Who Needs BIR Form 2307

Any business or individual in the Philippines that withholds taxes from payments must issue this form. This includes companies that pay freelancers, contractors, or suppliers for services subject to expanded withholding tax (EWT). The payor (the entity making the payment) fills out the form and gives it to the payee (the recipient). If you receive income from clients who deduct withholding tax before paying you, you should receive a copy as proof of your tax credits.

How to Fill Out BIR Form 2307 Online

You can fill out this form using our online PDF editor. Click the "Get Form" button above to open it in the editor, then follow these steps.

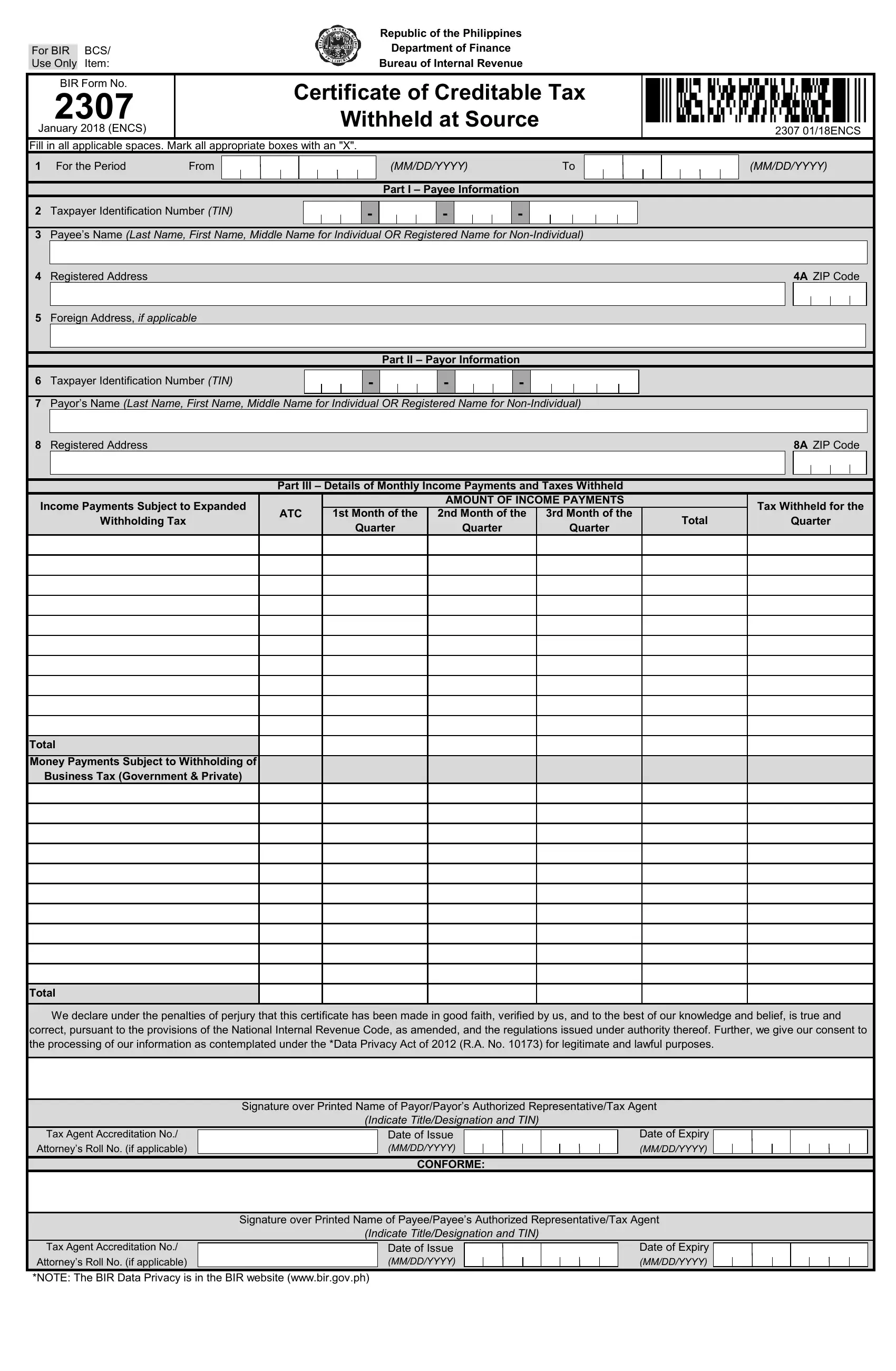

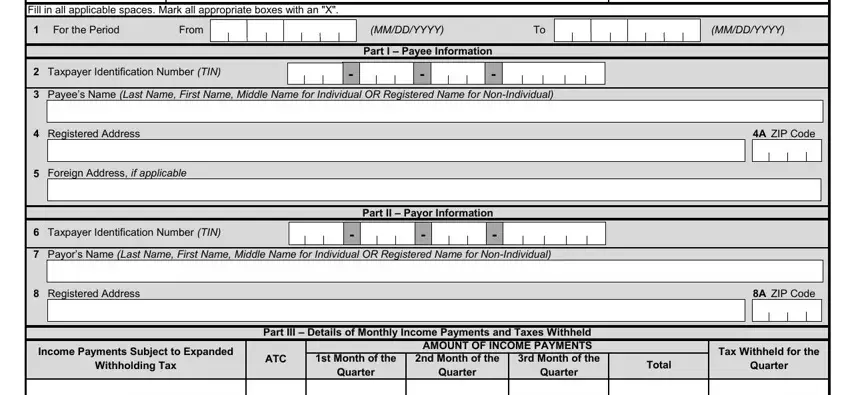

1. Enter the reporting period at the top. Write the start and end dates for the month or quarter the form covers.

2. Complete the payee information in Part I. Provide the payee's TIN, registered name, address, and zip code. For businesses, use the name registered with the BIR. Then fill in the payor details in Part II with the payor's TIN, registered name, and address. Verify these against your BIR Certificate of Registration (BIR Form 0605).

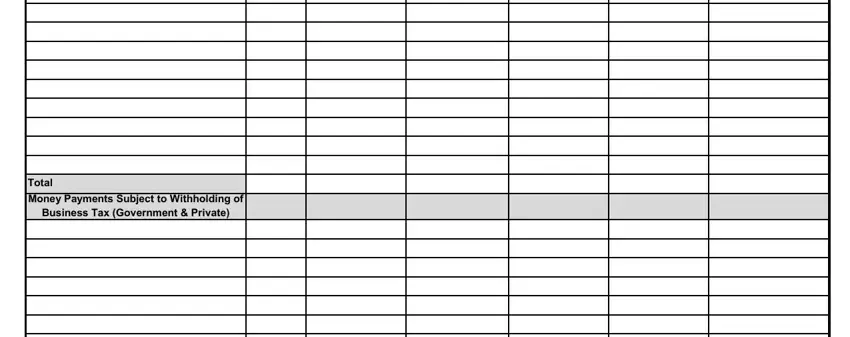

3. Record the income payments and taxes withheld in the Schedule section. List each type of payment using the correct Alphanumeric Tax Code (ATC), the monthly gross income amounts, and the tax rate applied. Double-check all amounts before continuing.

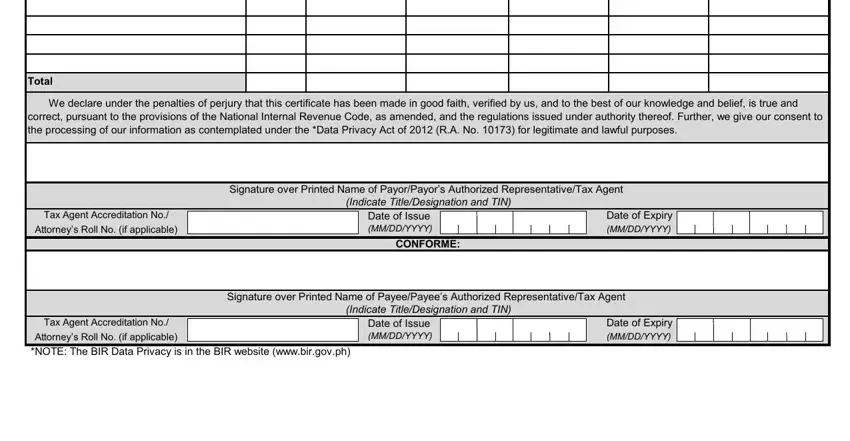

4. Sign and certify. Both the payor and the authorized representative must sign the form, declaring under penalties of perjury that all information is correct. Use the "Done" button in the editor to save your completed form.

Filing Deadlines

Payors must issue this certificate to payees by the end of the month following the close of the reporting period. For quarterly reporting, the form is due within 10 days after the end of each quarter. Late filing may result in penalties from the BIR. Payees should attach their certificates when filing income tax returns using BIR Form 1701Q (quarterly) or BIR Form 1701 (annual).

Penalties for Non-Compliance

Failing to issue or file this form on time can lead to penalties under the National Internal Revenue Code. Payors who do not withhold the correct tax amount or fail to remit it through the monthly remittance return (BIR Form 1601-E) face surcharges of 25% on the unpaid amount and interest charges of 12% per year. Payees who cannot present a valid certificate may lose their right to claim the tax credit, resulting in a higher tax bill when filing their annual return.

Difference Between Form 2307 and Form 2306

Both forms certify taxes withheld at source, but they cover different types of income. BIR Form 2306 is the Certificate of Final Tax Withheld at Source, used for income subject to final withholding tax such as interest income and dividends. Form 2307 covers income subject to creditable (expanded) withholding tax, where the amount withheld can be credited against the payee's total income tax liability on their annual return.