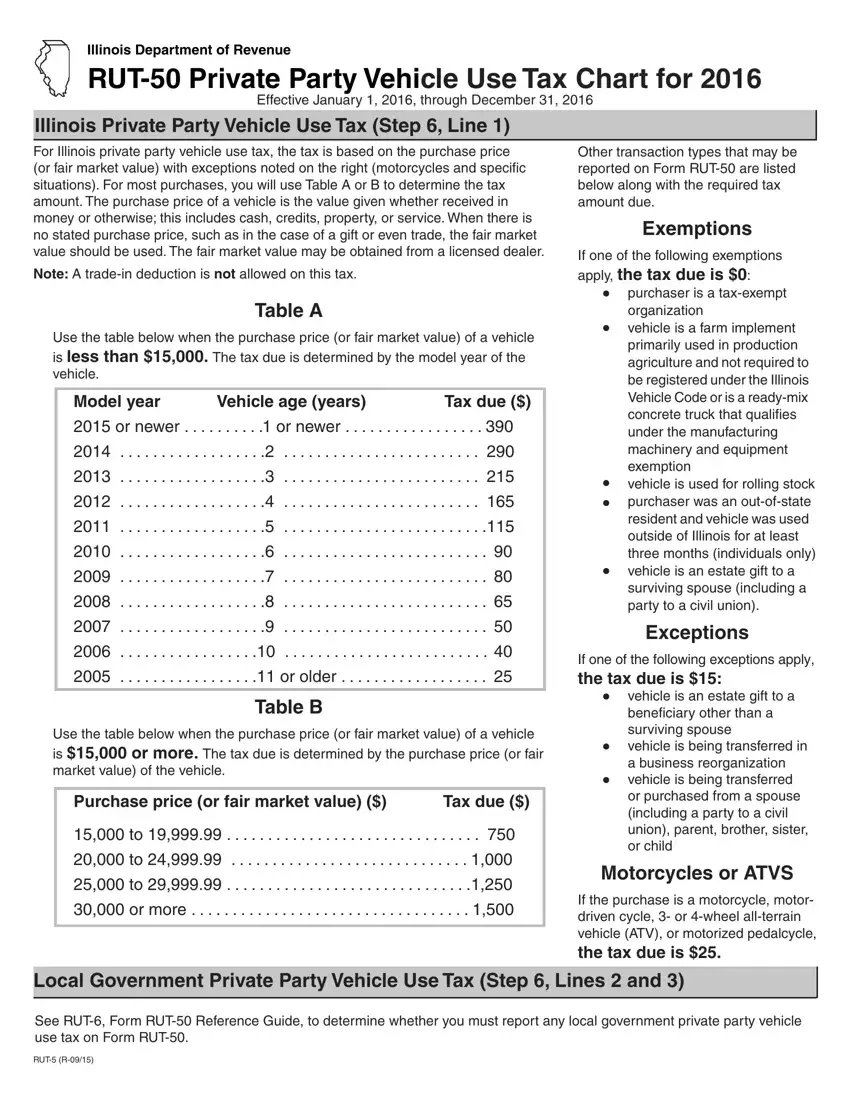

When it comes down to purchasing a vehicle in Illinois from a private party, a crucial piece of paperwork that comes into play is the Illinois Department of Revenue RUT-50 form. Effective from January 1, 2016, this form helps calculate the private party vehicle use tax that needs to be paid based on the purchase price or the fair market value of the vehicle, with certain exceptions such as motorcycles and specific situations clearly outlined. It's an essential document that ensures transactions are taxed appropriately, distinguishing between different cases through Tables A and B for determining the tax amount due depending on whether the vehicle's purchase price is below or above $15,000. Moreover, the form also provides guidance on transaction types that may be exempt from tax or qualify for a reduced tax rate under specific conditions, including vehicles transferred as an estate gift or purchased by tax-exempt organizations. Additionally, for those buying or receiving vehicles as estates or through business reorganizations, or in transactions between close family members, the form elaborates on the tax implications and the necessary dues. Understanding the RUT-50 form is indispensable for navigating these transactions smoothly and ensuring compliance with Illinois tax laws.

| Question | Answer |

|---|---|

| Form Name | Tax Form Rut 50 |

| Form Length | 1 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 15 sec |

| Other names | rut 50 sample, rut 50 illinois, illinois rut 50 form, illinois form rut 50 |