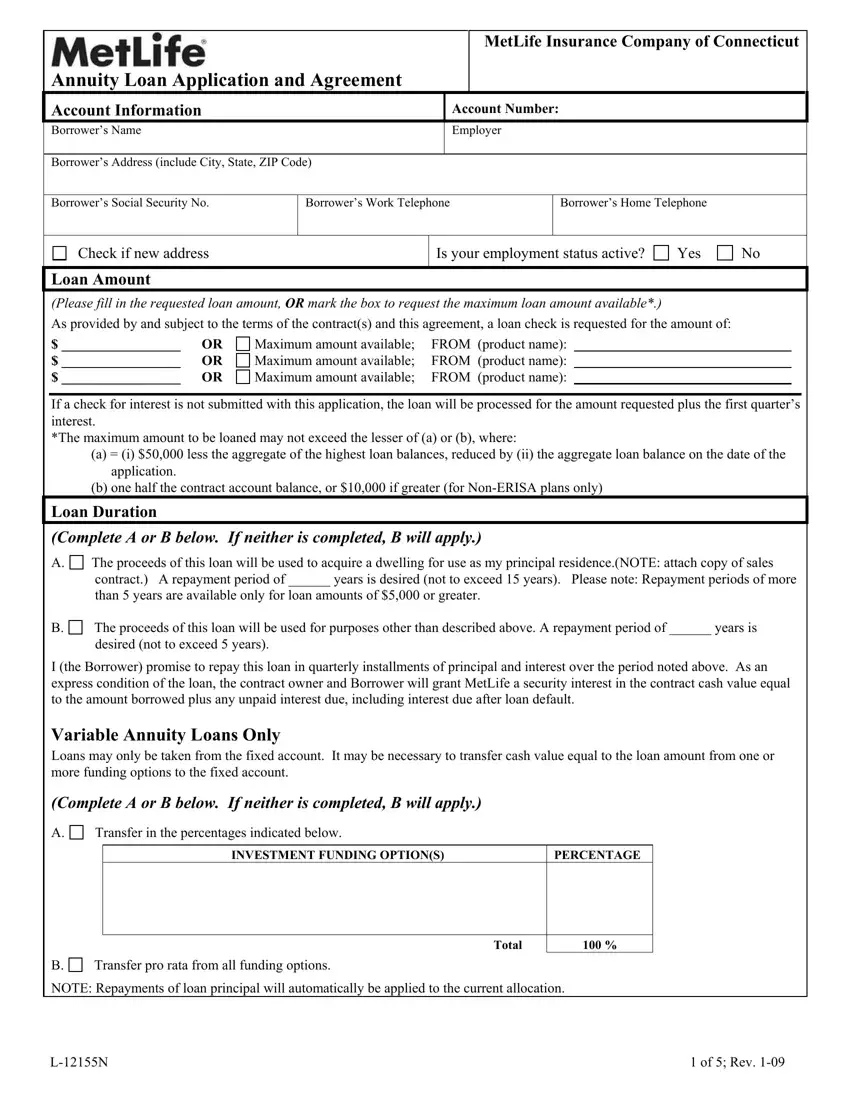

The MetLife Insurance Company of Connecticut Annuity Loan Application and Agreement is a document designed for borrowers seeking a loan against the value of their annuity contract. It captures essential details including borrower's information, employment status, loan amount request, and purpose of the loan, with specific sections dedicated to both general use and purchasing a principal residence. Notably, the form delineates the terms for loan amount eligibility, addressing maximum loan amounts relative to the borrower's contract account balance and adhering to stipulated legal thresholds to prevent exceeding permissible limits. It offers a choice between a fixed loan duration varying from one to fifteen years based on the loan's purpose, and outlines the conditions under which cash value from employer contributions can secure the loan, crucial for understanding the financial implications and responsibilities involved. Additionally, it encompasses a detailed section on the procedure for loan default, emphasizing the tax implications and the process for remedying a default. The form also includes provisions for spousal consent in alignment with ERISA plans, ensuring compliance with federal regulations pertaining to retirement accounts. This comprehensive document concludes with specific instructions for submission, aiming to facilitate a smooth application process for borrowers while ensuring adherence to relevant regulatory and contractual stipulations.

| Question | Answer |

|---|---|

| Form Name | Metlife Annuity Loan Application |

| Form Length | 5 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 1 min 15 sec |

| Other names | metlife 403 b loan request form, metlife retirement loan application, metlife annuity loan, metlife loan request form |