Our top rated web programmers have worked together to make the PDF editor that you're going to make use of. The software makes it simple to fill out st125 forms shortly and conveniently. This is everything you need to undertake.

Step 1: Click the "Get Form Here" button.

Step 2: You're now on the form editing page. You can edit, add information, highlight specific words or phrases, insert crosses or checks, and add images.

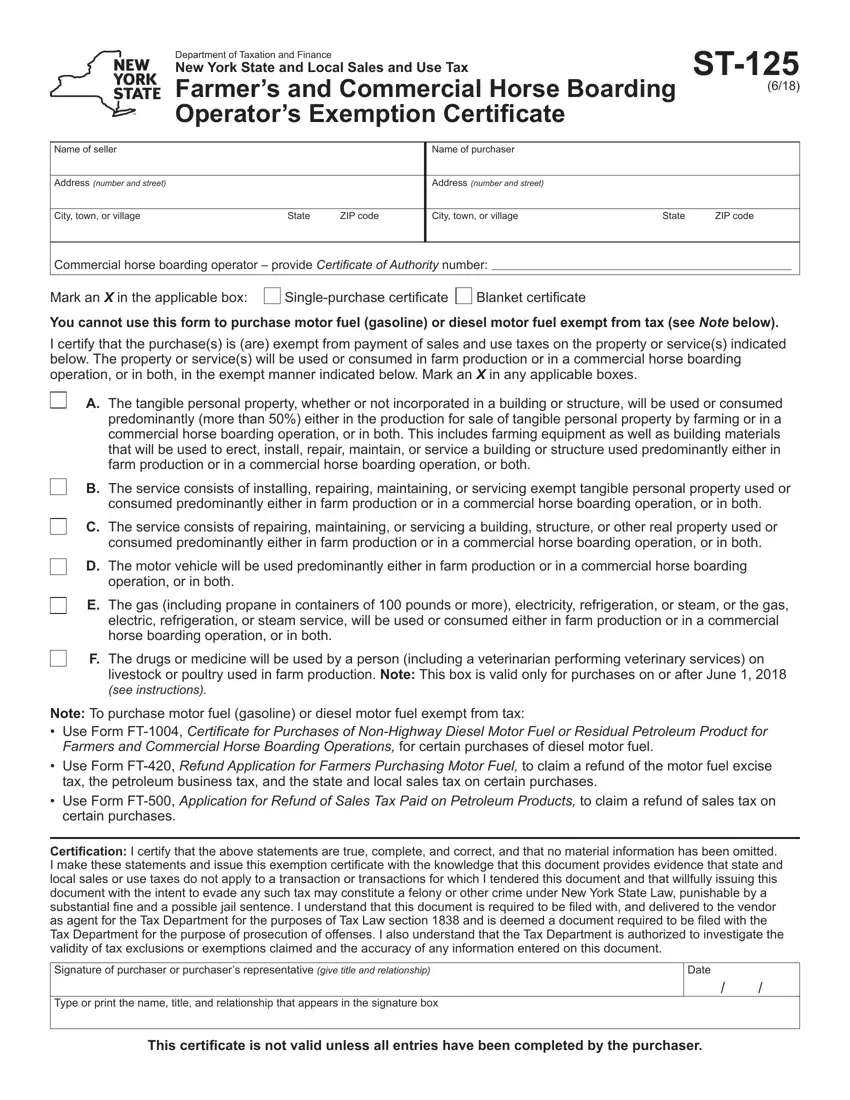

Enter the necessary data in every single area to fill in the PDF st125

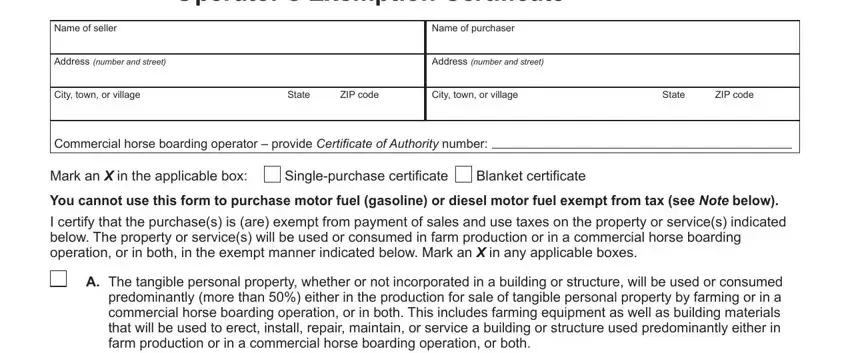

Add the demanded details in the B The service consists of, C The service consists of, D The motor vehicle will be used, operation or in both, E The gas including propane in, F The drugs or medicine will be, livestock or poultry used in farm, Note To purchase motor fuel, tax the petroleum business tax and, Use Form FT Application for, and Certiication I certify that the segment.

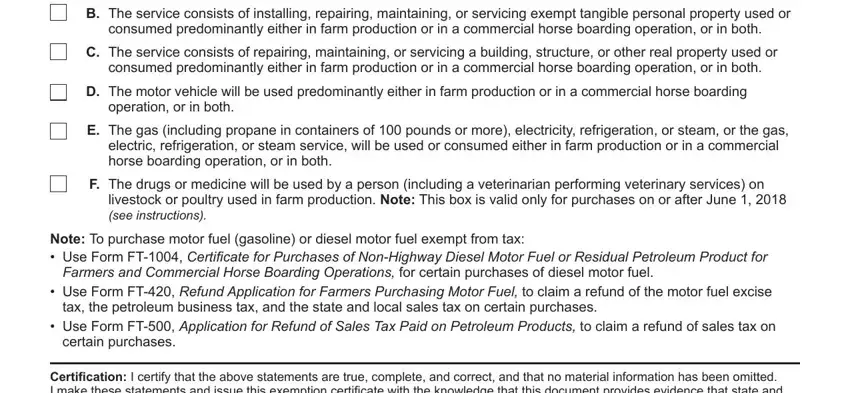

The software will ask you for particulars to automatically complete the area Certiication I certify that the, Signature of purchaser or, Type or print the name title and, Date, and This certiicate is not valid.

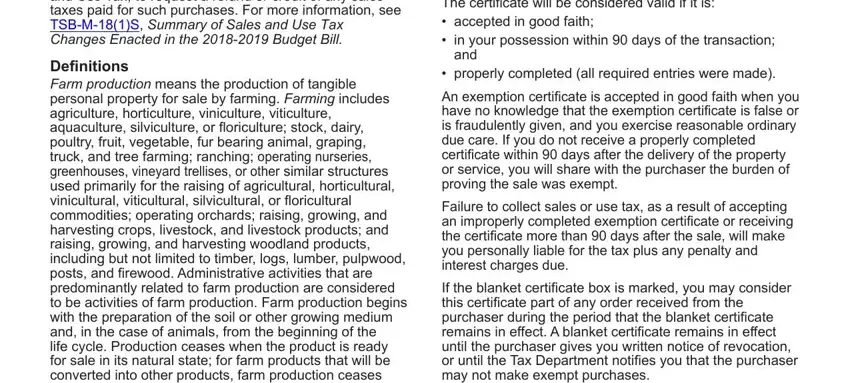

The New Box F Effective June mark, Deinitions Farm production means, As a New York State registered, and, properly completed all required, An exemption certiicate is, Failure to collect sales or use, and If the blanket certiicate box is section is going to be place to put the rights and responsibilities of all parties.

Step 3: After you choose the Done button, your finalized file can be easily exported to any of your gadgets or to electronic mail indicated by you.

Step 4: You should make as many copies of the file as you can to stay away from future misunderstandings.