Navigating the intricacies of rental income and its impact on investment properties can be a complex process, yet it's made more accessible with the detailed guidelines provided by Fannie Mae's Form 1039. This form serves as a vital tool for individuals and businesses alike, aiming to accurately report and evaluate rental income derived from investment properties. At its core, the form breaks down into essential segments requiring documentation such as IRS Form 8825 or lease agreements, along with a thorough analysis of the property's financial performance, taking into account gross rents received, various allowable deductions, and the all-important calculation of monthly property cash flow. Whether utilizing the detailed method via IRS Form 8825 related to entities like IRS Form 1065 or 1120S, or the straightforward approach with a lease agreement, the form meticulously guides users through a step-by-step process. This involves determining the property's in-service duration, calculating adjusted rental income, and ultimately assessing the qualifying impact of the mortgaged investment property PITIA (Principal, Interest, Taxes, Insurance, and Association dues) expense on the borrower's debt-to-income ratio. Furthermore, it addresses both subject and non-subject properties in refinancing and rental contexts, ensuring a comprehensive evaluation. The Form 1039, updated as of September 30, 2014, not only facilitates the calculation of an offset to the monthly PITIA but also outlines the criteria for incorporating any net income into the borrower's qualifying income, adhering to specific history requirements as detailed in the Selling Guide, thus providing a structured pathway for managing rental income effectively.

| Question | Answer |

|---|---|

| Form Name | 1039 Form |

| Form Length | 1 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 15 sec |

| Other names | fannie 1039, fannie form 1039, 1039 tax form, fnma form 1039 |

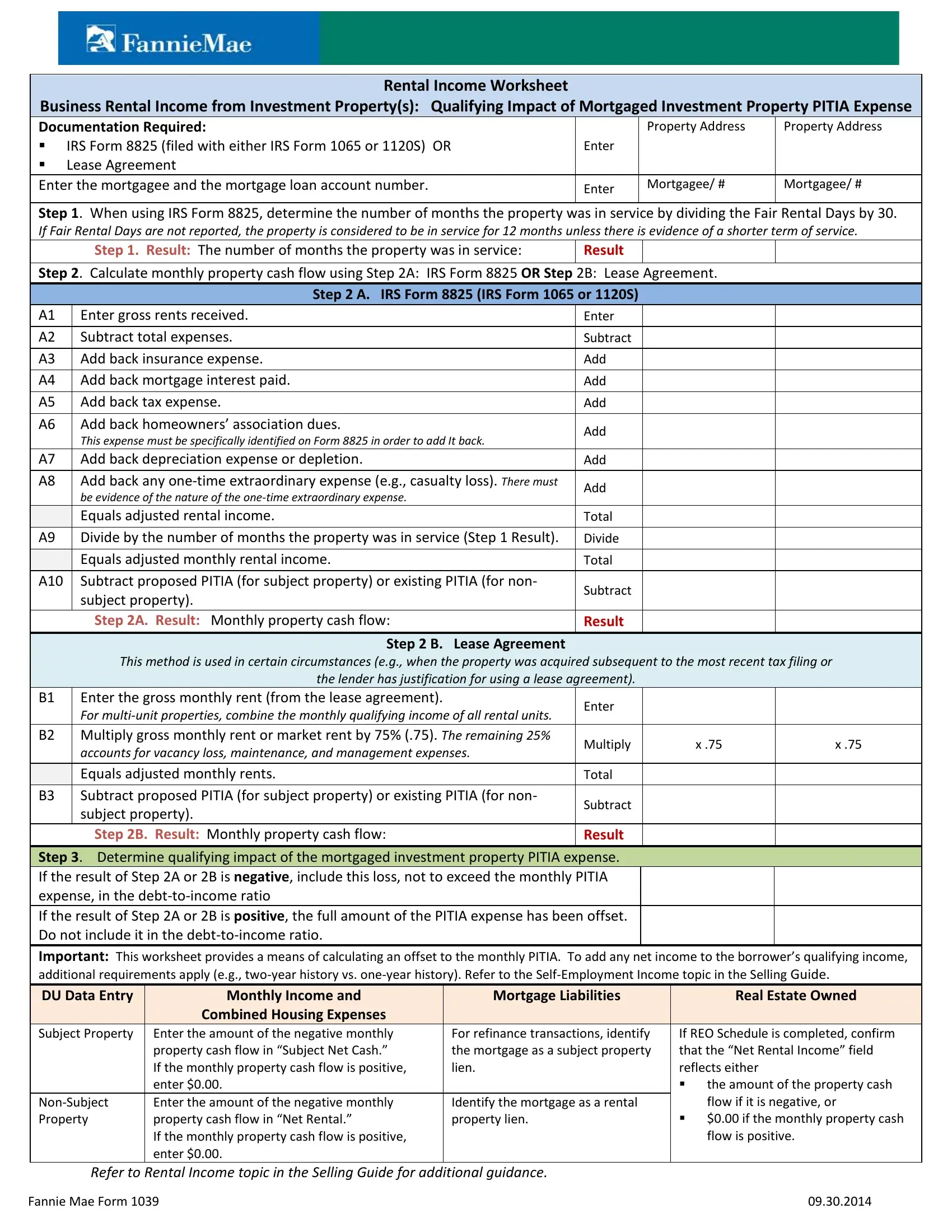

Rental Income Worksheet

Business Rental Income from Investment Property(s): Qualifying Impact of Mortgaged Investment Property PITIA Expense

Documentation Required: |

Property Address |

Property Address |

IRS Form 8825 (filed with either IRS Form 1065 or 1120S) OR |

Enter |

|

Lease Agreement

Enter the mortgagee and the mortgage loan account number. |

Enter |

Mortgagee/ # |

Mortgagee/ # |

|

|

|

Step 1. When using IRS Form 8825, determine the number of months the property was in service by dividing the Fair Rental Days by 30.

If Fair Rental Days are not reported, the property is considered to be in service for 12 months unless there is evidence of a shorter term of service.

Step 1. Result: The number of months the property was in service: |

Result |

|

|

|

|

|

|

Step 2. Calculate monthly property cash flow using Step 2A: IRS Form 8825 OR Step 2B: Lease Agreement.

Step 2 A. IRS Form 8825 (IRS Form 1065 or 1120S)

A1 |

Enter gross rents received. |

Enter |

|

|

|

A2 |

Subtract total expenses. |

Subtract |

|

|

|

A3 |

Add back insurance expense. |

Add |

|

|

|

A4 |

Add back mortgage interest paid. |

Add |

|

|

|

A5 |

Add back tax expense. |

Add |

|

|

|

A6 |

Add back homeowners’ association dues. |

Add |

|

This expense must be specifically identified on Form 8825 in order to add It back. |

|

|

|

|

A7 |

Add back depreciation expense or depletion. |

Add |

|

|

|

A8 |

Add back any |

Add |

|

|

be evidence of the nature of the

|

Equals adjusted rental income. |

Total |

A9 |

Divide by the number of months the property was in service (Step 1 Result). |

Divide |

|

Equals adjusted monthly rental income. |

Total |

A10 |

Subtract proposed PITIA (for subject property) or existing PITIA (for non- |

Subtract |

|

subject property). |

|

|

|

Step 2A. Result: Monthly property cash flow: |

Result |

Step 2 B. Lease Agreement

This method is used in certain circumstances (e.g., when the property was acquired subsequent to the most recent tax filing or

the lender has justification for using a lease agreement).

B1 |

Enter the gross monthly rent (from the lease agreement). |

Enter |

|

|

|

For |

|

|

|

|

|

|

|

|

B2 |

Multiply gross monthly rent or market rent by 75% (.75). The remaining 25% |

Multiply |

x .75 |

x .75 |

|

accounts for vacancy loss, maintenance, and management expenses. |

|||

|

|

|

|

|

|

Equals adjusted monthly rents. |

Total |

|

|

B3 |

Subtract proposed PITIA (for subject property) or existing PITIA (for non- |

Subtract |

|

|

|

subject property). |

|

|

|

|

|

|

|

Step 2B. Result: Monthly property cash flow: |

Result |

Step 3. Determine qualifying impact of the mortgaged investment property PITIA expense.

If the result of Step 2A or 2B is negative, include this loss, not to exceed the monthly PITIA expense, in the

If the result of Step 2A or 2B is positive, the full amount of the PITIA expense has been offset.

Do not include it in the

Important: This worksheet provides a means of calculating an offset to the monthly PITIA. To add any net income to the borrower’s qualifying income, additional requirements apply (e.g.,

|

DU Data Entry |

Monthly Income and |

Mortgage Liabilities |

|

|

Real Estate Owned |

|

|

Combined Housing Expenses |

|

|

|

|

|

Subject Property |

Enter the amount of the negative monthly |

For refinance transactions, identify |

|

If REO Schedule is completed, confirm |

|

|

|

property cash flow in “Subject Net Cash.” |

the mortgage as a subject property |

|

that the “Net Rental Income” field |

|

|

|

If the monthly property cash flow is positive, |

lien. |

|

reflects either |

|

|

|

enter $0.00. |

|

|

the amount of the property cash |

|

|

Enter the amount of the negative monthly |

Identify the mortgage as a rental |

|

|

flow if it is negative, or |

|

|

Property |

property cash flow in “Net Rental.” |

property lien. |

|

$0.00 if the monthly property cash |

|

|

|

If the monthly property cash flow is positive, |

|

|

|

flow is positive. |

|

|

enter $0.00. |

|

|

|

|

|

Refer to Rental Income topic in the Selling Guide for additional guidance. |

|

|

|

||

Fannie Mae Form 1039 |

|

09.30.2014 |

||||