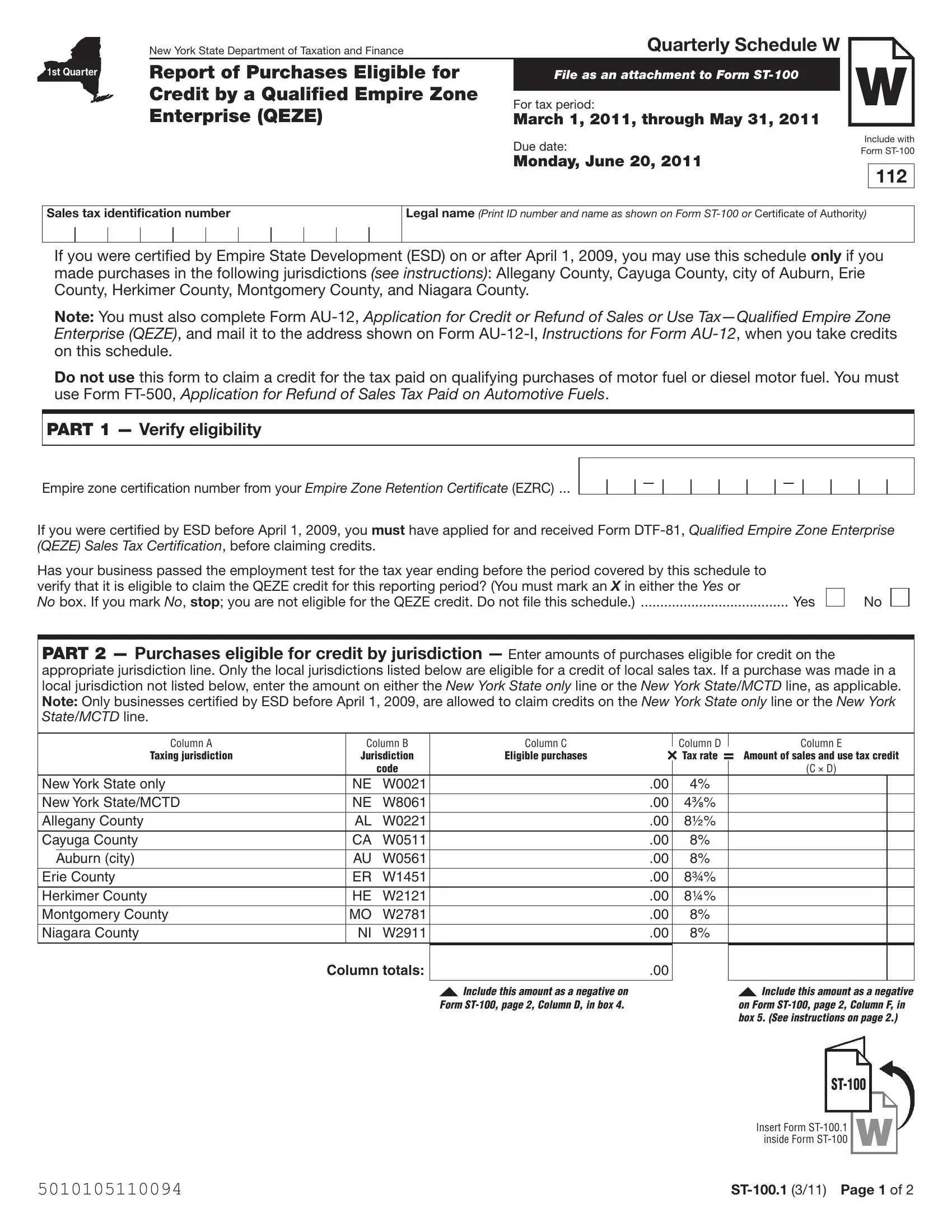

Understanding the intricacies of tax forms is fundamental for businesses aiming to leverage available credits to minimize their tax liabilities. Among these, the New York State Department of Taxation and Finance's ST-100.1 form emerges as a critical document for Qualified Empire Zone Enterprises (QEZE). Specifically designed for entities certified under the Empire State Development (ESD) before or after April 1, 2009, this form serves as a quarterly schedule W report, detailing purchases eligible for sales and use tax credit. It’s not just a mere form but a gateway for qualifying businesses in designated jurisdictions—including Allegany County, Cayuga County, city of Auburn, Erie County, Herkimer County, Montgomery County, and Niagara County—to substantiate their eligibility for significant tax relief. The form intricately ties to the ST-100, New York State and Local Quarterly Sales and Use Tax Return, stressing the importance of accurate completion and submission alongside requisite documents such as Form AU-12, Application for Credit or Refund of Sales or Use Tax. Crucially, businesses must verify their eligibility through the Empire Zone Retention Certificate (EZRC) number, pass an employment test for the tax year preceding the period covered by the schedule, and meticulously report eligible purchases by the jurisdiction to claim their dues. This holistic approach underscores the state's effort to balance economic stimulation with precise tax compliance, making the ST-100.1 form a pivotal component of the QEZE program’s fiscal machinery.

| Question | Answer |

|---|---|

| Form Name | Form St 100 1 |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | 2009, june, 100, New_York |