(3) |

Jan. 15, 2013 |

June 1, 2012 |

Sept. 2, 2012 |

Sept. 17, 2012 |

1/2 |

(1) |

Sept. 17, 2012 |

....................................... |

|

|

|

(2) |

Jan. 15, 2013 |

|

|

|

|

|

|

Sept. 1, 2012 |

Jan. 1, 2013 |

Jan. 15, 2013 |

100% |

None |

|

If the partnership files its 2012 Unincorporated BusinessTax Return by February 15, 2013, andpaysthefullbalanceoftaxdue,itneednot:(A) fileanamendeddeclarationoranoriginal declarationotherwisedueforthefirsttimeonJanuary15,2013,or(B) paythelastinstallment of estimated tax otherwise due and payable on January 15, 2013.

CAUTION

AnextensionoftimetofileyourfederaltaxreturnorNewYorkStatepartnershipinformation return does NOTextend the filing date of your NewYork City tax return.

NOTE

Filing a declaration or an amended declaration, or payment of the last installment on January 15,2013,orfilingataxreturnbyFebruary15,2013,willnotsatisfythefilingrequirementsif thepartnershipfailedtofileorpayanestimatedtaxwhichwasdueearlierinthetaxableyear.

ELECTRONICFILING

Note:Registerforelectronicfiling. Itisaneasy,secureandconvenientwaytofileandpayan extension

For more information log on to nyc.gov/nycefile.

To receive proper credit, you must enter your correct Employer Identification Number on your declaration and remittance.