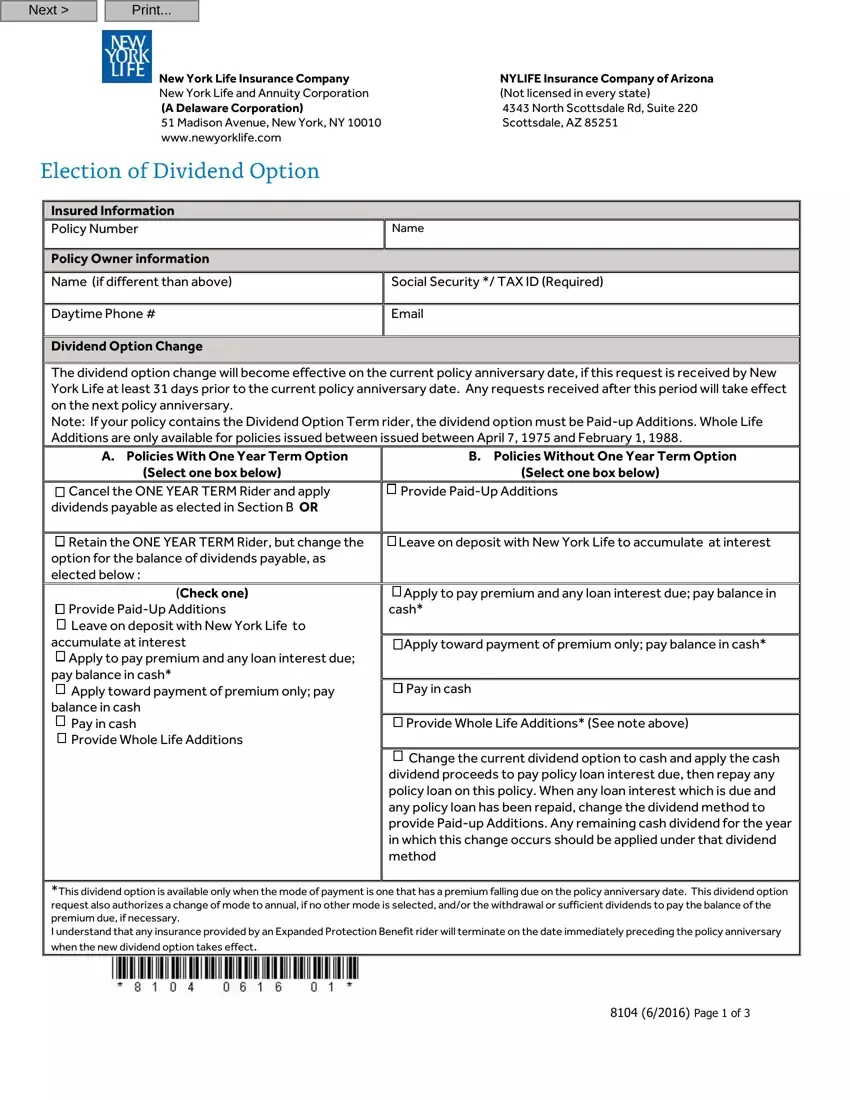

The New York 8104 form plays a pivotal role for policyholders with New York Life Insurance Company and its affiliates, encompassing an array of requests and changes pertaining to the policyholder's dividend options and income tax withholding preferences. This comprehensive form addresses the intricacies of managing dividend options, which can include alterations to how dividends are received or applied — such as opting for cash payments, applying dividends to premium payments, or investing in paid-up additions. Particularly noteworthy is the consideration given to policies with the Dividend Option Term rider, necessitating the selection of paid-up additions for these policies. Additionally, the form delves into the crucial area of tax compliance, mandating policyholders to make informed decisions about federal and state income tax withholdings. This decision is significantly influenced by the policyholder's citizenship status and whether or not they have been subject to or are currently exempt from backup withholding. The form serves as a testament to the nuanced relationship between insurance policy management and tax obligations, urging policyholders to consult with tax advisors to navigate these complexities. Importantly, it underscores the regulatory requirement to furnish social security or taxpayer identification numbers to avert obligatory withholding by the IRS, thus intertwining financial management with legal compliance in the context of life insurance.

| Question | Answer |

|---|---|

| Form Name | New York Form 8104 |

| Form Length | 3 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 45 sec |

| Other names | 81040108 new york life insurance forms election of dividend option |