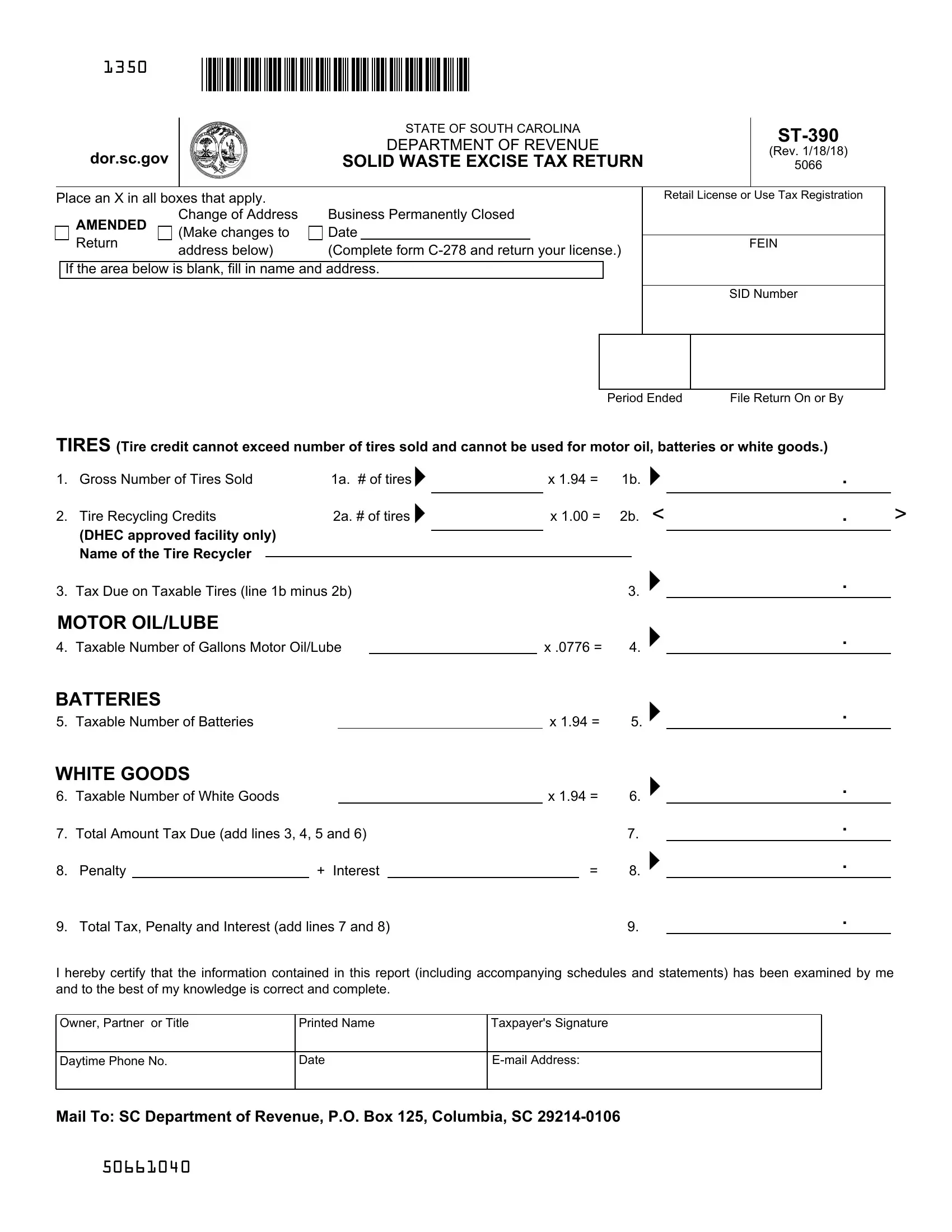

Understanding the ins and outs of specific tax forms can often feel overwhelming, yet with the right guidance, it becomes a manageable task. The State of South Carolina, through its Department of Revenue, mandates the use of the ST-390 form, a pivotal document for tire and battery retailers as well as motor oil and white good wholesalers. Known officially as the Solid Waste Excise Tax Return, its revision date stamps back to January 18, 2018, signaling the state’s effort to keep its procedures up-to-date. Designed with meticulous sections to cover various taxable items, the form serves a dual purpose; it not only facilitates the accurate computation of taxes due on sales of specific goods like tires, motor oils, batteries, and white goods but also streamlines the recycling credit process for tires. The form requires sellers to report the gross number of items sold and apply predetermined rates to calculate the tax due. Additionally, it presents an opportunity for businesses to reduce their payable amount through credits for tires recycled at approved facilities, emphasizing the state’s commitment to environmental stewardship. Integral deadlines align with the general sales tax return, offering a structured timeline for submissions. Fees per item sold are clearly defined, alongside instructions for computing the total amount due, optimizing the filing process. With avenues for penalty and interest calculation on late filings or payments explicitly outlined, the ST-390 form embodies a comprehensive tool for managing solid waste excise tax obligations in South Carolina.

| Question | Answer |

|---|---|

| Form Name | Form St 390 |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | form 390, how to st390, south carolina st390, st 390 south carolina |