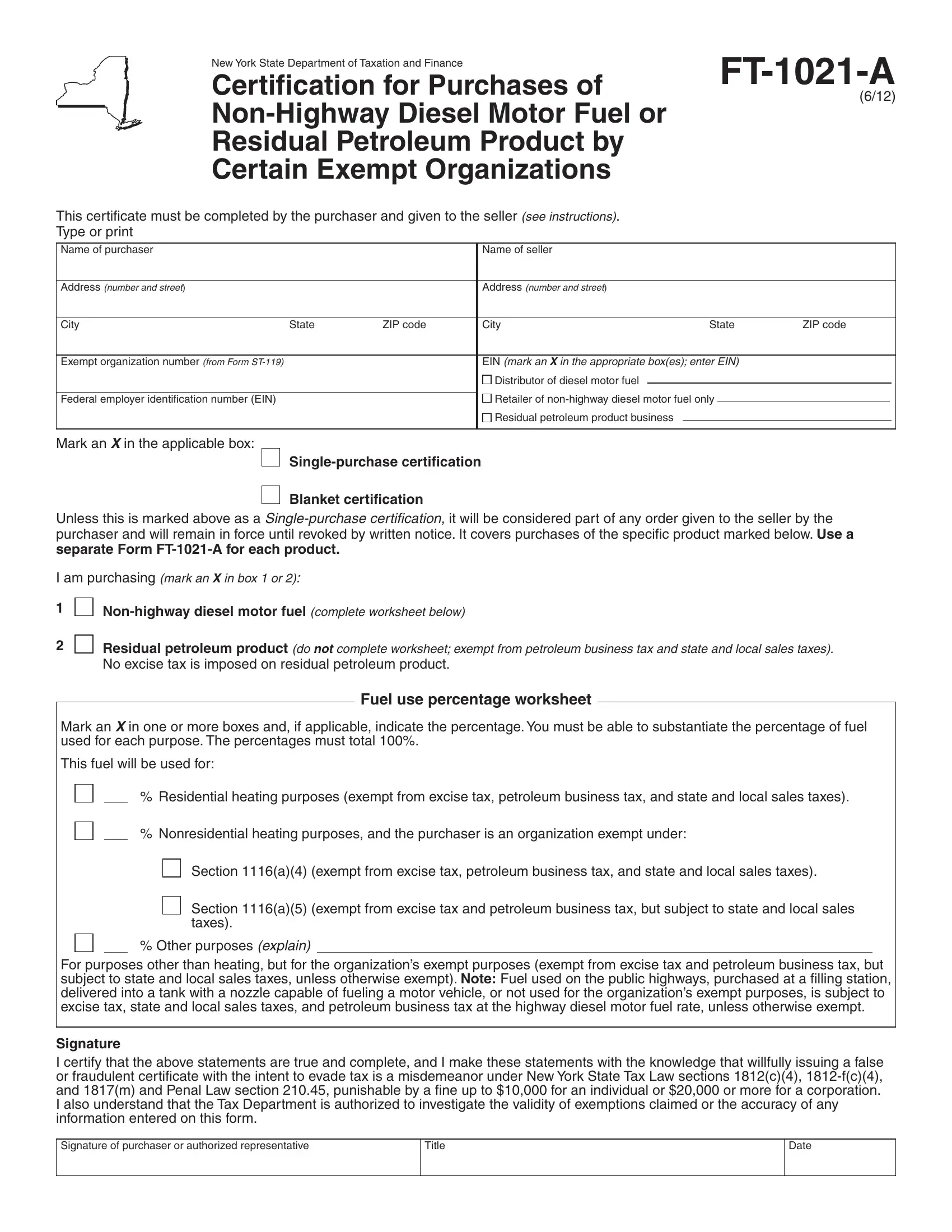

The New York State Department of Taxation and Finance offers a crucial document known as the FT-1021-A form, which serves as a Certification for Purchases of Non-Highway Diesel Motor Fuel or Residual Petroleum Product by Certain Exempt Organizations. This form is meticulously designed to facilitate tax-exempt purchases by qualifying organizations, ensuring they navigate the complexities of fuel taxation with ease. Organizations granted exempt status under specific sections of Tax Law can utilize this form to purchase non-highway diesel motor fuel or residual petroleum products without incurring the usual taxes. The form demands detailed information from the purchaser and the seller, including names, addresses, and tax identification numbers, highlighting its comprehensive nature in promoting tax compliance and accountability. Moreover, it distinguishes between single-purchase and blanket certifications, offering flexibility based on the purchasing needs of the organization. By categorizing fuel usage and detailing the tax exemption requirements for various types of fuel, including those used for residential heating or organizational purposes, the FT-1021-A form plays a pivotal role in simplifying the tax exemption process for eligible entities. This streamlined approach not only aids in the precise documentation and substantiation of fuel usage but also underscores the legal obligations of organizations to adhere to strict guidelines to maintain their exempt status, thus fostering a culture of transparency and diligence in tax-related matters.

| Question | Answer |

|---|---|

| Form Name | Ft 1021 A Form |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | form 1021, NonHighway, 1812-f, 1021 form |

New York State Department of Taxation and Finance

Certification for Purchases of

Residual Petroleum Product by

Certain Exempt Organizations

This certificate must be completed by the purchaser and given to the seller (see instructions). Type or print

(6/12)

Name of purchaser |

|

|

Name of seller |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address (number and street) |

|

|

Address (number and street) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City |

State |

ZIP code |

City |

State |

ZIP code |

||||

|

|

|

|

|

|

|

|

|

|

Exempt organization number (from Form |

|

|

EIN (mark an X in the appropriate box(es); enter EIN) |

|

|

|

|||

|

|

|

Distributor of diesel motor fuel |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Retailer of |

|

|

|

|

||

Federal employer identification number (EIN) |

|

|

|

|

|

|

|||

|

|

|

|

|

|

||||

|

|

|

Residual petroleum product business |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

Mark an X in the applicable box:

Blanket certification

Unless this is marked above as a

separate Form

I am purchasing (mark an X in box 1 or 2):

1

2

Residual petroleum product (do NOT complete worksheet; exempt from petroleum business tax and state and local sales taxes).

No excise tax is imposed on residual petroleum product.

Fuel use percentage worksheet

Mark an X in one or more boxes and, if applicable, indicate the percentage. You must be able to substantiate the percentage of fuel used for each purpose. The percentages must total 100%.

This fuel will be used for:

% Residential heating purposes (exempt from excise tax, petroleum business tax, and state and local sales taxes).

% Nonresidential heating purposes, and the purchaser is an organization exempt under:

Section 1116(a)(4) (exempt from excise tax, petroleum business tax, and state and local sales taxes).

Section 1116(a)(5) (exempt from excise tax and petroleum business tax, but subject to state and local sales taxes).

% Other purposes (explain)

For purposes other than heating, but for the organization’s exempt purposes (exempt from excise tax and petroleum business tax, but subject to state and local sales taxes, unless otherwise exempt). Note: Fuel used on the public highways, purchased at a filling station, delivered into a tank with a nozzle capable of fueling a motor vehicle, or not used for the organization’s exempt purposes, is subject to excise tax, state and local sales taxes, and petroleum business tax at the highway diesel motor fuel rate, unless otherwise exempt.

Signature

I certify that the above statements are true and complete, and I make these statements with the knowledge that willfully issuing a false or fraudulent certificate with the intent to evade tax is a misdemeanor under New York State Tax Law sections 1812(c)(4),

Signature of purchaser or authorized representative

Title

Date

Page 2 of 2

Instructions

Who may use this form

This certification may be used only by organizations

granted exempt organization status under Tax Law, Article 28, section 1116(a)(4) or section 1116(a)(5). The exempt organization must give its supplier a completed Form

Organizations exempt under section 1116(a)(4) include organizations operated exclusively for religious, charitable, scientific, literary, or educational purposes, or to foster national or international amateur sports competition, or for the prevention of cruelty to children or animals.

Organizations exempt under section 1116(a)(5) include posts or organizations of past or present members of the armed forces of the United States, or auxiliary units, or societies of, or trusts or foundations for, any of these posts or organizations.

Sellers

Your sales are subject to the applicable taxes on

Definitions

Diesel motor fuel is No. 1 diesel motor fuel, No. 2 diesel motor fuel, biodiesel, kerosene, fuel oil or other middle distillate and also motor fuel suitable for use in the operation of an engine of the diesel type. It does not include any product specifically designated as No. 4 diesel motor fuel.

Highway diesel motor fuel is any diesel motor fuel which is not

Residual petroleum product includes the topped crude of refinery operations consisting of No. 5 fuel oil, No. 6 fuel oil, bunker C, and that special grade of diesel product specifically designated as No. 4 diesel fuel that is not suitable for use in the operation of a motor vehicle engine.

Dyed diesel motor fuel is diesel motor fuel that has been dyed in accordance with and for the purpose of complying with the provisions of 26 USC 4082(a).

General information

All

This certification may not be used for purchases of fuel for use in unrelated business activities. An exempt organization is engaged in unrelated business activities if the trade or business regularly carried on by the organization is not substantially related (aside from its need for income or funds or the use it makes of the

profits derived) to the exercise or performance of its charitable, educational, or other purpose or function.

Volunteer fire companies and voluntary ambulance services may purchase motor fuel or diesel motor fuel for use in motor vehicles exempt from NYS and local sales taxes by giving the supplier both a properly completed Form

Exempt organizations that use

Exempt organizations that must pay NYS and local sales taxes may claim a refund of the sales taxes by completing and filing Form

Certain exempt organizations may be able to claim a refund of the excise tax on Form

The exempt organization must use Form

Need help?

Visit our Web site at www.tax.ny.gov

•get information and manage your taxes online

•check for new online services and features

Telephone assistance

Miscellaneous Tax Information Center: (518)

To order forms and publications: |

(518) |

|

|

Text Telephone (TTY) Hotline (for persons with hearing and speech disabilities using a TTY): If you have access to a TTY, contact us at (518)

If you do not own a TTY, check with independent

living centers or community action programs to ind out where machines are available for public use.

Persons with disabilities: In compliance with the

Americans with Disabilities Act, we will ensure that our lobbies, ofices, meeting rooms, and other

facilities are accessible to persons with disabilities. If you have questions about special accommodations for persons with disabilities, call the information center.