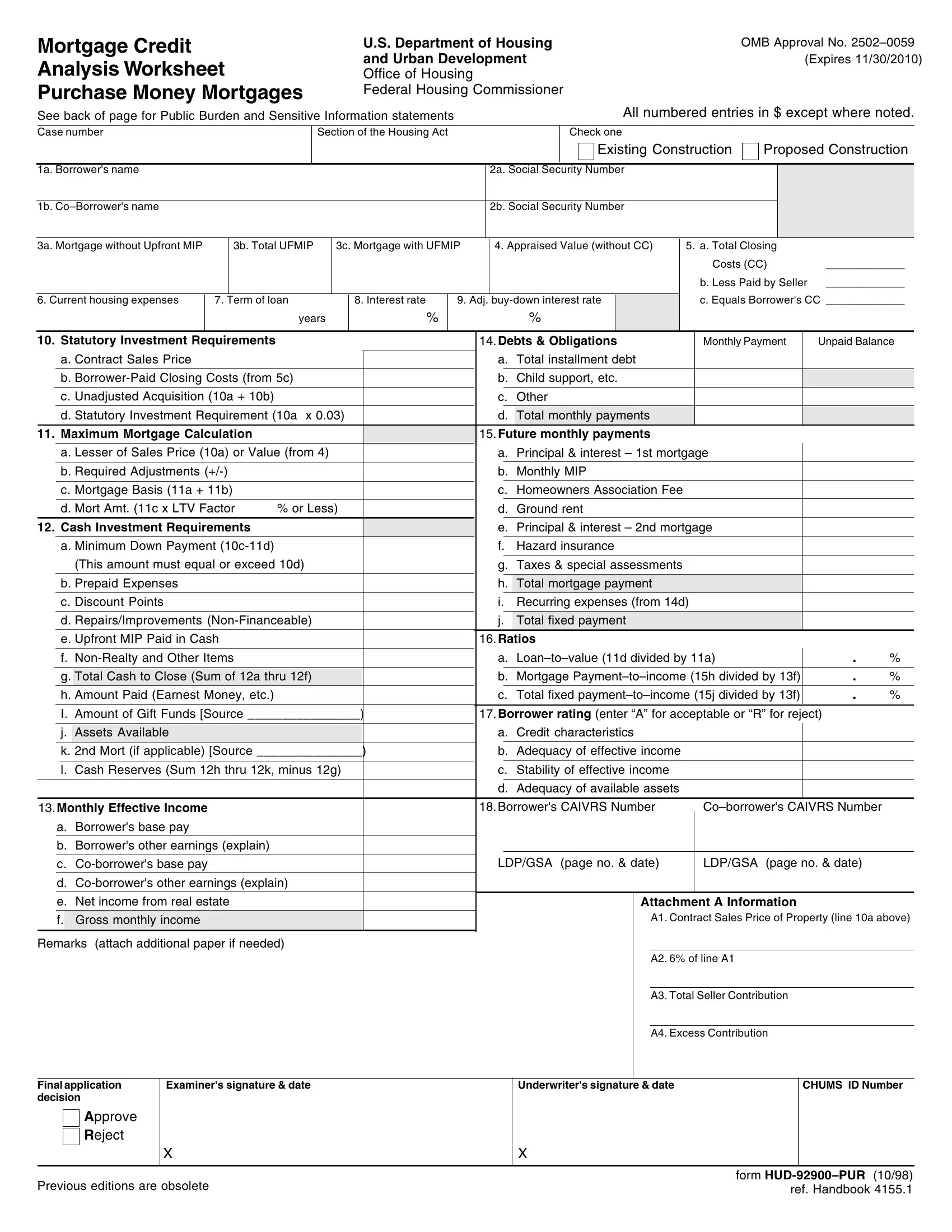

The HUD 92900 PUR form, also known as the Mortgage Credit Analysis Worksheet for Purchase Money Mortgages, plays a critical role in the U.S. home buying process, especially for those leveraging loans guaranteed by the Federal Housing Administration (FHA). Managed by the U.S. Department of Housing and Urban Development (HUD) and intricate in nature, this document is designed to delineate and analyze various financial aspects tied to securing a mortgage. It captures detailed information ranging from the borrower’s personal details and the specifics of the mortgage (including terms, rates, and the loan’s structure) to the property’s appraised value and the buyer's financial obligations. This form is instrumental in assessing the borrower's creditworthiness, ensuring the loan meets HUD's strict lending criteria. It encompasses an array of sections including borrower’s income, future monthly payments, and required cash investment, among others, making it a comprehensive assessment tool for both the lender and borrower. The HUD 92900 PUR form not only facilitates a systematic evaluation to determine eligibility for an FHA loan but also includes provisions for preventing loan fraud, emphasizing the importance of accuracy in the provided information. With its expiration and OMB approval numbers clearly stated, it remains a vital piece of documentation within the housing sector, necessitating careful completion by prospective homeowners and meticulous review by lenders.

| Question | Answer |

|---|---|

| Form Name | Hud 92900 Pur Form |

| Form Length | 7 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 1 min 45 sec |

| Other names | hud 27050 b, form hud 27050 b pdf, hud form 27050 b, OMB |