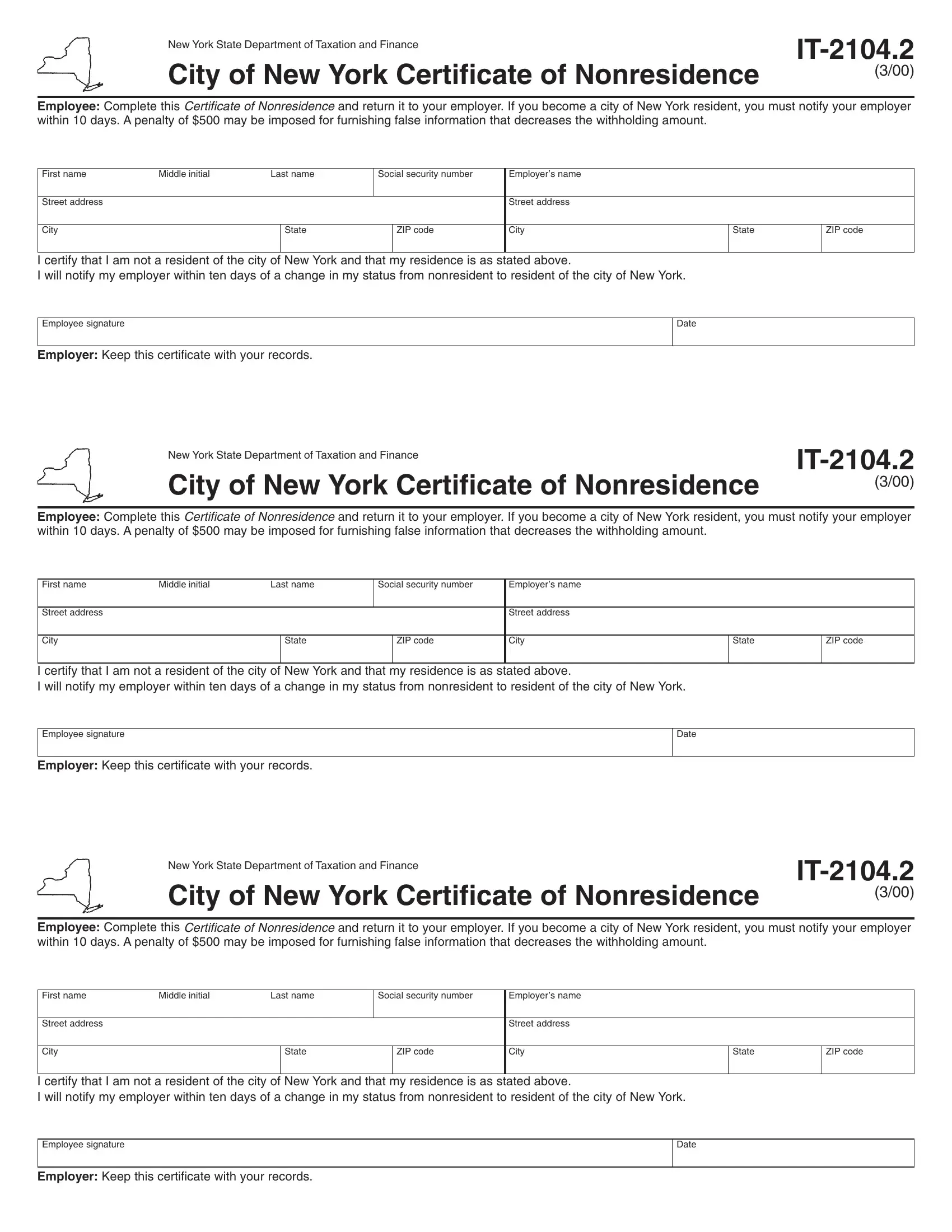

In navigating the complexities of tax requirements, employees and employers in New York City face a distinct set of obligations, particularly when it concerns nonresidency certification. The New York State Department of Taxation and Finance issues the IT-2104.2 form, or the City of New York Certificate of Nonresidence, as a crucial document for those working in the city but residing outside of it. This form serves a dual purpose: it stands as a declaration by the employee of their nonresident status, and it acts as a preventative measure against incorrect tax withholding. Completion and submission of this form to one’s employer are integral steps, demanding attention to resident status changes within a 10-day window to uphold compliance and avoid possible penalties that include a substantial $500 fine for providing false information. The form delves into the specifics of residency determination, heavily relying on the criteria of domicile and permanent place of abode to distinguish residents from nonresidents, along with detailed definitions and exceptions — such as for members of the armed forces or those meeting certain conditions during tax year segments. Moreover, the form emphasizes the legal groundwork behind the collection and usage of personal information, delineating the rights of the Taxation and Finance Department to enforce compliance and the potential repercussions of non-compliance. This furnishes both employees and employers with the guidelines for safeguarding one’s standing under state tax laws, and by extension, underscores the commitment of the state towards maintaining tax fairness and efficiency.

| Question | Answer |

|---|---|

| Form Name | It 2104 2 Form |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | it 2104 form, it 2104 2020 printable, it2104 for 2019, it 2104 |

New York State Department of Taxation and Finance

City of New York Certificate of Nonresidence |

(3/00) |

|

Employee: Complete this Certificate of Nonresidence and return it to your employer. If you become a city of New York resident, you must notify your employer within 10 days. A penalty of $500 may be imposed for furnishing false information that decreases the withholding amount.

First name |

Middle initial |

Last name |

Social security number |

Employer’s name |

|

|

||

|

|

|

|

|

|

|

|

|

Street address |

|

|

|

|

|

Street address |

|

|

|

|

|

|

|

|

|

|

|

City |

|

|

State |

|

ZIP code |

City |

State |

ZIP code |

|

|

|

|

|

|

|

|

|

I certify that I am not a resident of the city of New York and that my residence is as stated above.

I will notify my employer within ten days of a change in my status from nonresident to resident of the city of New York.

Employee signature

Date

Employer: Keep this certificate with your records.

New York State Department of Taxation and Finance

City of New York Certificate of Nonresidence |

(3/00) |

|

Employee: Complete this Certificate of Nonresidence and return it to your employer. If you become a city of New York resident, you must notify your employer within 10 days. A penalty of $500 may be imposed for furnishing false information that decreases the withholding amount.

First name |

Middle initial |

Last name |

Social security number |

Employer’s name |

|

|

||

|

|

|

|

|

|

|

|

|

Street address |

|

|

|

|

|

Street address |

|

|

|

|

|

|

|

|

|

|

|

City |

|

|

State |

|

ZIP code |

City |

State |

ZIP code |

|

|

|

|

|

|

|

|

|

I certify that I am not a resident of the city of New York and that my residence is as stated above.

I will notify my employer within ten days of a change in my status from nonresident to resident of the city of New York.

Employee signature

Date

Employer: Keep this certificate with your records.

New York State Department of Taxation and Finance

City of New York Certificate of Nonresidence |

(3/00) |

|

Employee: Complete this Certificate of Nonresidence and return it to your employer. If you become a city of New York resident, you must notify your employer within 10 days. A penalty of $500 may be imposed for furnishing false information that decreases the withholding amount.

First name |

Middle initial |

Last name |

Social security number |

Employer’s name |

|

|

||

|

|

|

|

|

|

|

|

|

Street address |

|

|

|

|

|

Street address |

|

|

|

|

|

|

|

|

|

|

|

City |

|

|

State |

|

ZIP code |

City |

State |

ZIP code |

|

|

|

|

|

|

|

|

|

I certify that I am not a resident of the city of New York and that my residence is as stated above.

I will notify my employer within ten days of a change in my status from nonresident to resident of the city of New York.

Employee signature

Date

Employer: Keep this certificate with your records.

Resident and Nonresident Defined |

To determine whether or not you are a resident of the city of New York, you must consider your domicile and permanent place of abode. In general, your domicile is the place you intend to have as your permanent home. A permanent place of abode is a residence (a building or structure where a person can live).

If your domicile is New York City, you are a resident unless you meet all three of the conditions in either Group A or Group B:

Group A:

1)You did not maintain any permanent place of abode in New York City during the taxable year; and

2)you maintained a permanent place of abode outside New York City during the entire taxable year; and

3)you spent 30 days or fewer in New York City during the taxable year.

Group B:

same ratio to 90 as the number of days in such portion of the taxable year bears to 548. This condition is illustrated by the following formula:

Number of days in the nonresident portion |

|

|

Maximum number of days |

|

__________________________________ |

x |

90 = |

allowed in New York City |

|

548 |

||||

|

|

|||

|

|

|

You are also a resident if your domicile is not New York City but you maintain a permanent place of abode within New York City and spend 184 days or more in New York City during the taxable year. This rule does not apply to members of the armed forces.

You are a New York City nonresident if you do not meet the above definition of a resident. You are a

Privacy Notification

The right of the Commissioner of Taxation and Finance and the Department of Taxation and Finance to collect and maintain personal information, including mandatory disclosure of social security numbers in the manner required by tax regulations, instructions, and forms, is found in Articles 22, 26,

The Tax Department uses this information primarily to determine and administer tax liabilities due the state and city of New York and the city of Yonkers. We also use this information for certain tax offset and exchange of tax information programs authorized by law, and for any other purpose authorized by law.

1)You were in a foreign country or countries for at least 450 days during any period of 548 consecutive days; and

2)during this period of 548 consecutive days, you did not spend more than 90 days in New York City and you did not maintain a permanent place of abode in New York City at which

your spouse (unless legally separated) or minor children spent more than 90 days; and

3)during the nonresident portion of the taxable year in which the

Information concerning quarterly wages paid to employees and identified by unique random identifying code numbers to preserve the privacy of the employees’ names and social security numbers is provided to certain state agencies, for research purposes to evaluate the effectiveness of certain employment and training programs.

Failure to provide the required information may subject you to civil or criminal penalties, or both, under the Tax Law.

This information is maintained by the Director of the Registration and Data Services Bureau, NYS Tax Department, Building 8 Room 924, W A Harriman Campus, Albany NY 12227; telephone 1 800

Resident and Nonresident Defined |

To determine whether or not you are a resident of the city of New York, you must consider your domicile and permanent place of abode. In general, your domicile is the place you intend to have as your permanent home. A permanent place of abode is a residence (a building or structure where a person can live).

If your domicile is New York City, you are a resident unless you meet all three of the conditions in either Group A or Group B:

Group A:

1)You did not maintain any permanent place of abode in New York City during the taxable year; and

2)you maintained a permanent place of abode outside New York City during the entire taxable year; and

3)you spent 30 days or fewer in New York City during the taxable year.

Group B:

same ratio to 90 as the number of days in such portion of the taxable year bears to 548. This condition is illustrated by the following formula:

Number of days in the nonresident portion |

|

|

Maximum number of days |

|

__________________________________ |

x |

90 = |

allowed in New York City |

|

548 |

||||

|

|

|||

|

|

|

You are also a resident if your domicile is not New York City but you maintain a permanent place of abode within New York City and spend 184 days or more in New York City during the taxable year. This rule does not apply to members of the armed forces.

You are a New York City nonresident if you do not meet the above definition of a resident. You are a

Privacy Notification

The right of the Commissioner of Taxation and Finance and the Department of Taxation and Finance to collect and maintain personal information, including mandatory disclosure of social security numbers in the manner required by tax regulations, instructions, and forms, is found in Articles 22, 26,

The Tax Department uses this information primarily to determine and administer tax liabilities due the state and city of New York and the city of Yonkers. We also use this information for certain tax offset and exchange of tax information programs authorized by law, and for any other purpose authorized by law.

1)You were in a foreign country or countries for at least 450 days during any period of 548 consecutive days; and

2)during this period of 548 consecutive days, you did not spend more than 90 days in New York City and you did not maintain a permanent place of abode in New York City at which

your spouse (unless legally separated) or minor children spent more than 90 days; and

3)during the nonresident portion of the taxable year in which the

Information concerning quarterly wages paid to employees and identified by unique random identifying code numbers to preserve the privacy of the employees’ names and social security numbers is provided to certain state agencies, for research purposes to evaluate the effectiveness of certain employment and training programs.

Failure to provide the required information may subject you to civil or criminal penalties, or both, under the Tax Law.

This information is maintained by the Director of the Registration and Data Services Bureau, NYS Tax Department, Building 8 Room 924, W A Harriman Campus, Albany NY 12227; telephone 1 800

Resident and Nonresident Defined |

To determine whether or not you are a resident of the city of New York, you must consider your domicile and permanent place of abode. In general, your domicile is the place you intend to have as your permanent home. A permanent place of abode is a residence (a building or structure where a person can live).

If your domicile is New York City, you are a resident unless you meet all three of the conditions in either Group A or Group B:

Group A:

1)You did not maintain any permanent place of abode in New York City during the taxable year; and

2)you maintained a permanent place of abode outside New York City during the entire taxable year; and

3)you spent 30 days or fewer in New York City during the taxable year.

Group B:

same ratio to 90 as the number of days in such portion of the taxable year bears to 548. This condition is illustrated by the following formula:

Number of days in the nonresident portion |

|

|

Maximum number of days |

|

__________________________________ |

x |

90 = |

allowed in New York City |

|

548 |

||||

|

|

|||

|

|

|

You are also a resident if your domicile is not New York City but you maintain a permanent place of abode within New York City and spend 184 days or more in New York City during the taxable year. This rule does not apply to members of the armed forces.

You are a New York City nonresident if you do not meet the above definition of a resident. You are a

Privacy Notification

The right of the Commissioner of Taxation and Finance and the Department of Taxation and Finance to collect and maintain personal information, including mandatory disclosure of social security numbers in the manner required by tax regulations, instructions, and forms, is found in Articles 22, 26,

The Tax Department uses this information primarily to determine and administer tax liabilities due the state and city of New York and the city of Yonkers. We also use this information for certain tax offset and exchange of tax information programs authorized by law, and for any other purpose authorized by law.

1)You were in a foreign country or countries for at least 450 days during any period of 548 consecutive days; and

2)during this period of 548 consecutive days, you did not spend more than 90 days in New York City and you did not maintain a permanent place of abode in New York City at which

your spouse (unless legally separated) or minor children spent more than 90 days; and

3)during the nonresident portion of the taxable year in which the

Information concerning quarterly wages paid to employees and identified by unique random identifying code numbers to preserve the privacy of the employees’ names and social security numbers is provided to certain state agencies, for research purposes to evaluate the effectiveness of certain employment and training programs.

Failure to provide the required information may subject you to civil or criminal penalties, or both, under the Tax Law.

This information is maintained by the Director of the Registration and Data Services Bureau, NYS Tax Department, Building 8 Room 924, W A Harriman Campus, Albany NY 12227; telephone 1 800