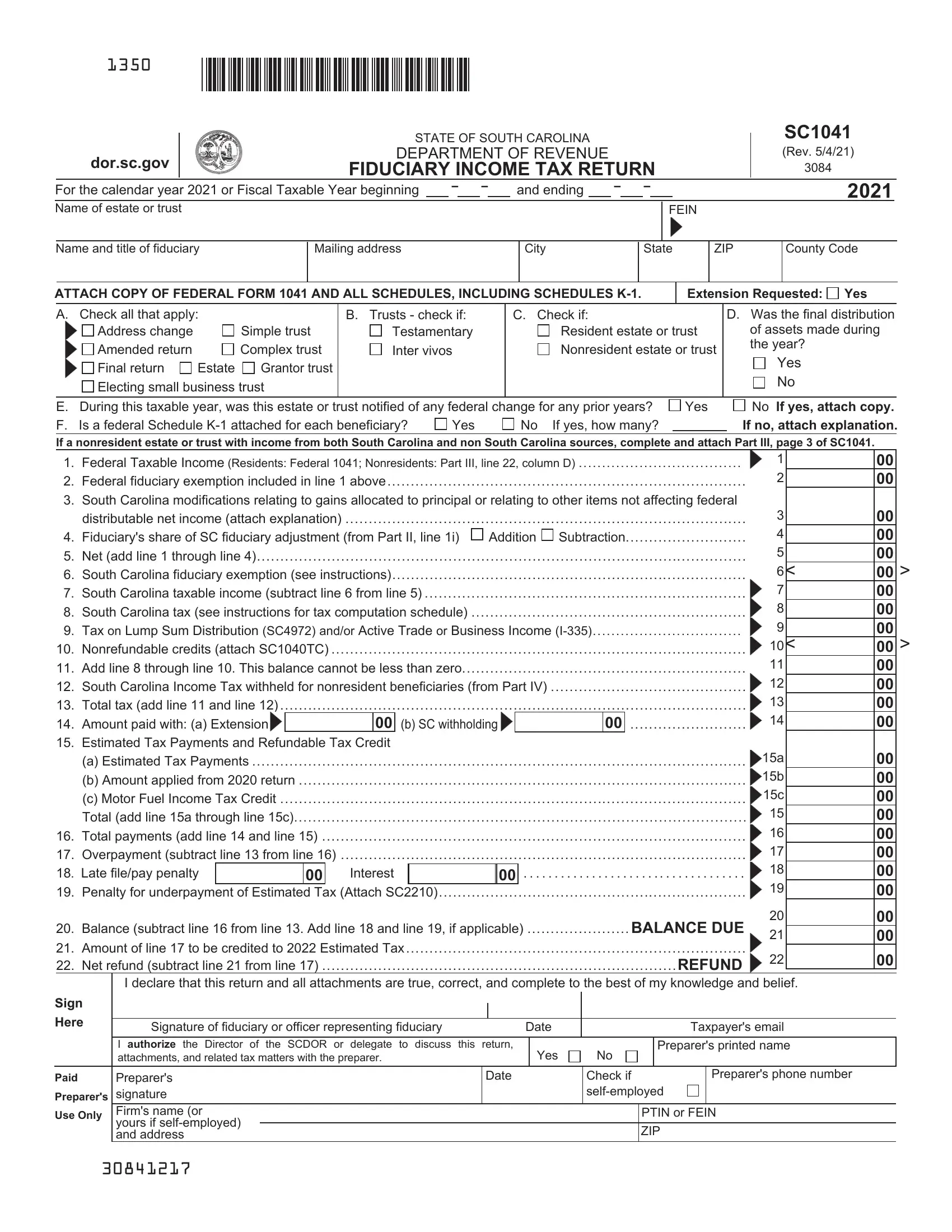

Navigating the complexities of fiduciary income tax returns can be challenging for estates and trusts in South Carolina. The SC 1041 form, as revised on July 15, 2020, provides a structured framework for reporting income, deductions, and taxes due for both resident and nonresident entities for the fiscal year or calendar year 2020. It mandates the inclusion of the federal Form 1041 alongside all relevant schedules, ensuring that the state's Department of Revenue has a comprehensive view of the fiduciary's financial activities. Beyond its basic reporting function, the form delves into specifications such as estate or trust type, residency status, and the intricate details of income sources and modifications specific to South Carolina law. The form accommodates for various adjustments to federal taxable income, caters to nonresident estates or trusts with South Carolina sources of income, and requires detailed beneficiary reporting. This introduction to the SC 1041 form outlines the necessity for meticulous attention to detail and an understanding of both federal and state tax obligations, underscoring the importance of accuracy and compliance in fiduciary income tax filing.

| Question | Answer |

|---|---|

| Form Name | Sc Form 1041 |

| Form Length | 11 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 2 min 45 sec |

| Other names | sc 1041 tax form, sc1041, sc form sc1041, how to south carolina fiduciary |