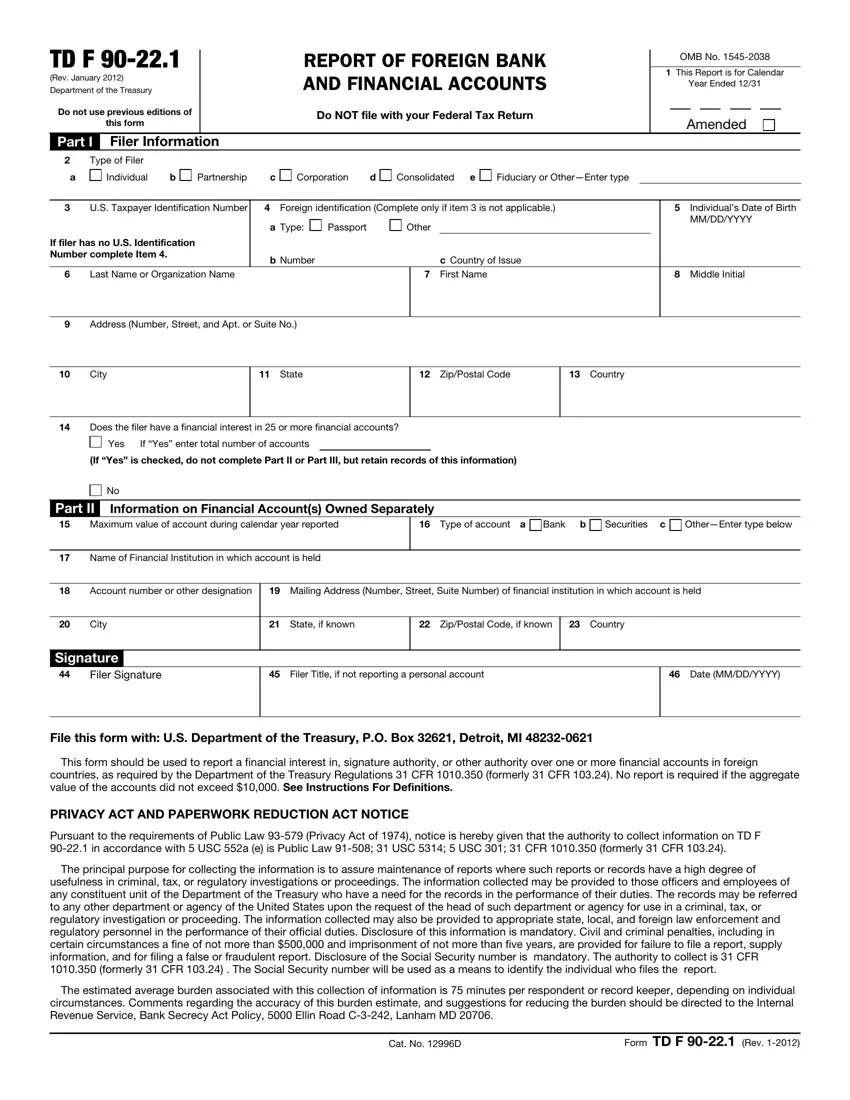

The Form TD F 90-22.1, known as the Report of Foreign Bank and Financial Accounts (FBAR), plays a crucial role in ensuring U.S. persons comply with the United States Department of the Treasury's regulations concerning foreign financial accounts. This requirement, which underwent revision in January 2012, mandates the reporting of financial interest, signature authority, or other forms of control over foreign bank and financial accounts if the aggregate value of those accounts exceeded $10,000 at any point during the calendar year. Designed not to be filed with the federal tax return but rather sent directly to the address indicated by the Department of the Treasury, it encompasses various types of filers, including individuals, corporations, partnerships, and others. The form gathers detailed information about the accounts being reported, such as maximum values during the reported year, types of accounts, account numbers, and details regarding the financial institutions where these accounts are held. It also contains sections for reporting accounts owned jointly, where the filer has signature authority but no financial interest, and for consolidated reporting in certain cases. Submitting this form is critical as failure to do so can result in severe civil and criminal penalties. Additionally, it emphasizes the importance of transparency in financial matters, aiding regulatory and law enforcement agencies in their efforts to prevent financial crimes. With privacy and Paperwork Reduction Acts notices included, filers are informed about their rights, the mandatory disclosure of their Social Security number, and the intended use of their information, aiming to balance the requirement for financial transparency with individual privacy rights.

| Question | Answer |

|---|---|

| Form Name | Td F 90 22 1 |

| Form Length | 8 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 2 min |

| Other names | td f 90 22 1, irs bank account, td f bank, td f 90 22 1 form |