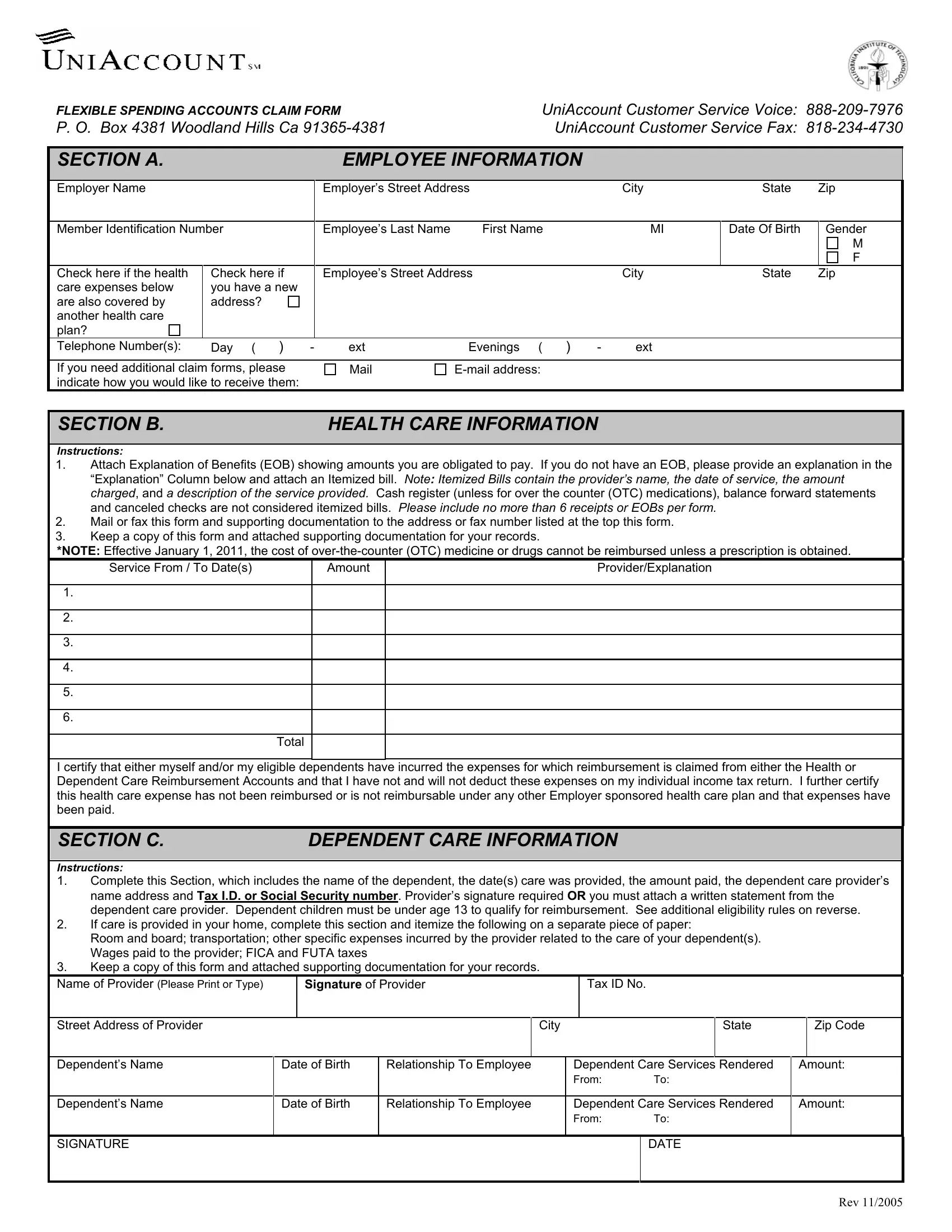

In today's fast-paced world, managing healthcare and dependent care expenses becomes a crucial part of financial planning for many individuals and families. Recognizing this need, the UniAccount Flexible Spending Accounts Claim Form provides a structured way for employees to claim reimbursements for eligible expenses. With customer service support via phone and fax, the form is designed to streamline the process, making it less daunting for users. Participants are required to fill in personal information and detail their healthcare or dependent care expenses, adhering to instructions provided for documentation. Notably, the form emphasizes the importance of attaching Explanation of Benefits (EOB) or itemized bills to support claims. For healthcare expenses, it highlights a significant update regarding over-the-counter (OTC) medication reimbursements post-January 1, 2011 – requiring a prescription to qualify. In the realm of dependent care, it outlines eligibility rules and necessary documentation, aiming to ensure that claims are justified and in compliance with IRS guidelines. The summary sections for both healthcare and dependent care expenses offer a glance at common reimbursable expenses, guiding users through the often-complex landscape of eligible claims. This detailed approach underlines the necessity for accurate and thorough documentation, ensuring that only legitimate expenses are reimbursed, thereby maintaining the integrity and purpose of the Flexible Spending Account (FSA) program.

| Question | Answer |

|---|---|

| Form Name | Uniaccount Claim Form |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | uniaccount flexible spending form, uniaccount claim form, uniaccount fsa anthem com, anthem bcbs retiree uniaccount claim form |