We used the top programmers to set-up the PDF editor. This software will let you complete the sun trust subordination acknowledgement and agreement document with no trouble and won't eat up a lot of your energy. This simple guideline will let you start out.

Step 1: Select the "Get Form Now" button to begin.

Step 2: After you've entered your sun trust subordination acknowledgement and agreement edit page, you'll discover all actions you may take concerning your document at the top menu.

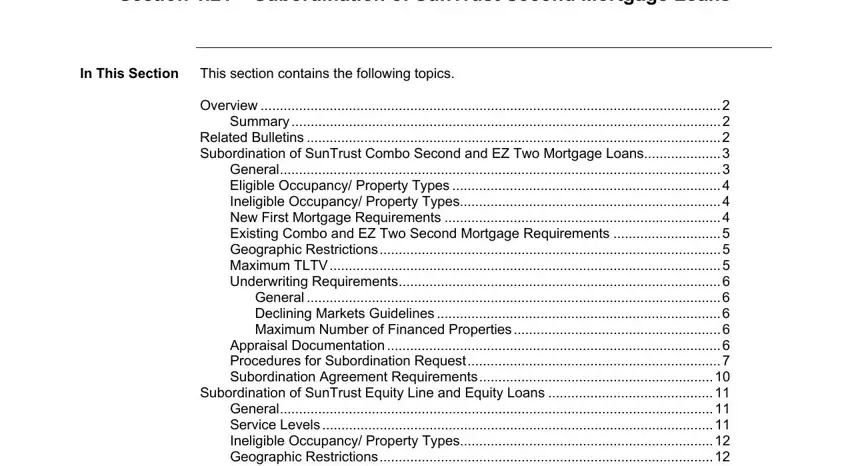

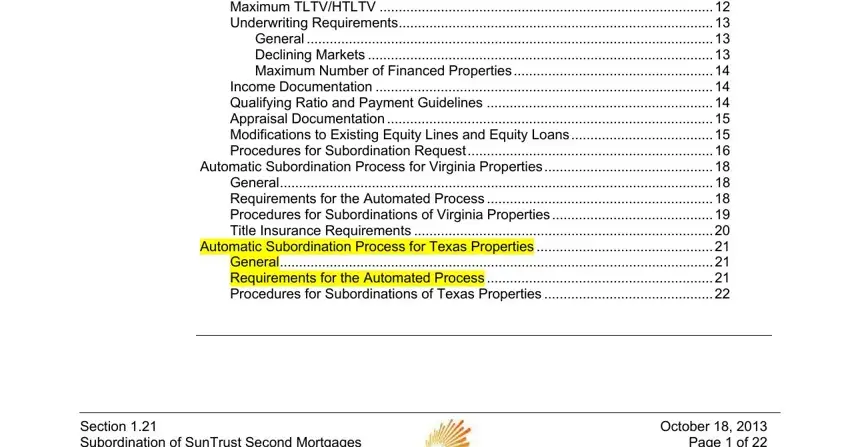

The PDF document you are about to fill in will contain the next segments:

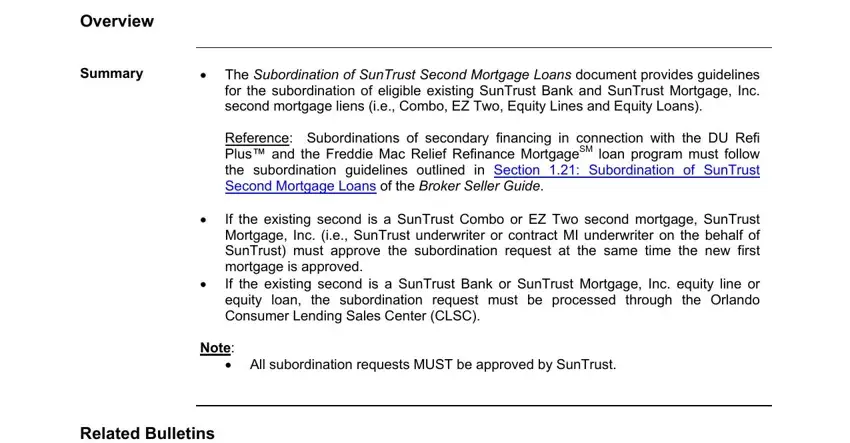

Provide the demanded particulars in the Overview Summary Related, Section Subordination of SunTrust, and October Page of area.

Note all particulars you may need inside the area Overview, Summary, The Subordination of SunTrust, Reference Subordinations of, If the existing second is a, Note, All subordination requests MUST, and Related Bulletins.

The Related bulletins are provided, Section Subordination of SunTrust, and October Page of area will be the place to indicate the rights and obligations of each side.

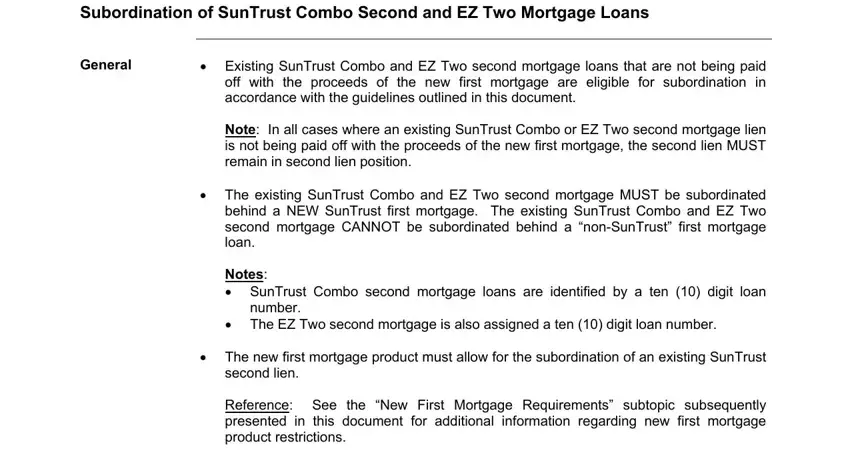

Finalize by looking at the next areas and submitting the relevant details: Subordination of SunTrust Combo, General, Existing SunTrust Combo and EZ, Note In all cases where an, The existing SunTrust Combo and, Notes SunTrust Combo second, number, The EZ Two second mortgage is, The new first mortgage product, second lien, and Reference See the New First.

Step 3: When you pick the Done button, the final document is easily exportable to any type of of your devices. Or, you can easily send it by using mail.

Step 4: In order to prevent any specific concerns down the road, you will need to get up to two or three copies of your file.